1.1 Facts

Domestic company X. AG is the debtor under a syndicated loan agreement.

1.2 Questions

- Under what conditions do the loans granted under the loan agreement constitute a bond or cash bond subject to withholding tax?

- What provisions should be included in the loan agreement to ensure that no bond or cash bond exists?

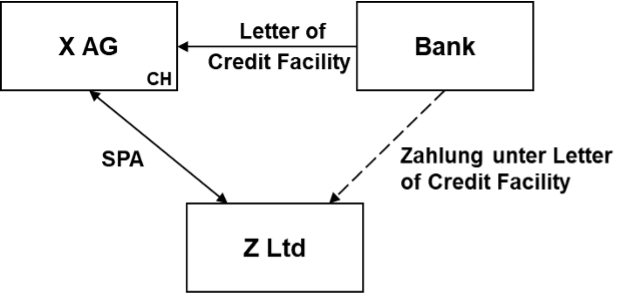

1.3 Option 1

The agreement is a so-called Letter of Credit Facility, which was taken out by X. AG from the foreign company Z. Ltd. for the benefit of the seller (Y. Ltd.) in connection with an acquisition.

If X. AG fails to pay the purchase price to Y. Ltd on time, the latter may demand payment of the purchase price from Z. Ltd (event of default). In this case, Z. Ltd has a claim (immediately due) against X. AG in the amount of the purchase price, which bears interest at 4% per annum.

1.4 Option 2

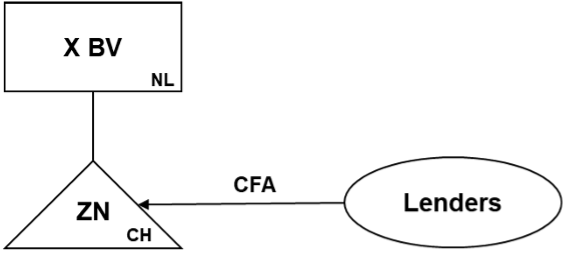

The debtor under the contract is the Swiss Branch, which is registered in the Commercial Register as a branch of a Dutch company (X. BV). X. BV is a group company of an industrial conglomerate that is actually managed in the Netherlands. Must this contract be subject to the 10/20 non-banking rules?

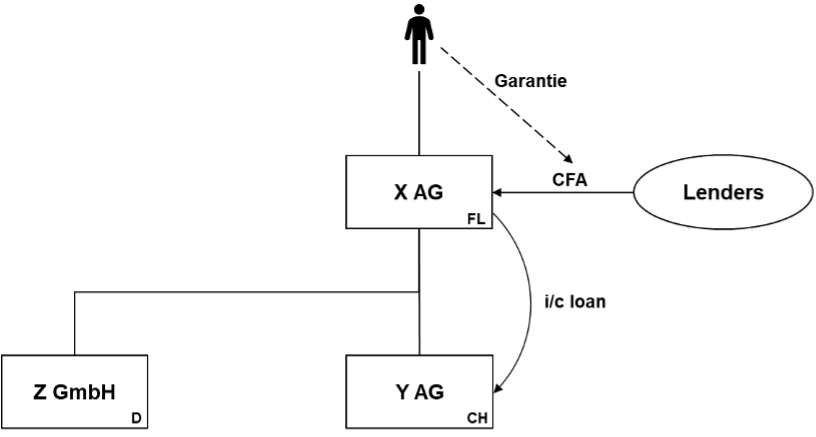

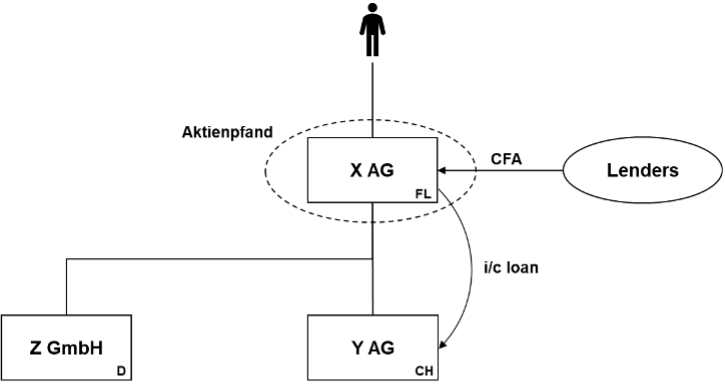

2.1 Facts

X. AG is now a corporation domiciled in Liechtenstein that holds the domestic Y. AG as well as the German Z. GmbH. The shareholder of X. AG is Mr. X, who is domiciled in Liechtenstein and personally guarantees the loan agreement. X. AG transfers the funds raised under the loan agreement to its domestic subsidiary via an intra-group loan.

2.2 Questions

- Under what conditions are interest payments under the loan agreement subject to withholding tax?

- What must be ensured in the agreement so that interest payments are not subject to withholding tax?

2.3 Option 1

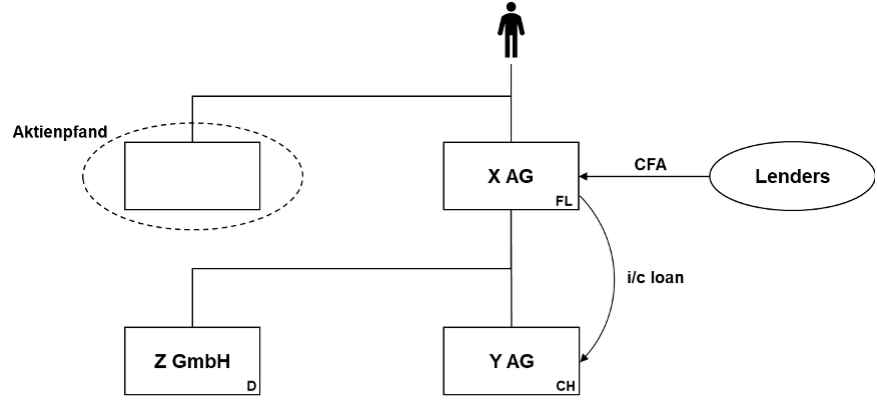

How would the case be assessed if Mr. X did not guarantee the loan agreement but pledged the shares of X AG in favor of the creditors (or made a transfer for security purposes)?

2.4 Variant 2

How should the case be assessed if Mr. X did not guarantee the loan agreement but pledged a securities account held privately by him in favor of the creditors (or made a security transfer)?

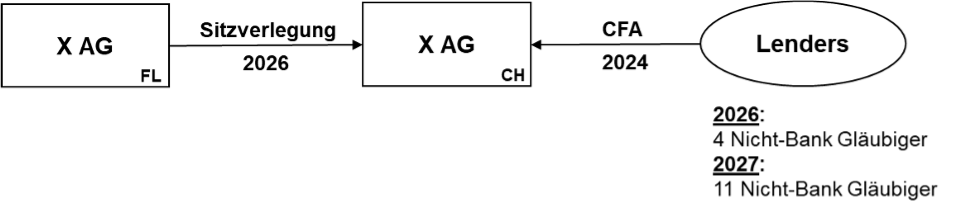

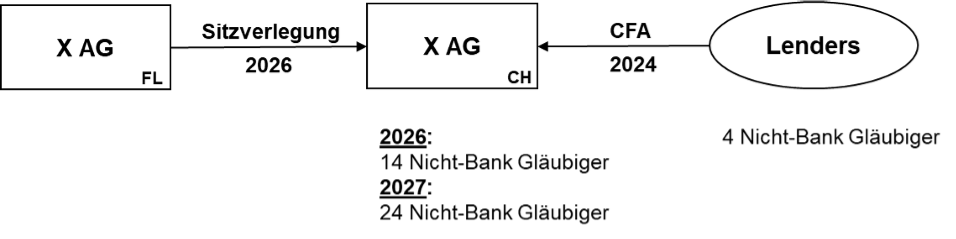

3.1 Facts

X. AG, a Liechtenstein-based company, has been a debtor under a loan agreement (term loan and RCF) with a term of 8 years and more than 10 non-bank creditors since 2024.

In 2026, X. AG relocates its registered office to Switzerland.

3.2 Question

Are interest payments under the loan agreement subject to withholding tax following the relocation of X. AG’s registered office to Switzerland?

3.3 Scenario 1

At the time of the relocation, there are only 4 non-bank creditors under the loan agreement. Only after the relocation to Switzerland do transfers to an additional 7 non-banks occur.

3.4 Scenario 2

At the time of the relocation, there are 4 non-bank creditors under the loan agreement concluded in 2024. At the time of the relocation, X. AG also has an additional 10 long-term liabilities for a fixed amount. With regard to the 20-non-bank rule, it therefore has 14 non-bank creditors.

After the relocation of its registered office, X. AG enters into a loan agreement in 2027, under which there are an additional 10 non-bank creditors.

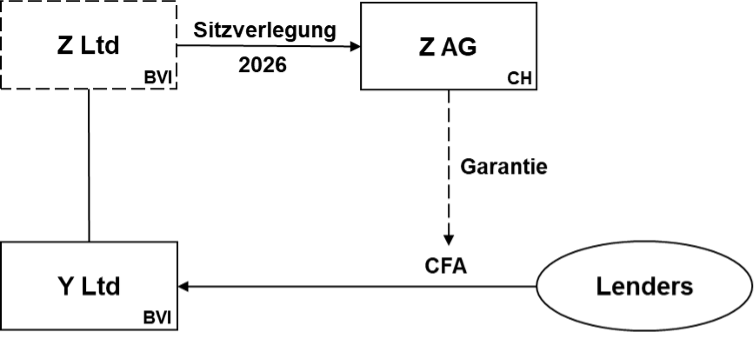

4.1 Facts

Y. Ltd, based in the BVI, is the debtor under a loan agreement concluded in 2024 with more than 10 non-bank creditors, which is guaranteed by Y. Ltd’s parent company, Z. Ltd, also based in the BVI.

In 2026, Z. Ltd relocates its registered office to Switzerland.

4.2 Question

Are interest payments under the loan agreement subject to withholding tax following the relocation of X. AG’s registered office to Switzerland if the provisions regarding the use of funds, as set forth in the FTA circular of February 5, 2019, are violated?

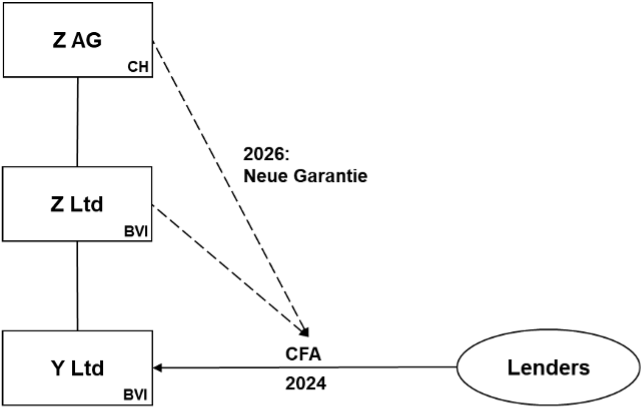

4.3 Alternative

Now, the foreign Z. Ltd is acquired by the newly established domestic Z. AG as part of a quasi-merger (under civil law via a scheme of arrangements). The domestic Z. AG now acts as the guarantor of the loan agreement in place of Z. Ltd.

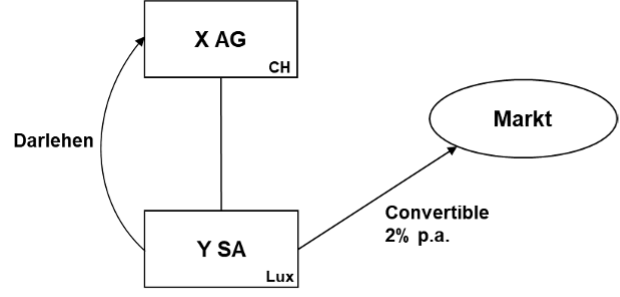

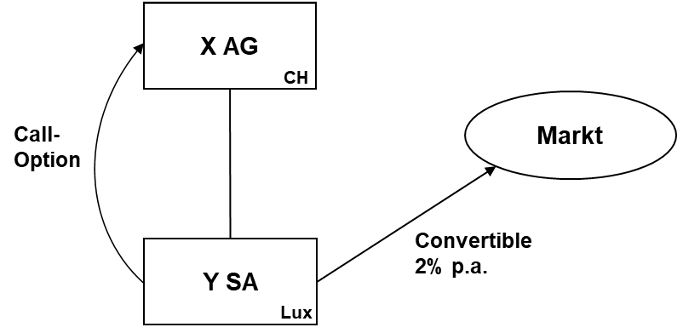

5.1 Facts

Luxembourg-based Y. SA issues a convertible bond (term: 5 years) with an annual coupon of 2% p.a. to more than 10 non-bank creditors in 2026, which is guaranteed by X. AG, the publicly traded domestic parent company of Y. SA. At maturity, investors may convert the convertible bond into shares of X. AG at a price of CHF 1.50. (At the time of the convertible bond’s issuance, the price of X. AG is CHF 1.30 [variant: CHF 2.50]).

In 2026, Y. SA will use the proceeds from the convertible bond primarily to acquire a call option from X. AG, which entitles it to purchase X. AG shares at a price of CHF 0.01.

5.2 Questions

- Is the 2% coupon subject to withholding tax?

- What are the tax consequences in 2031 if the price of X. AG is CHF 3 at that time and the bond is converted into (newly issued) shares of X. AG?

5.3 Alternative

Y. SA does not acquire a call option from X. AG but instead passes the proceeds from the convertible bond on to X. AG as an interest-bearing loan.