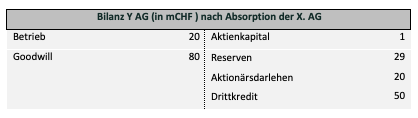

1. Facts

On February 15, 2025, a private equity fund acquires the domestic company X. AG through another domestic acquisition vehicle, Y. AG, for CHF 100 million.

Y. AG is financed with equity capital of CHF 30 million. The remaining CHF 70 million is raised through a shareholder loan granted by the fund (CHF 20 million) and a third-party loan (guaranteed and secured by the fund), both of which bear interest at 8% per annum.

On June 15, 2025 (alternative: June 15, 2027), Y. AG merges with X. AG.

Question

- What are the tax consequences of the absorption?

2. Scenario 1: Reverse Merger

- Would the assessment change if X. AG were to absorb Y. AG (reverse merger)?

3. Scenario 2: Equity-to-debt swap

On May 15, 2025, X AG resolves to pay a dividend of CHF 18.5 million, which it settles through a debt assumption.

4. Option 3: Profit Push-Up

On May 15, 2025, X Corp. transfers a patent to Y Corp. This generates licensing revenue from third parties and Y Corp. of approximately CHF 5 million, which is used to service Y Corp.’s interest payments.

5. Option 4: Cascading Acquisition

Among X. AG’s assets is an (operating) subsidiary (X2. AG; fair value: CHF 70 million), which in turn holds an (operating) subsidiary, X3. AG (fair value: CHF 30 million).

Y. AG first acquires X3. AG for CHF 30 million, for which it takes out a loan of CHF 20 million and receives equity capital of CHF 10 million from the fund. X2. AG distributes the proceeds to X. AG and its owner.

X3 AG then acquires X2 AG for CHF 40 million, for which it receives a loan of CHF 25 million and equity of CHF 15 million. Interest payments are made from the operating income of X3 AG. X AG distributes the proceeds to its owner.

X2 AG finally acquires X AG for CHF 30 million, for which it receives a shareholder loan of CHF 20 million and equity of CHF 10 million. Interest payments are made from the operating income of X2 AG.

6. Option 5: Acquisition by an operating company

X. AG is now acquired not by the acquisition vehicle of a private equity fund, but on February 15, 2025, for CHF 100 million by an operating company (Y. AG). Prior to the acquisition of X. AG, Y. AG generated a profit of CHF 5 million per year.

Y. AG takes out bank financing of CHF 50 million for the acquisition of X. AG, which bears interest at 5% per annum.

On June 15, 2026, Y. AG merges with X. AG.

In 2028, Y. AG’s operations fall into crisis and the company goes into the red (while X. AG’s operations remain profitable).

7. Option 6: Acquisition of a real estate company

X. AG is a real estate company that is acquired by Y. AG on February 15, 2025, for CHF 100 million. The seller is a private individual.

On June 15, 2025, Y. AG absorbs X. AG.

1. Facts

X, a resident of Switzerland, is the sole shareholder of X AG. The company operates a business (book value: CHF 500,000) and owns a property (book value: CHF 1 million; acquisition cost: CHF 3 million; market value: CHF 10 million; rental income: CHF 300,000; mortgage: CHF 6 million).

As part of succession planning, on February 15, 2025, X AG transfers the business at a book value of CHF 500,000 to Y AG, a company newly established by X.

Question

- What are the tax consequences of transferring the business to Y. AG?

2. Option 1: Prompt sale of X. AG

In 2029, X. faces a financial crisis and sells X. AG for CHF 5 million (property value: CHF 12 million; mortgage: CHF 7 million).

3. Option 2: Pledging of shares

To resolve the financial difficulties, X. takes out a loan from a third party and secures it with the shares of X. AG through a security assignment.

4. Option 3: X’s untimely death

In 2028, X. dies unexpectedly. The estate administrator sells the shares of X. AG to a third party in 2029 and distributes the proceeds among the heirs.

5. Scenario 4: Immediate gift

X. gifts the shares of X. AG to his daughter Y. in 2026 (gift subject to equalization during his lifetime).

6. Scenario 5: Relocation to Another Canton

On November 15, 2025, X moves to the canton of Graubünden. On June 15, 2027, he sells his shares in X AG.

7. Option 6: Relocation abroad

X. moves to Berlin on November 15, 2025 (alternative: Dubai). On June 15, 2027, he sells his shares in X. AG.

8. Scenario 7: Cessation of operations of Y. AG

The buyer of Y. AG ceases operations of Y. AG as early as 2026 and liquidates the company.

1. Facts

Metall Holding AG is a company in Switzerland wholly owned by shareholder Petra Stebler. Metall Holding AG owns three wholly-owned subsidiaries: Gold AG, Silber AG, and Eisen AG. All three are operating companies.

Eisen AG owns 100% of Chrom AG, which is also an operating company. The book value, income tax value, and cost basis of Chrom AG amount to CHF 100,000.

Eisen AG intends to transfer all shares of Chrom AG to Metall Holding AG via a dividend distribution (stock dividend). The dividend is to be recorded in the amount of the book value, charged to the reserves of Eisen AG.

Question

- Is this spin-off possible on a tax-neutral basis, and does it violate the lock-up period resulting from the transfer described in the factual background?

3. Option 2: Prompt spin-off of Gold AG, Silver AG, and Iron AG

Unlike in Option 1, Chrom AG is not spun off; instead, the three subsidiaries Gold AG, Silber AG, and Eisen AG are spun off from Metall Holding AG to NewMetall Holding AG.

Questions

- Does this spin-off violate the lock-up period resulting from the transfer in the underlying facts?

- Can the tax authority waive the reassessment in the event of a violation of the waiting period?

4. Option 3: Timely contribution in kind of Chrom AG to NewMetall

Holding AG

Unlike in Option 1, is Chrom AG immediately contributed as a contribution in kind to NewMetall Holding AG after the stake in Eisen AG has been transferred to Metall Holding AG?

Question

- Does this spin-off violate the lock-up period resulting from the transfer of the equity interest within the group?

5. Option 4: Transfer and Replacement Acquisition of Real Estate

Silver AG owns property No. 300, which is leased to Gold AG. This property has been used entirely for operational purposes by Gold AG for years. The market value of property No. 300 is CHF 800,000, with a book value of CHF 200,000.

Plot No. 300 was transferred from Silber AG to Gold AG at book value via an asset transfer within the meaning of Art. 69 FusG.

Shortly thereafter, Gold AG sells the property to a third party. Gold AG then acquires replacement property No. 1400 from Silber AG at a book value of CHF 1,200,000 (market value CHF 2,200,000), which it will henceforth again use entirely for business purposes.

Questions

- Can the transfer of property No. 300 be carried out on a tax-neutral basis?

- Does the replacement acquisition violate the lock-up period resulting from the group transfer?

6. Option 5: Sale to a foreign intermediate holding company

Metall Holding AG is a group company of Commodities plc, a company incorporated under the laws of Jersey with tax residency in Switzerland. Commodities plc holds 90% of Copper Ltd. through a UK intermediate holding company (UKCo). The remaining 10% of Copper Ltd. is held by Metall Holding AG.

It is intended that the 10% stake in Copper Ltd. be sold to UKCo at a book value of CHF 20 million (market value: CHF 40 million).

7. Option 6: Foreign Control

How would Option 5 be assessed if Commodities plc were also resident abroad for tax purposes?