1. Facts

X AG, founded in 2010 and headquartered in Canton B, has fully paid-in share capital of CHF 20 million, divided into 20,000 fully paid-in registered shares with a par value of CHF 1,000 each. All shares of X AG are owned by Mr. A, who is also subject to unlimited tax liability in Canton B.

Starting in the 2014 fiscal year, X AG’s performance steadily deteriorated, resulting in a loss that grew steadily over the years. As of November 1, 2018, interim financial statements for X AG are therefore prepared. These show a total loss carryforward of CHF 12 million. Mr. A, in his capacity as a shareholder of X AG, makes a cash contribution to X AG in the amount of CHF 11 million at this time, with X AG recognizing this contribution in full in its open capital contribution reserves. A corresponding report is also submitted to the Federal Tax Administration (FTA) using Form 170. Due to the circumstances (restructuring), X AG refrains from calculating the issue tax on Mr. A’s cash contribution. As part of the restructuring, X AG also refrains from writing off the loss carryforward against the corresponding open capital contribution reserves. A corresponding write-off will not take place until prior to the transfer of the company to an independent third party at the beginning of 2022.

Questions

- What are the general requirements for the issuance tax to be due?

- Can the exception provision of Art. 6(1)(k) StG be invoked in this case?

- Is a waiver pursuant to Art. 12 StG possible in this case?

1. Facts

The Muster couple owns a small group of companies—the traditional family business—through a family holding company and also directly owns Muster AG, which operates a successful business that is completely independent of and separate from the family business. The eldest daughter purchases all shares in Muster AG from her parents through an acquisition holding company at a market value of CHF 15,000,000, whereby the acquisition holding company pays CHF 3,000,000, corresponding to its equity, and CHF 12,000,000 is left as a loan from the parents. The terms are as follows:

- Unsecured

- Interest-free

- Monthly amortization of CHF 100,000; the borrower may make higher amortization payments at any time, including full repayment of the outstanding loan amount.

- On delayed amortization payments, default interest of 4.0 percent is immediately due from the due date until payment without a reminder.

- As soon as an amortization payment is overdue, the creditors may terminate the entire remaining loan with immediate effect.

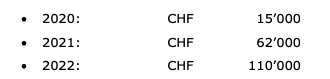

By March 2020, the loan will be repaid to CHF 4,500,000 in accordance with these terms. Due to COVID-19, no amortization payments will be made between April 2020 and the end of 2022, as Muster AG’s profits have plummeted and it cannot generate the dividends necessary for the amortization payments; the outstanding balance as of December 31, 2022, is therefore CHF 3,300,000. Default interest is charged on this amount in accordance with the contract, resulting in the following default interest payments by Muster AG to the creditors:

Starting in January 2023, amortization payments will resume. The difference between CHF 4,500,000 and CHF 3,300,000—that is, CHF 1,200,000—was and remains, like the loan itself, non-interest-bearing.

During an audit covering the period up to and including 2022, the FTA noted:

- There are no third-party relationships.

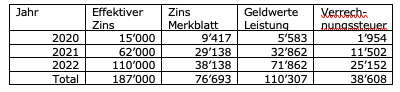

- The FTA therefore applies the interest rates set forth in the 2020–2022 interest rate schedules, i.e., it recognizes 2.5 percent up to CHF 1,000,000 and 0.75 percent for amounts exceeding CHF 1,000,000

- The FTA’s calculation results in the following monetary benefits for Muster AG:

Questions

- Does the loan agreement involve third-party relationships or not?

- Is the interest calculation correct, or what are the counterarguments?

1. Facts

The Muster Group is an internationally active conglomerate; the domestic Muster Holding AG is the parent company, and the domestic Muster AG serves as the group’s operational “control center.” The U.S. market is centered under US-Subholding AG. Additionally, the Muster Group has central business units in Germany and the UK, which are consolidated under D-Subholding AG and UK-Subholding AG.

The Muster Group is planning a new overall financing structure as follows:

-

Financing 1:- Muster Holding AG, as the issuer, issues an unsecured bond of CHF 250,000,000.

- The proceeds will be made available to the domestic subsidiary Muster AG in the form of a loan with a spread, and possibly also via cash pooling for a small amount.

-

Financing 2:- US-Subholding AG, as the issuer, issues an unsecured bond in the amount of USD 500,000,000.

- Muster Holding AG guarantees this bond.

- The funds are transferred by the US subholding exclusively to its US subsidiaries in the form of loans.

-

Financing 3:- A newly established Dutch company, Muster Finanz AG, a subsidiary of Muster AG, plans to issue a bond of up to EUR 1,200,000,000 as the issuer.

- Muster Holding AG grants a paid guarantee in favor of Muster Finanz AG.

- Muster Finanz AG will pass on the EUR 1,200,000,000 raised to Muster AG in the form of a loan.

- SAG will pass on the funds received from Muster Finanz AG as a loan to D-Subholding AG and UK-Subholding AG and, if necessary, to other foreign group companies.

- Approximately EUR 200,000,000 will be used by Muster Finanz AG.

The total equity of the foreign group companies of the Muster Group amounts to approximately CHF 250,000,000.

Questions

- What should be noted regarding Muster Finanz AG?

- Are there any withholding tax implications regarding Financing 1?

- Are there any withholding tax implications regarding Financing 2?

- Are there any withholding tax implications regarding Financing 3?

- What should be considered regarding the interest structure?

- What should be considered regarding the settlement of the guarantee?

- Does it matter whether Muster Finanz AG is a subsidiary of Muster Holding AG instead of Muster AG?

- Are there any stamp duty implications?

1. Facts

The Tue-Gutes Foundation was established in 2018 in the Principality of Liechtenstein (hereinafter referred to as “FL”). At the time of its establishment, the founder, Ms. Grosszügig, was subject to unlimited tax liability in Switzerland, was 81 years old, and designated herself and her children as beneficiaries. Ms. Grosszügig and her adult children have been living in Germany since 2019.

In 2022, the Tue-Gutes Foundation submitted the following refund applications to the FTA using Form 78 for the withholding tax deducted on dividends from its stock portfolio:

-

Due in 2019 CHF 200,000 Withholding tax CHF 40,000

-

Due 2020 CHF 300,000 Withholding tax CHF 60,000

-

Due in 2021 CHF 200,000 Withholding tax CHF 40,000

In 2023, the FTA rejected these refund claims on the following grounds:

- In the case of foreign foundations, the specific circumstances are examined to determine to whom the foundation’s assets and income are attributable for tax purposes.

- For the purposes of attribution, it is of decisive importance who, based on the specific circumstances of the individual case, actually has control over the foundation’s assets.

- According to the submitted statutes, the founder has the authority to issue and amend regulations.

- The founder therefore has a right to issue instructions in the sense of having a certain influence over the foundation, such that the foundation’s assets and income can be attributed to the founder for tax purposes.

- Due to the attribution to the founder residing in Germany, a refund based on the Double Taxation Agreement between Switzerland and FL (hereinafter referred to as “DTA-FL”) is not possible.

Questions

- What is the significance of the FTA’s 2023 rejection letter?

- What are the conditions for a refund?

- Does it matter that the founder was placed under guardianship at the end of 2020 due to age-related dementia?

1. Facts

Vertriebs AG is part of an international group. In the past, it has retained earnings and reports over CHF 30,000 in reserves subject to withholding tax, which are offset by an identical amount of liquidity. Vertriebs AG has invested these liquid funds in the group’s own cash pool with the cash pool leader based in EU Country 1. The interest rate has been 0.00 percent from 2017 to 2022. The average cash pool costs passed on to Vertriebs AG amount to CHF 100,000 per year as cash pool leader remuneration.

This matter is addressed during an audit by the FTA for the years 2018–2022.

Questions

- Is this considered a monetary benefit, and—if so—how is it calculated?

- What changes if the cash pool leader is a domestic company and the parent company of Vertriebs AG?