- Entreprises

- International

Post-closing M&A aspects

Note: This language version is an automatically generated translation. The text may therefore contain linguistic and terminological errors.

view in original language (German)Note: This language version is an automatically generated translation. The text may therefore contain linguistic and terminological errors.

view in original language (German)What tax risks arise after the closing - and how can they be identified and managed at an early stage? These case studies shed light on key post-closing issues such as indirect partial liquidation, financing structures, guarantees and intragroup restructurings. Typical stumbling blocks and their tax consequences are systematically highlighted using practical scenarios. The solutions offer you concrete guidance for the legally compliant structuring and implementation of post-deal transactions.

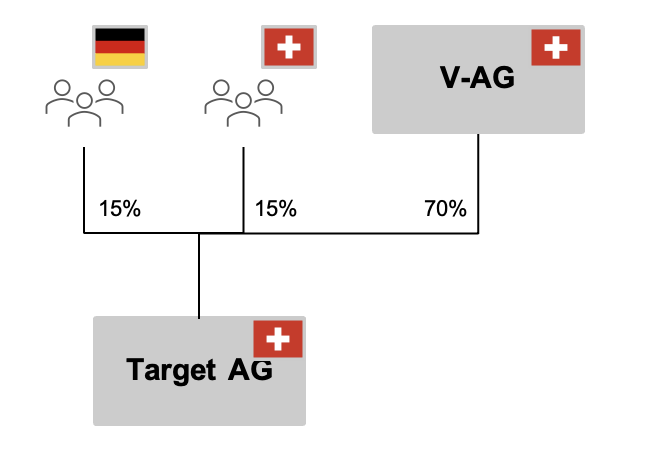

Target AG, headquartered in Zurich, is owned by three “shareholder groups”: Shareholder I, V-AG, headquartered in Switzerland (70% stake); Shareholder Group II, consisting of five individuals residing in Germany (who collectively hold a 15% stake); and by Shareholder Group III, consisting of five individuals residing in Zurich, Switzerland (who collectively hold a 15% stake).

Target AG will be sold on March 31, 2026, to K-AG, based in Zurich, Switzerland.

Is the sale of Target AG a case for indirect partial liquidation (ITL)?

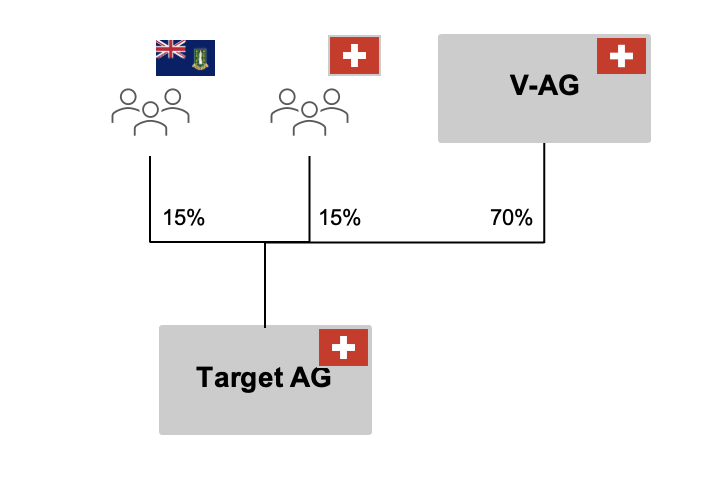

Shareholder Group II now consists of natural persons residing in an offshore jurisdiction (e.g., the British Virgin Islands). The other two shareholder groups remain unchanged. As of March 31, 2026, all shares in Target AG will again be sold to K-AG, which is based in Zurich, Switzerland.

Does your assessment change, or does the sale of Target AG constitute a case for the ITL?

Target AG, headquartered in Zurich, is owned by three individuals residing in Zurich / Switzerland. On March 31, 2026 (signing of the binding agreement with simultaneous closing of the transaction), the shareholders sell an 85% stake to K-AG, headquartered in Zurich, Switzerland, for CHF 8.5 million. The general meeting of Target AG took place on March 15, 2026.

The simplified balance sheet of Target AG as of December 31, 2025, can be presented as follows:

The shareholder current account is to be repaid to Target AG by K-AG on behalf of the shareholders upon closing of the sale. Non-operating funds amount to CHF 1.0 million (assumption

: accepted liquidity reserve of CHF 300,000)

Is the sale of Target AG a case for the ITL? If so, what is the extent of potential taxation?

One year later, i.e., as of March 31, 2027, the three minority shareholders (i.e., natural persons residing in Zurich) sell an additional 10% of the shares to K-AG, headquartered in Zurich, Switzerland, for CHF 1.0 million.

Target AG did not pay any dividends for the 2025 fiscal year. The financial statements of K-AG and all group companies of the K Group are not available until early April of the following year (due to the preparation of consolidated financial statements). The Annual General Meeting of Target AG for the 2026 fiscal year will therefore not take place until late April 2027.

The simplified balance sheet of Target AG as of December 31, 2026, can be presented as follows:

Another year later, i.e., as of March 31, 2028, the remaining 5% of shares are sold to K-AG, headquartered in Zurich, Switzerland. The Annual General Meeting for the 2027 fiscal year has not yet taken place.

The simplified balance sheet of Target AG as of December 31, 2027, can be presented as follows:

Initial situation as in the standard case, i.e., sale of 85% by three individuals residing in Zurich / in Switzerland to K-AG as of March 31, 2026. The three individuals sell the remaining 15% to K-AG in April 2031. K-AG.

Is the partial sale of the 15% in April 2031 subject to the ITL regulations?

Already with the purchase agreement effective March 31, 2026, the parties—i.e., the three individuals residing in Zurich / in Switzerland and K-AG—enter into a put-call option agreement regarding the remaining 15%.

K-AG exercises the call option either:

Is the sale of the 15% subject to the ITL regulations under the put-call option?

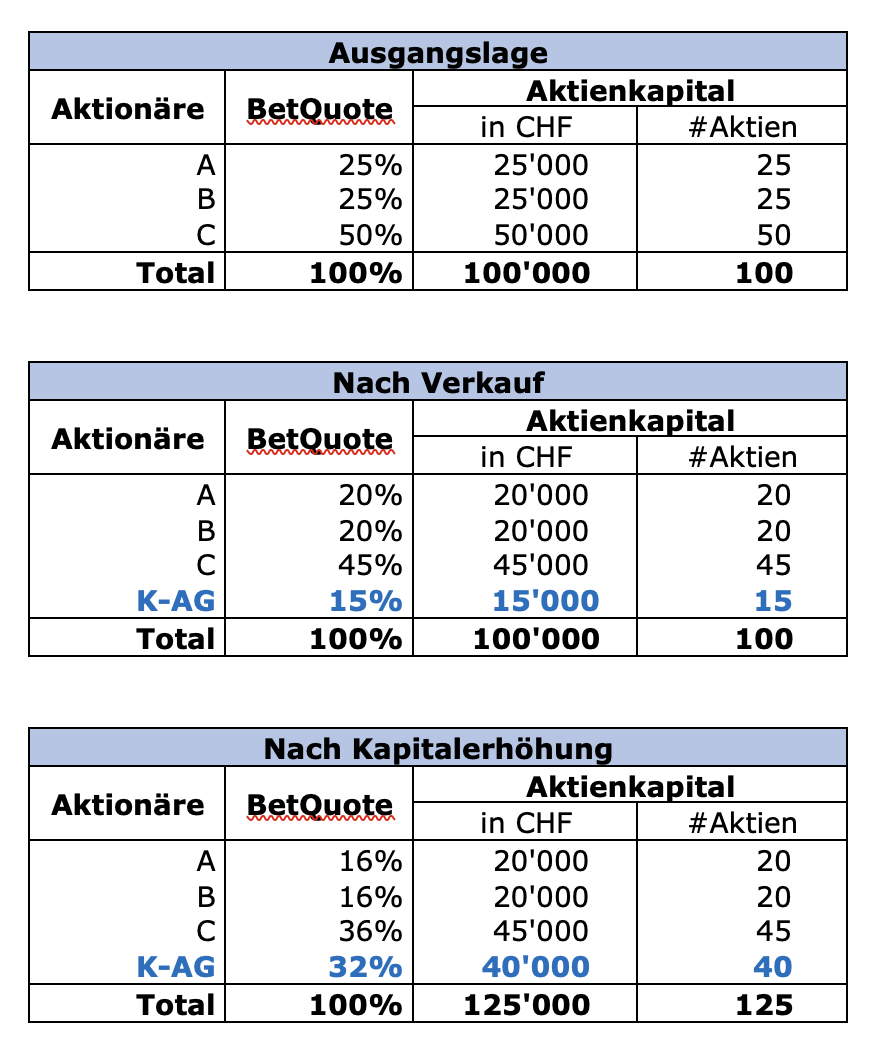

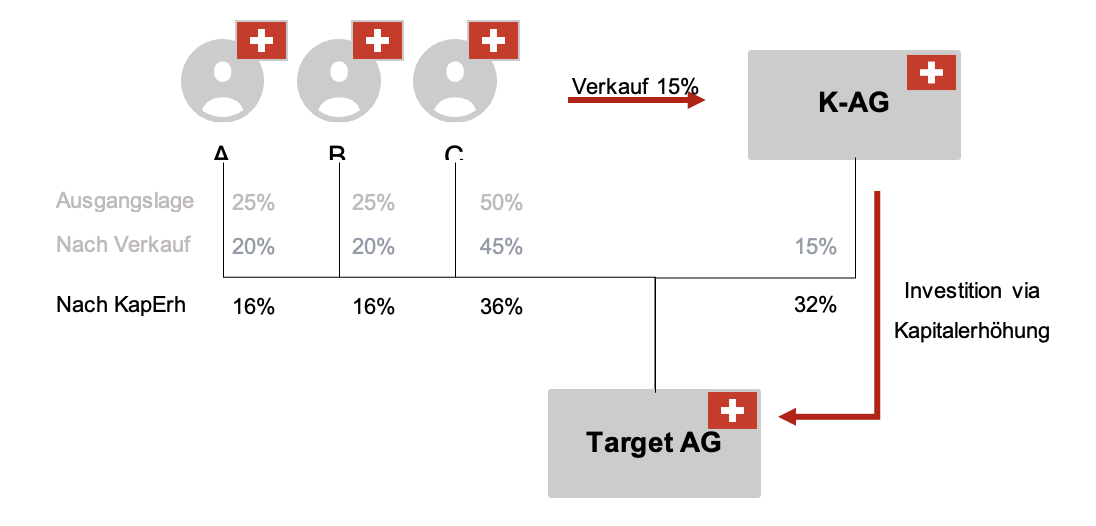

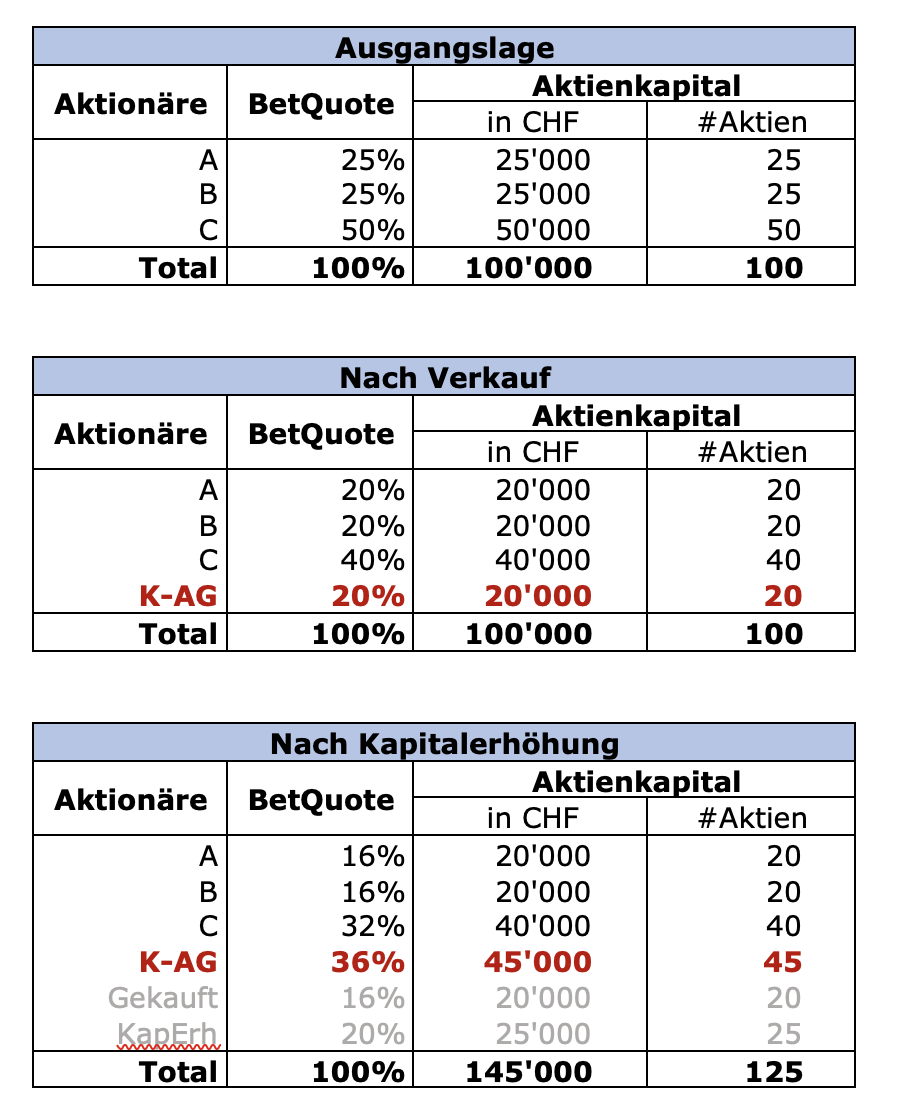

Target AG, headquartered in Zurich, is owned by three individuals residing in Zurich / Switzerland. Shareholders A and B each hold 25%, and shareholder C holds 50% of the shares.

The share capital of Target AG currently amounts to CHF 100,000, divided into 100 shares with a par value of CHF 1,000 each.

On March 31, 2026, the three shareholders will sell a 15% stake to K-AG, headquartered in Zurich, Switzerland (“Primary Transaction”). Additionally, the parties agree that Target AG will carry out a capital increase in which only K-AG will subscribe for new shares (“Secondary Transaction”); the three individuals will accordingly waive their subscription rights.

The ownership structure of Target AG following the completed sale and capital increase can be illustrated as follows:

The transaction and the respective ownership structure of Target AG can be illustrated as follows:

On March 31, 2026, the three shareholders sell a 20% stake to K-AG, headquartered in Zurich, Switzerland (“Primary Transaction”). Additionally, on the date of execution of the share purchase agreement, a capital increase takes place in which only K-AG subscribes for new shares (“Secondary Transaction”); the three natural persons accordingly waive their subscription rights.

The ownership structure of Target AG following the completion of the sale and capital increase can be summarized as follows:

How do you assess the situation with regard to the existence of the elements of an ITL?

On March 31, 2026, the three shareholders residing in Zurich / Switzerland sell a 20% stake in K-AG, headquartered in Zurich / Switzerland. The shares in question are employee shares that were acquired at a formula value. The holding period for the shares is less than five years.

How do you assess the situation with regard to the existence of the facts

Target AG, headquartered in Zurich, was owned by individuals residing in Zurich / Switzerland. On March 31, 2026, all shares in Target AG were sold to K-AG, headquartered in Zurich / Switzerland. The purchase agreement includes an indemnification clause in favor of the sellers in the event of a breach of the ITL.

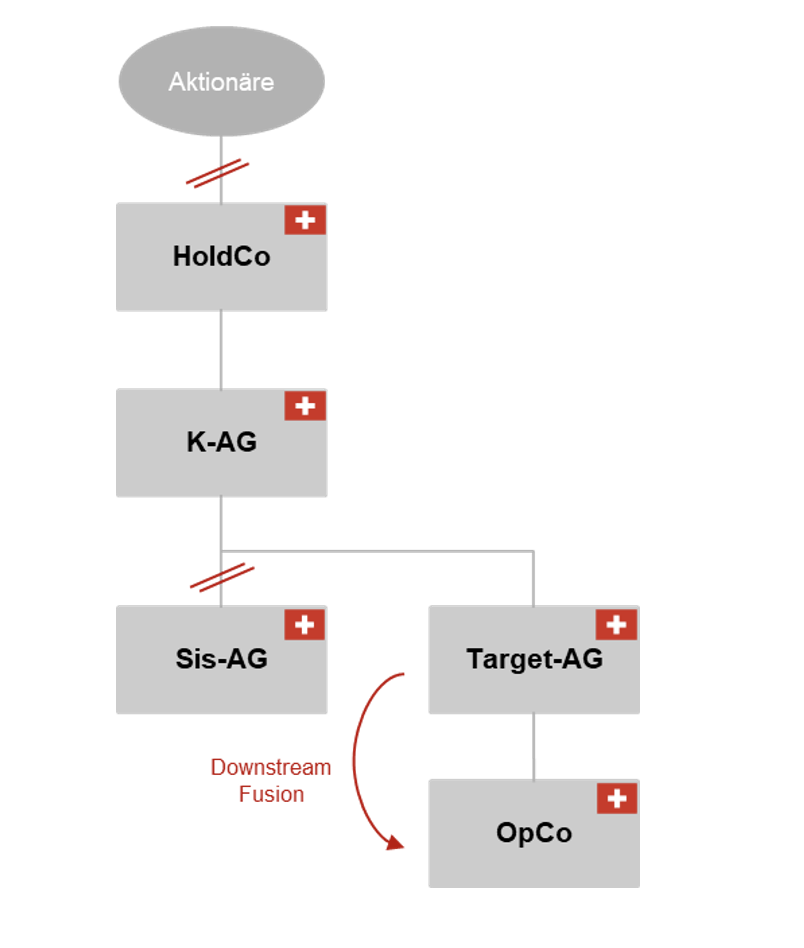

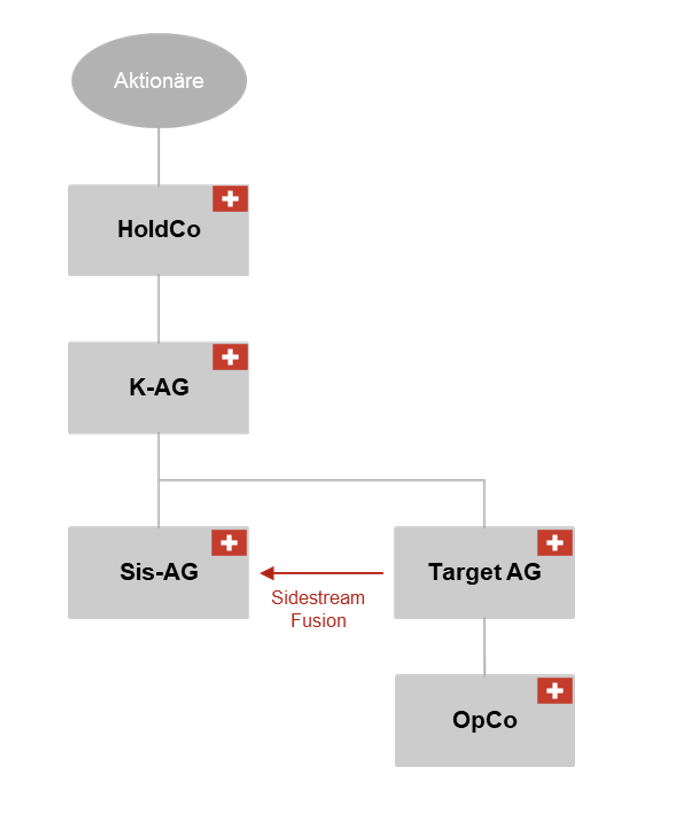

K-AG is a pure holding company. In addition to its stake in Target AG, K-AG holds numerous other stakes in operating companies in Switzerland and abroad, including in particular Sis-AG, based in the Canton of Zurich.

To acquire Target AG, K-AG obtained external financing from a third party (i.e., a bank).

As collateral for the bank financing, the bank requires an upstream guarantee from Target AG. Under commercial law, this upstream guarantee[ is limited to the freely available equity of Target AG.]

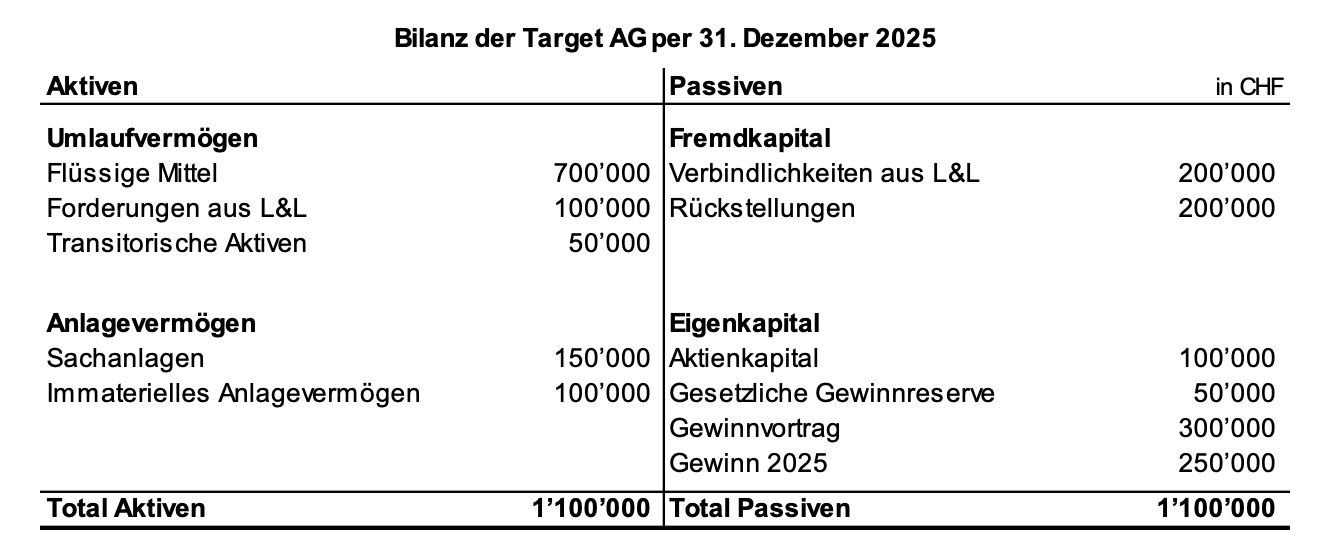

To pay the first principal installment of the bank financing as well as the first interest payment in Q3/2026, Target AG decides to grant a loan to K-AG. At the time the agreement was concluded on March 31, 2026, the audited 2025 financial statements were already available and had already been approved by the general meeting of Target AG.

The balance sheet of Target AG as of December 31, 2025, can be presented as follows:

The loan agreement between Target AG and K-AG stipulates that the loan amounts to CHF 500,000, bears interest in accordance with the ESTV’s Safe Haven Rates (i.e., in accordance with the 2026 Circular on Tax-Recognized Interest Rates for Advances or Loans in Swiss Francs), and may be amortized either upon maturity (5 years) or through dividends from future profits.

How do you assess the granting of the upstream loan with regard to the ITL?

Target AG, headquartered in Zurich, was owned by individuals residing in Zurich / Switzerland. On March 31, 2026, all shares in Target AG were sold to K-AG, headquartered in Switzerland. The purchase agreement contains an indemnification clause in favor of the sellers in the event of a breach of the ITL.

The purchase agreement stipulates that a portion of the purchase price is to remain as a loan liability of K-AG to the sellers. This loan is to be amortized over the following five years and bear interest in accordance with the FTA’s safe-haven rates (i.e., in accordance with the 2026 Circular on Tax-Deductible Interest Rates for Advances or Loans in Swiss Francs).

How do you assess the granting of the seller loan with regard to the ITL?

Target AG, headquartered in Zurich, was owned by individuals residing in Zurich / Switzerland. On March 31, 2026, all shares in Target AG were sold to K-AG, headquartered in Switzerland. The purchase agreement includes an indemnification clause in favor of the sellers in the event of a breach of the ITL.

K-AG is a pure holding company. In addition to its stake in Target AG, K-AG holds numerous other stakes in operating companies in Switzerland and abroad, including in particular Sis-AG, based in the Canton of Zurich.

To finance the acquisition of Target AG, K-AG obtained external financing from a third party (i.e., a bank).

In addition, to increase cost efficiency and avoid duplication of effort, management functions are to be centralized at the K-AG level. Against this backdrop, Group Treasury, Group Legal, and Accounting functions, as well as Group C-level functions, will be established. To this end, two accountants and Target AG’s in-house lawyer will be newly hired by K-AG. Furthermore, Target AG’s CFO is to be newly hired by K-AG and will serve as Group CFO.

How do you assess the centralization plans with regard to ITL?

Target AG, headquartered in Zurich, was owned by individuals residing in Zurich / Switzerland. On March 31, 2026, all shares in Target AG were sold to K-AG, headquartered in Switzerland. The purchase agreement includes an indemnification clause in favor of the sellers in the event of a breach of the ITL.

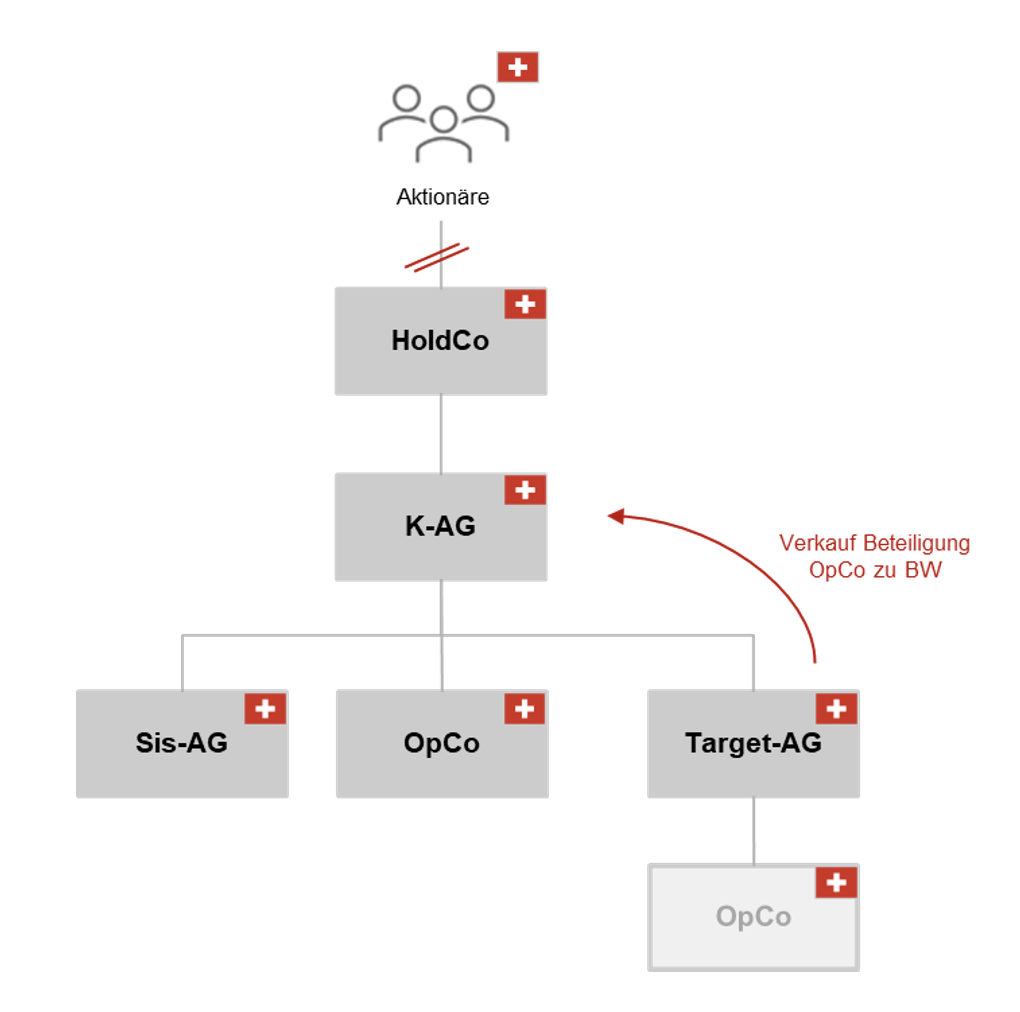

K-AG is a pure holding company. In addition to its stake in Target AG, K-AG holds numerous other stakes in operating companies in Switzerland and abroad, including in particular Sis-AG, based in the Canton of Zurich.

As part of the post-closing integration, the OpCo is to be transferred from Target AG to K-AG at a book value of CHF 100,000 on a tax-neutral basis (“transfer between domestic group companies” under civil law in the form of a sale).

How do you assess the transfer of the equity interest in OpCo at book value to the acquiring company K-AG from an ITL perspective?

Target AG, headquartered in Zurich, was owned by individuals residing in Zurich / Switzerland. On March 31, 2026, all shares in Target AG were sold to K-AG, headquartered in Zurich / Switzerland. The purchase agreement includes an indemnification clause in favor of the sellers in the event of a breach of the ITL.

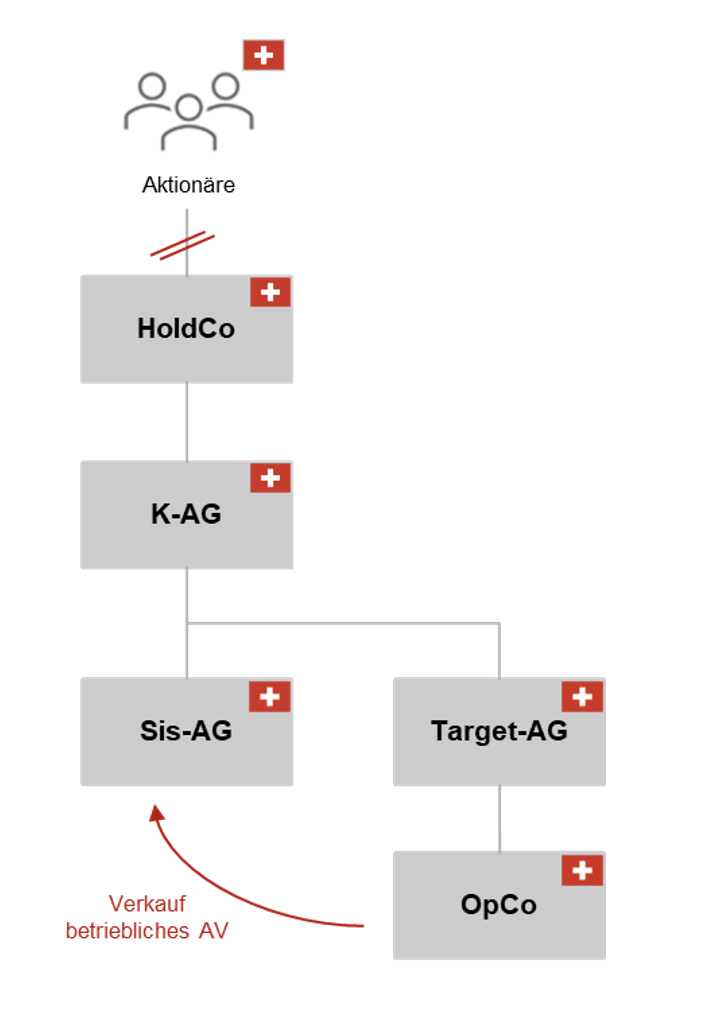

K-AG is a pure holding company. In addition to its stake in Target AG, K-AG holds numerous other stakes in operating companies in Switzerland and abroad, including in particular Sis-AG, based in the Canton of Zurich.

K-AG centralizes all acquired intellectual property with a sister company (“Sis-AG”) based in Switzerland. K-AG decides to do the same for Target AG’s intellectual property rights. The intellectual property rights of the Target Group and the OpCo are to be transferred from the OpCo to Sis-AG at a book value of CHF 100,000 on a tax-neutral basis ("transfer between domestic group companies" to a sister company of Target AG).

Target AG, headquartered in Zurich, was owned by individuals residing in Zurich / Switzerland. On March 31, 2026, all shares in Target AG were sold to K-AG, headquartered in Zurich / Switzerland. The purchase agreement includes an indemnification clause in favor of the sellers in the event of a breach of the ITL.

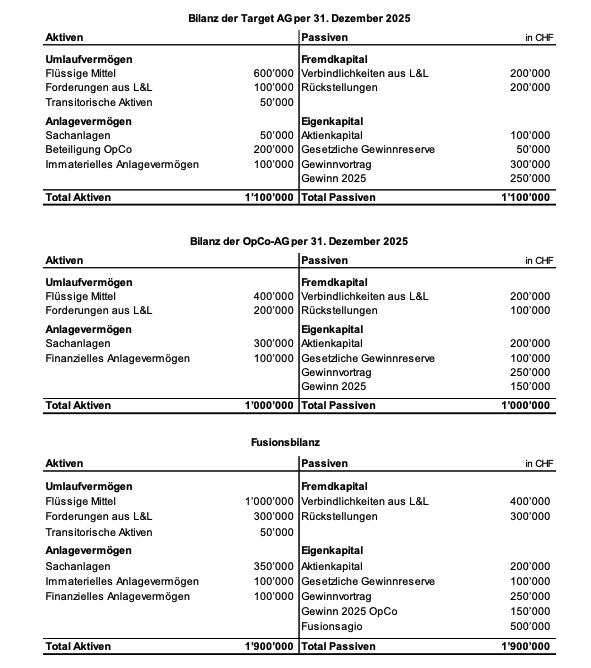

As part of a group-wide structural simplification, K-AG decides to merge Target AG with its subsidiary, OpCo, based in Zurich. The merger is to take place based on the financial statements as of December 31, 2025, and retroactively as of January 1, 2026. OpCo is to be the acquiring company (downstream merger). The merger is entered in the Commercial Register of the Canton of Zurich at the end of May 2026.

The balance sheets of the two companies as of December 31, 2025, as well as the balance sheet of the acquiring OpCo following the merger, can be presented as follows:

How do you assess the proposed parent company absorption / downstream merger, particularly with regard to the ITL?

Target AG, headquartered in Zurich, was owned by individuals residing in Zurich / Switzerland. On March 31, 2026, all shares in Target AG were sold to K-AG, headquartered in Zurich / Switzerland. The purchase agreement includes an indemnification clause in favor of the sellers in the event of a breach of the ITL.

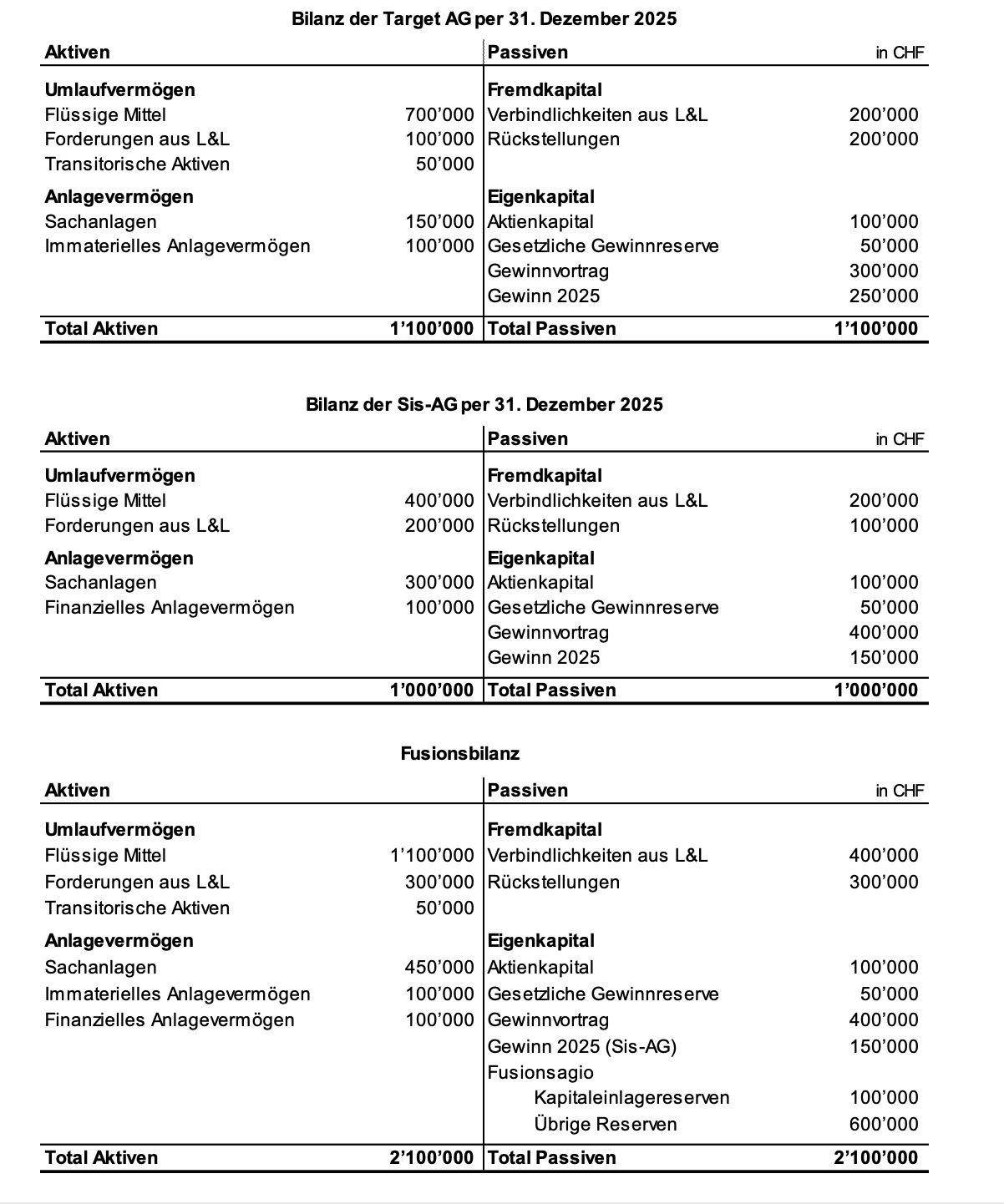

As part of a group-wide structural simplification, K-AG resolves to merge Target AG with Sis-AG, based in Zurich, based on the financial statements as of December 31, 2025 (the Annual General Meeting took place in mid-March; no dividend was declared for FY 2025) and retroactively as of January 1, 2026. Sis-AG is to be the acquiring company. The merger is entered in the Commercial Register of the Canton of Zurich at the end of May 2026.

The balance sheets of the two companies as of December 31, 2025, as well as the balance sheet of the acquiring Sis-AG following the merger, can be presented as follows:

As of the closing date, Target AG holds treasury shares with a book value of CHF 500,000. The treasury shares were originally acquired for the purpose of employee participation at Target AG. Following the acquisition by K-AG, the treasury shares at Target AG are no longer required—any employee participation will take place at the K-AG level.

Target AG reports both reserves from capital contributions (KER within the meaning of Art. 20 para. 3 DBG and Art. 5 para. 1^bis^ VStG) and retained earnings.

Following the acquisition of Target AG by K-AG, the structure is to be adjusted accordingly. To this end, three options are being discussed:

Prior to the transaction, both parties A and B each hold a 50% stake in Target AG. Party A is now to acquire Party B’s stake as part of a share deal and, following closing, will accordingly hold 100% of Target AG.

The following payments are made as part of the transaction:

How are the corresponding payments classified for the sellers and for the buyer of K-AG?