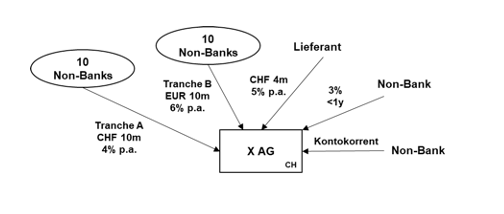

1. Facts

The domestic company X. AG raises debt financing (private placement) in March 2024. The private placement consists of Tranche A (CHF 10 million; 4% p.a.) and Tranche B (EUR 10 million; 6% p.a.). Both Tranche A and Tranche B have 10 non-bank creditors each.

X. AG has no other long-term liabilities denominated in a fixed amount.

However, X. AG still has the following liabilities:

- A liability to a supplier arising from an outstanding invoice of CHF 4 million, which has accrued interest at 5% p.a. since the due date.

- A short-term liability to a non-bank bearing interest at 3% p.a.

- An overdraft liability to a non-bank.

Question

Is the private placement a bond within the meaning of Art. 4(1)(a) VStG?

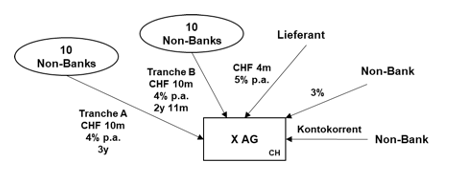

How would the case be assessed if Tranche A and Tranche B were both denominated in CHF and bore interest at 4% p.a., but the term of Tranche B were one month shorter than that of Tranche A?

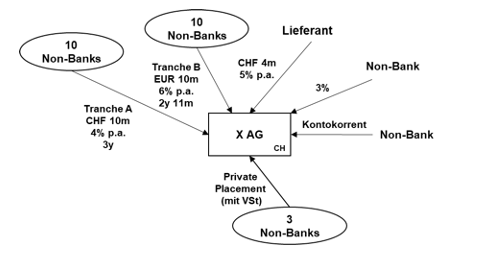

As in the initial facts.

X. AG, however, has issued another private placement bearing 4% interest to three non-bank creditors and declared this to the FTA as a bond (and paid withholding tax on the interest).

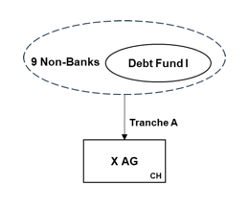

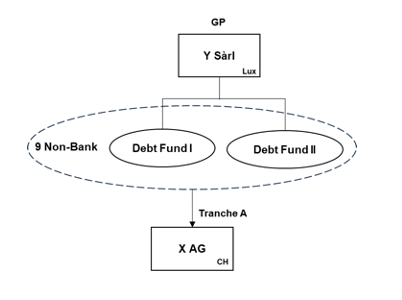

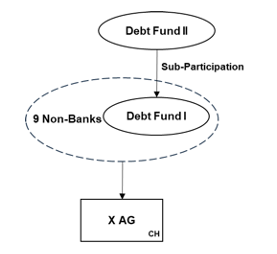

One of the 10 creditors of X. AG under Tranche A is Debt Fund I, a fund without legal personality (Special limited partnership; SCSp) established under Luxembourg law with numerous (non-bank) investors.

Debt Fund I was established in 2021 and, in addition to the claim against X. AG, holds numerous other investments.

The general partner (GP) is Y. Sàrl. The fund management company (AIFM) is Z. Sàrl.

Does this change the assessment in any way?

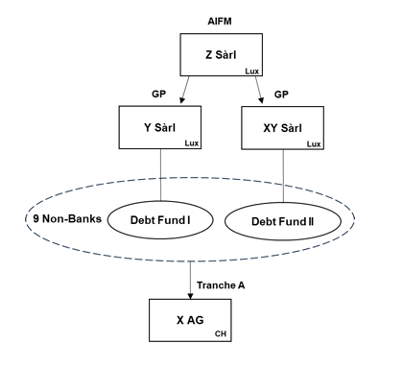

Now, not only Debt Fund I but also (the equally pre-existing) Debt Fund II is to subscribe to Tranche A (alongside 9 other non-bank creditors).

The GP of Debt Fund II is also Y. Sàrl.

As in Variant 4. However, the GP of Debt Fund II is now XY Sàrl. Like Debt Fund I, Debt Fund II has Z. Sàrl as its AIFM.

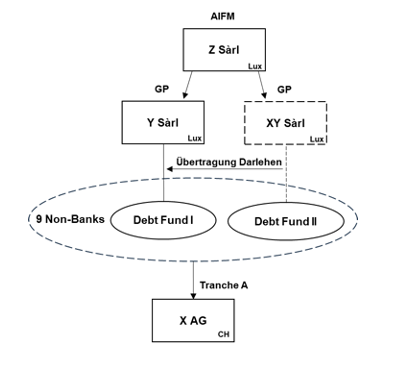

As in Variant 5. Debt Fund II notices the error (before the first interest payment) and sells its claim against X.AG to Debt Fund I.

As in the initial scenario.

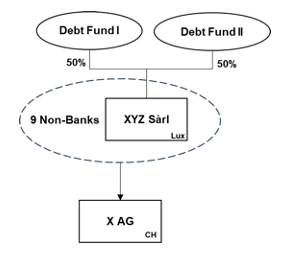

Debt Fund I and Debt Fund II establish a Luxembourg corporation (XYZ Sàrl), which subscribes to Tranche A.

As in the initial scenario.

Debt Fund I now grants Debt Fund II a sub-participation in Tranche A.

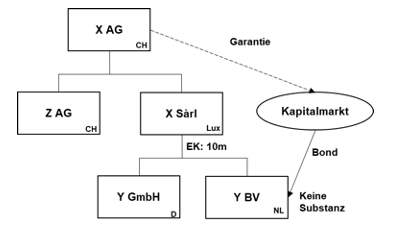

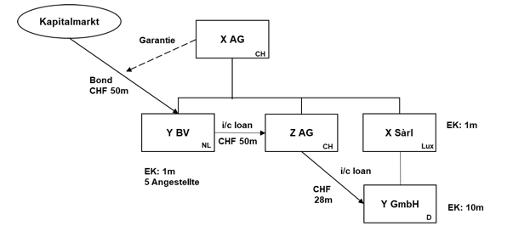

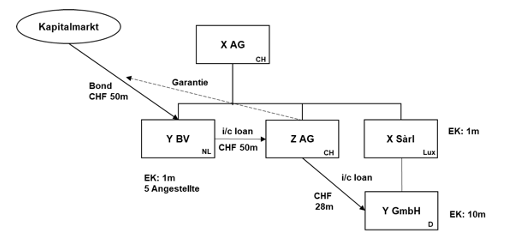

1. Facts

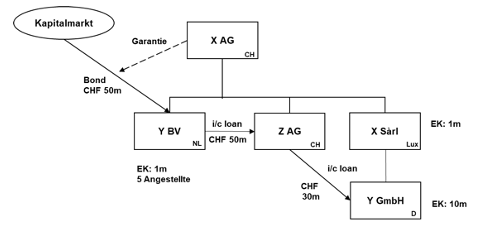

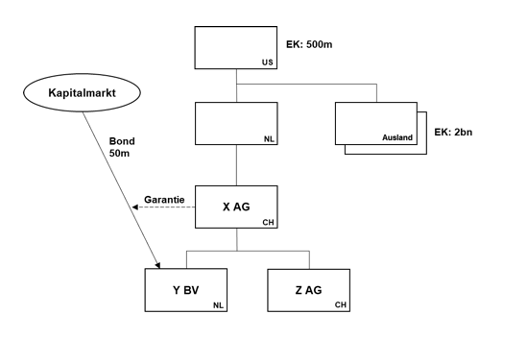

In March 2024, the domestic company X. AG issues a bond in the amount of CHF 50 million with a 5-year term and a coupon of 3.5% p.a. (10,000 notes at CHF 5,000 each) through its Netherlands-based financial company Y. BV (share capital: CHF 1 million; 5 employees). The bond is registered with SIX as a book-entry security.

The bond is guaranteed by X. AG.

The funds raised through the bond are passed on via a loan to Z. AG, a domestic subsidiary of X. AG.

X. AG also has a Luxembourg-based subsidiary (X. Sàrl; equity: CHF 10 million; a holding company) which, in turn, holds a Germany-based operating subsidiary (Y. GmbH; equity: CHF 10 million).

In December 2024 (two weeks before the end of the fiscal year on December 31), X. AG grants Y. GmbH a loan of CHF 30 million.

Questions

- How should the interest payments under the bond be treated?

- Are transfers of shares subject to the turnover tax?

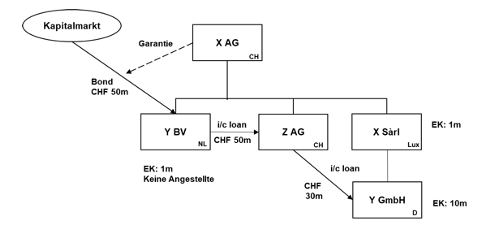

As in the initial scenario.

On January 15, 2025, Y. GmbH repays the loan to Z. AG. It is not until December 15, 2025, that a loan is granted to Y. GmbH again.

As in the initial facts.

However, Y. BV now has no employees working in the Netherlands.

As in Variant 2.

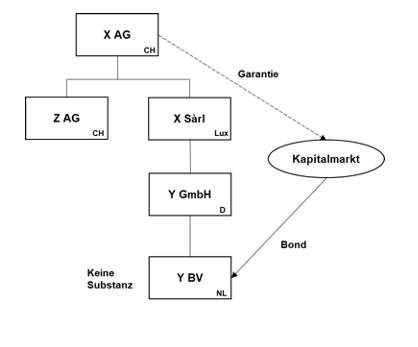

However, Y. BV is now a subsidiary of the German company Y. GmbH.

As in Option 2.

However, Y. BV is now a subsidiary of the Luxembourg intermediate holding company X. Sàrl.

As in the initial scenario.

As of December 31, 2024, the foreign group companies have liabilities totaling only CHF 28 million

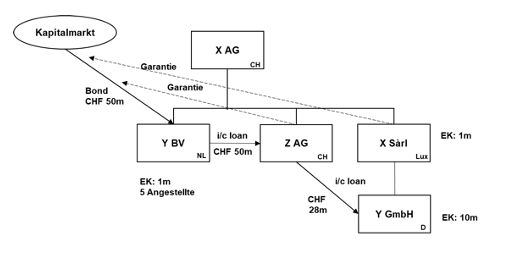

As in Variant 5.

Now, however, it is not X AG but its subsidiary Z AG that provides the guarantee. Z AG’s guarantee is contractually limited to the funds of Z AG that are distributable under commercial law at the time the guarantee is called upon.

As in Option 6.

In addition to Z. AG, X. Sàrl now also provides a guarantee. The guarantee provided by X. Sàrl is not limited to the distributable funds of X. Sàrl (nor those of its parent company, X. AG) (and there is also no statutory limitation under Luxembourg company law).

As in Option 5.

X AG will be acquired by a U.S. group in 2025. The group will acquire X AG through a Dutch holding company. The U.S. parent holding company has equity of CHF 500 million and has additional foreign group companies with cumulative equity of CHF 2 billion.

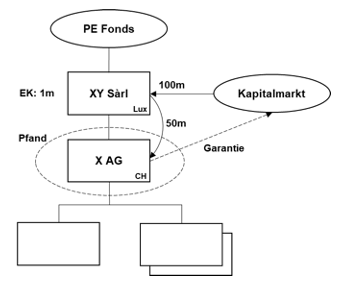

X AG is acquired in 2025 by a private equity fund through a Luxembourg acquisition company (XY Sàrl) for CHF 200 million.

To this end, XY. Sàrl raises acquisition financing of CHF 100 million. (This is used, among other things, to repurchase the bond issued by Y. BV.)

XY. Sàrl has equity of CHF 1 million.

The acquisition financing is guaranteed and secured (post-closing) by X. AG. The guarantees and collateral are contractually limited to the distributable funds of X. AG. In addition, XY. Sàrl grants a pledge over the shares of X. AG as well as a security assignment of XY. Sàrl’s claims against X. AG (and its subsidiaries).

XY. Sàrl has no assets whatsoever in Luxembourg.

As in the initial scenario.

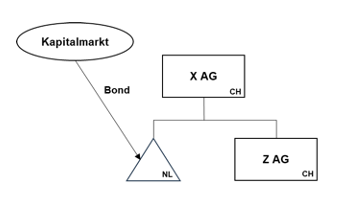

X AG now issues the bond not through a subsidiary, but through its Dutch branch.

1. Facts

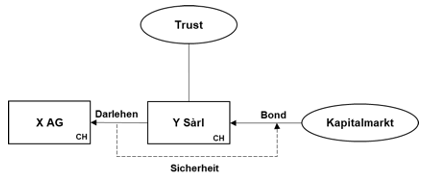

The domestic X. AG has no foreign subsidiaries. It raises funds on the capital market through a so-called orphan bond.

To this end, Y. Sàrl, based in Luxembourg, issues 10,000 notes totaling CHF 50 million with a coupon of 3.5%. The funds are transferred to X. AG in the form of a loan.

The notes are secured by a pledge of Y. Sàrl’s loan claim against X. AG.

Y. Sàrl is owned by a charitable foundation in Liechtenstein. Y. Sàrl is managed by Z. Bank.

Question

Are interest payments on the notes or the loan subject to withholding tax?

1. Facts

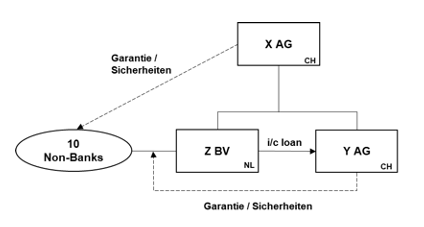

The domestic X. AG is the parent company of the also domestic Y. AG as well as the financial company Z. BV, which is based in the Netherlands.

Z. BV is the debtor under a loan agreement and passes the funds on to Y. AG. The loan agreement is guaranteed and secured by both X. AG and Y. AG.

The net use of funds in Switzerland exceeds the equity of the foreign group companies.

The loan agreement is syndicated to a maximum of 10 non-bank creditors.

Questions

- What must be ensured to ensure that interest payments are not subject to withholding tax?

- What applies with regard to the concept of “cash obligation” relevant for the turnover tax?