1. Facts

B. AG, headquartered in the canton of Nidwalden, was wholly owned by A., a resident of the canton of Nidwalden, and acquired a hotel property in Germany from A. pursuant to a purchase agreement dated December 10, 2003, for a purchase price of EUR 4,610,000, or CHF 6,851,382. Purchase costs of

CHF 285,545 were added to the purchase price. This resulted in total

acquisition costs of CHF 7,136,927. However, the hotel property was not recorded in the financial statements of B. AG at its actual acquisition cost, but only at the amount of CHF 1,865,995. Between 2004 and 2014, the book value of the property was continuously adjusted. When the property was sold in 2015 as part of the liquidation of B. AG, the book value was CHF 3,426,930.

The mortgage debt for the hotel property in the amount of EUR 4,577,973 was assumed by A. A recourse claim resulting from the assumption of the debt was not asserted by A. and was not reported in the financial statements of B. AG as a liability to A.

The sale of the property in 2015 resulted in gross proceeds of CHF 5,702,094 and, after deducting the book value of CHF 3,426,930, a book profit of CHF 2,275,164. The book profit was credited directly to the current account or the loan of shareholder A.

The Nidwalden Cantonal Tax Office treated the realized liquidation gain of CHF 2,275,164 as a taxable liquidation dividend for income tax purposes for shareholder A. for the 2015 tax year, on the grounds that previously hidden capital contributions had been made to the liquidated B. AG.

Questions

- Can hidden capital contributions also be repaid tax-free under Art. 20(3) DBG?

- What challenges and follow-up questions arise in tax practice?

1. Facts

In June _3, B. founded C. AG with a share capital of CHF 150,000, consisting of 1,500 shares with a par value of CHF 100 each. Upon incorporation, B. agrees with A. that A. will acquire 750 shares of C. AG at a par value of CHF 75,000 as of January 1, _4, and will commence employment with C. AG. At the time of C. AG’s incorporation, A. is employed by another company and must still terminate the existing employment relationship.

Question

- How should the shares of C. AG acquired by A. be treated for tax purposes?

C. AG was founded several years ago. A begins salaried employment with C. AG as of January 1, _4, and on December 29, _3, purchases 750 of the total 1,500 shares of C. AG from B. at a par value of CHF 100 per share.

A and B enter into a shareholders’ agreement stipulating that the shares in C. AG held by the parties may not be sold, pledged, or otherwise encumbered. In addition, the parties agreed on a mutual right of first refusal with a purchase price based on the net asset value.

As of December 31, _3, the market value according to KS 28 of the SSK is

CHF 369,299 and the net asset value is CHF 173,312 (in each case for 750 shares of C. AG).

In the opinion of the Cantonal Tax Office, A.’s acquisition of the shares results in income from employment of CHF 278,007, based on the market value according to KS 28 of the SSK and taking into account the social security contributions owed.

Question

- Does A. face income tax consequences upon the acquisition of the shares of C. AG? If so, how is the income determined?

Question

- How are genuine employee shareholdings taxed as part of assets?

A. is employed by C. AG as CEO and, in March of year _3, acquires 100 shares of C. AG under an employee stock ownership plan at the recognized formula value of CHF 1,000 each (as of 12/31/_2) with a discount of 25.274% for the intended lock-up period of 5 years, i.e., at a purchase price of CHF 747.26 per share, totaling CHF 74,726.

In March of the year _7, C. AG is sold to a new investor, and A. receives a total sale price of CHF 500,000 for his 100 shares. The formula value as of Dec. 31, _6 is CHF 3,000 per share.

Variation: The shares of C. AG are not sold until 5 years later, in _9.

Question

- Does the sale of the shares in C. AG result in income tax consequences for A.? If so, how is the income determined?

A. is employed as CEO at D. AG and, in _6, acquires 142,500 shares of the group company F under a “management participation program” (MPP) for an amount of DKK 2,850,000, which corresponds to CHF 604,427. In November _9, A. acquires 9,928 warrants at a price of DKK 427,500 as part of a “top-up investment” in addition to his previous investment. Due to a relaunch of the D. employee participation program under the title “The New Beginning,” the previous investment is converted in _12, and A. receives shares and warrants of the group company K.

In _14, the D. Group goes public. The shares and warrants acquired by A. under the employee participation program are converted into “IPO Shares” valued at DKK 7,283,860, which A. sells in the same year, _14.

In the tax year _14, the Cantonal Tax Office calculates additional income from employment for A., deviating from the tax return filed. The tax calculation is based on the fact that, as a result of the D. Group’s initial public offering, A. received IPO Shares with a value of

DKK 7,283,680 (CHF 1,190,153), resulting in additional taxable

income from employment for A. (CHF 590,015 according to the assessment, or CHF 502,277 following the appeal decision).

A., however, assumes that this constitutes a tax-exempt capital gain and disputes the tax offset against income.

Questions

- How should A.’s MPP shares be classified for tax purposes?

- Can A. realize a tax-free capital gain in connection with the IPO and the sale of the IPO shares?

1. Facts

Leo AG is headquartered in the canton of Appenzell Ausserrhoden (AR) and is engaged in the distribution, marketing, sale, and financing of real estate, the trade in building materials, and the holding of equity interests. It is wholly owned by the Tiger Foundation, which is headquartered in the Principality of Liechtenstein. This foundation, in turn, is also the beneficial owner of Anstalt Jaguar. Anstalt Jaguar is also headquartered in the Principality of Liechtenstein. Among other activities, Anstalt Jaguar is the owner of the “Wild” trademark. This trademark was registered in the Liechtenstein trademark register on September 29, 2015, and trademark protection has been in effect since October 20, 2015, for various countries. On November 7 of the same year, Anstalt Jaguar decided to enter into a license agreement with Leo AG, pursuant to which it granted Leo AG the right to use the "Wild" trademark. The licensee was required to pay an amount of CHF 100,000 for this grant of the right of use and, in addition, to pay an ongoing license fee amounting to 10% of the tax base.

For the 2016 fiscal year, Leo AG reported a profit after taxes of approximately CHF 53,000. During the assessment of Leo AG, the tax authority determined that total license payments of approximately CHF 730,000 had been charged to expenses. Of this amount, the tax authority recognized CHF 73,000 and added CHF 657,000 to taxable profit as a monetary benefit provided to the Tiger Foundation, based in the Principality of Liechtenstein.

Questions

- What considerations did the Federal Supreme Court make in this case, and how did it justify its decision?

- How did the Federal Supreme Court assess the calculation of the monetary benefit?

A. is the sole owner and sole member of the board of directors of D AG.

The Cantonal Tax Office conducted an audit of D AG for the tax periods 2008–2013, which resulted in the recognition of hidden profit distributions.

In September 2017, the Cantonal Tax Office conducted another audit of D AG’s books for the tax years 2014 and 2015 and identified hidden profit distributions to A. totaling CHF 85,509 and to her partner B. totaling CHF 53,148, for a total of CHF 138,658 (among other things, this involved costs for construction consulting not justified by business needs, impermissible or excessive wages paid to A.’s son and another person, and a share for the private use of a property held by the company).

A. filed her own 2014 tax return in March 2016 and her 2015 tax return in November 2016. In these returns, she did not report any investment income from her stake in D AG. In assessment proposals dated November 30, 2018, the tax commissioner added the benefits from D AG attributable to her to her taxable income. The taxpayer agreed to these on January 7, 2019.

Following a notification from the cantonal tax office, the FTA issued D AG an invoice for withholding tax of CHF 48,530 on the total monetary benefits of CHF 138,658 and demanded that the withholding tax be passed on to A. D AG paid the withholding tax, and A. transferred the amount to D AG.

In August 2020, A. filed a request with the cantonal tax office for a refund of the withholding tax paid.

Question

- Can A. claim a refund of the withholding tax? If so, to what extent?

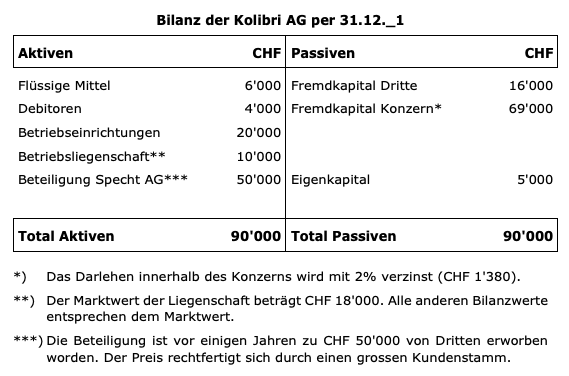

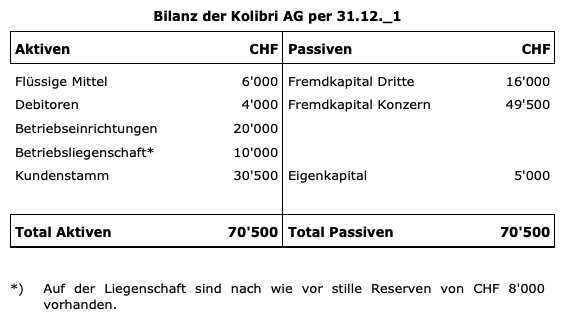

1. Facts

The balance sheet of Kolibri AG as of December 31, _1, shows the following:

Questions

- How is the hidden equity calculated for Kolibri AG in this scenario?

- What are the tax consequences (direct taxes, withholding taxes) for all companies involved if the loan is granted by the domestic parent company?

- Does anything change in this scenario if the parent company’s loan is interest-free?

- What are the tax consequences (direct taxes, withholding taxes) for all companies involved if the loan is granted by a domestic sister company?

- What are the tax consequences (direct taxes, withholding taxes) for all companies involved if the loan is granted by a foreign group company?

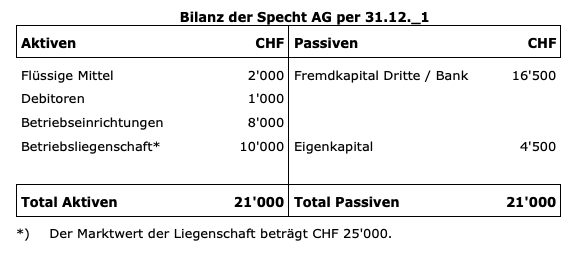

- The loan from the group companies in the amount of CHF 69,000 arose from the purchase of Specht AG. The group financed the purchase of Specht AG through a bank, but Kolibri AG’s parent company had to provide collateral to the bank (in the form of mortgages and/or securities). The bank charges an interest rate of 4% (CHF 2,760) for this loan. Does this arrangement render the calculation of hidden equity invalid, or is there still hidden equity present? In this case, is a profit adjustment also made from a tax perspective, since the 4% interest paid exceeds the interest rates specified in the circular from the Federal Tax Administration (3.75% and 2.25%, respectively)?

- Kolibri AG’s accounting is not kept in CHF but in a foreign currency. Does this circumstance affect the calculation of hidden equity?

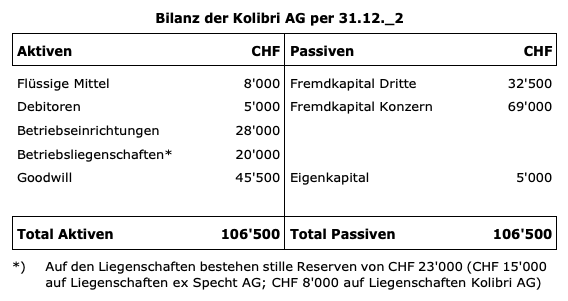

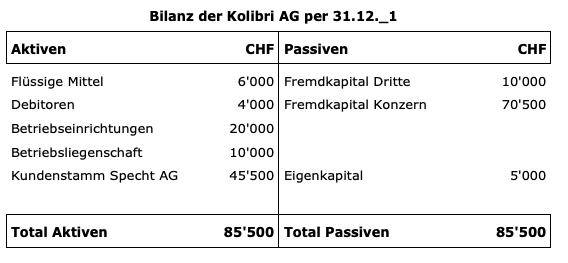

Kolibri AG absorbs Specht AG retroactively as of 01/01/2. Since Kolibri AG does not have sufficient equity, the merger loss is capitalized as goodwill. This is confirmed and recognized by the auditors. This results in the following merger balance sheet.

Note

The tax consequences of a debt push-down are not addressed.

Question

Does this subsidiary absorption change the calculation of hidden equity, and if so, in what way?

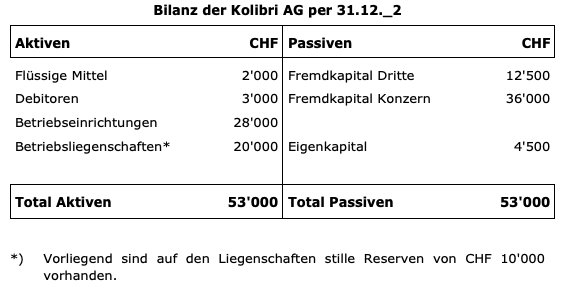

In contrast to the initial examples, current assets have been adjusted.

In this scenario, we assume that Kolibri AG has equity of CHF 50,000 prior to the subsidiary absorption and can therefore write off the merger loss of CHF 45,500 directly against equity (income tax value of Specht AG investment CHF 50,000 vs. Specht AG equity CHF 4,500).

The following balance sheet of Kolibri AG is available as of 12/31/2:

Question

- How is the hidden equity calculated based on this subsidiary absorption?

In this scenario, we assume that Kolibri AG did not acquire Specht AG, but rather acquired the customer base in the amount of CHF 30,500 (=goodwill) as part of an asset deal.

Under this assumption, Kolibri AG’s balance sheet as of 12/31/1 appears as follows:

Question

- How is the hidden equity calculated based on this purchase of the customer base from a third-party company?

The balance sheet is the same as in Variant III. Additionally, the tax office is presented with the statement that the intrinsic value of Kolibri AG (DCF method or income approach) totals CHF 100,000.

Question

- Under this premise, can the group’s entire loan be recognized as debt capital?

In this scenario, we assume that Kolibri AG financed the purchase of Specht AG entirely through third parties and that no collateral was provided by group companies. Since the group has sufficient liquidity in subsequent years, this bank loan is repaid by the group.

Under this assumption, Kolibri AG’s balance sheet as of 12/31/1 appears as follows:

Question

- How is hidden equity calculated based on this scenario? Is there hidden equity?