1. Facts

In 2015, X sells a classic car with a market value of CHF 1 million for CHF 100,000 from his private assets to X AG (share capital: CHF 100,000), which he owns. It is recorded in the balance sheet of X AG at CHF 100,000.

In 2024, X. AG is liquidated. Its sole asset is the classic car. At that time, it has a value of CHF 2 million (alternative: CHF 500,000).

The liquidation balance sheet of X. AG looks as follows (in TCHF):

Questions

- Is income tax and withholding tax due on the liquidation dividend?

- Would the assessment change if no issue tax had been paid in 2015?

As in the initial facts. However, X. sold X. AG to Y. in 2020.

Question

- Does this change the assessment in any way?

As in the initial scenario. However, X. AG sold the classic car in 2022 for CHF 1.5 million (variant: CHF 900,000) and reinvested the proceeds in shares, which are worth CHF 2 million (variant: CHF 1.5 million) at the time of liquidation in 2024.

As in the initial scenario. However, X. AG is not liquidated; instead, only the classic car (value: CHF 2 million) is distributed as a dividend in kind.

As in the initial scenario. X. sells the classic car not to X. AG, but to Y. AG (a subsidiary of X. AG).

In 2024, both X. AG and Y. AG are liquidated.

X. AG operates Business A and Business B. As part of a de jure (two-stage) split within the meaning of Art. 61(1)(b) DBG, X. AG transfers Business B (market value: CHF 10 million) to Y. AG at a book value of CHF 1 million and distributes the shares of Y. AG to X.

Subsequently, Y. AG is sold to Z. In 2024, Y. AG is liquidated, and Z. receives a liquidation dividend of CHF 5 million.

Question

- Can Z. invoke Art. 20(3) DBG with respect to the hidden reserves contributed to Y. AG as part of this split?

In 2015, X. AG transfers an asset necessary for operations with a book value of CHF 1 million (market value: CHF 4 million) to its subsidiary Y. AG and invokes the restructuring provision of Art. 61(1)(d) DBG (spin-off).

In 2022, X. AG sells Y. AG to Z.

In 2024, Y. AG is liquidated.

Question

- Can Z. invoke Art. 20 para. 3 DBG to the extent of the hidden capital contribution of CHF 3 million?

In 2015, X. converts his business (book value: CHF 1 million; market value: CHF 5 million) into X. AG, a corporation, pursuant to Art. 19 para. 1 lit. b DBG.

In 2022, X sells X AG to Z.

In 2024, X. AG is liquidated.

Question

- Can Z. invoke Art. 20 para. 3 DBG?

1. Facts

For many years, X. has held several buildings with rental apartments in the Canton of Bern as part of his private assets. In the 2023 tax period, he declares these as business assets for the first time.

In 2024, he transfers the properties to X. AG. The properties meet the qualitative and quantitative requirements for a real estate business.

Question

- Can X. invoke Art. 12(4)(a) StHG with regard to real estate gains tax?

1. Facts

The taxable association “Tennis Club” (TC) aims to cultivate and promote the sport of tennis. It operates the clubhouse for its members and also runs a public restaurant there. In addition, it manages the tennis facility, which includes tennis courts and associated amenities. Both the property containing the clubhouse and the separate parcel of land with the tennis facility are owned by the association.

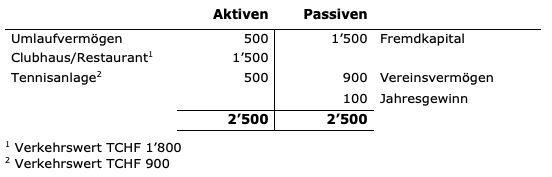

The balance sheet of the TC association is as follows (in TCHF):

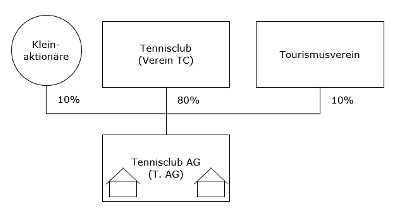

The TC association intends to legally and economically separate its operational activities from the association. It wishes to spin off the operational activities—including the management of the restaurant and the operation of the tennis facility—into a stock corporation, Tennisclub AG (T. AG). In doing so, all real estate is to be transferred along with the operational activities.

As part of the spin-off, the public sector, through the regional tourism association (a taxable association), and private minority shareholders (private assets) will each hold a 10% stake in T. AG. The public sector will subscribe to shares because the tennis club is obligated to make the tennis facility publicly accessible (in particular to tourists). This requirement is secured in the land register by an easement and is supported by the municipality through annual contributions.

The TC association will no longer engage in any operational activities in the future. It will limit itself to supporting members in the maintenance and promotion of tennis and will focus on providing conceptual and financial support for the operation.

In addition to the following transferred assets (book values) of the TC club

- Current assets CHF 100

- Clubhouse/Restaurant TCHF 1,500

- Tennis facility CHF 500

- Liabilities CHF 1,400

the new shareholders are contributing TCHF 350. The TC club owns 80% of the share capital (TCHF 560), while the remaining shareholders hold shares with a par value of TCHF 140.

The target structure is as follows:

Questions

- Can the operations and real estate be spun off into T. AG at book value in a tax-neutral manner under the DBG/StHG?

- Is an issuance tax due as a result of the formation of T. AG?

- Variant: What are the tax consequences under the direct federal tax if all shares of T. AG are sold to an independent third party after three years at a market value of TCHF 1,900?

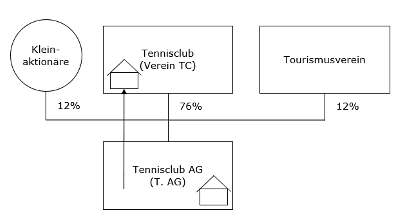

The business and the real estate are held by T. AG. For the shareholder structure, reference can be made to the target structure in the preceding scenario.

The clubhouse and restaurant require renovation. This necessitates a significant investment. The minority shareholders and the public sector are not willing to provide additional equity or provide collateral. However, they have agreed that the clubhouse and restaurant will be transferred to the TC club at book value, while the tennis facility remains with T. AG. In return, their ownership stake in T. AG will be increased by 2% each. The renovation can be financed through contributions from club members and bank financing.

The target structure is as follows:

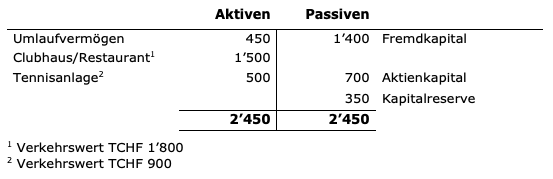

The balance sheet of T. AG is as follows (in TCHF):

Questions

- Can the restaurant operations and the property with the clubhouse/restaurant be sold to the TC Association at book value in a tax-neutral manner under the DBG?

- What are the tax consequences of this transfer and the change in ownership stakes for the minority shareholders and the tourism association?

- Variant: Unlike in the basic scenario, the TC Association is the sole shareholder of T. AG. T. AG is to be merged into the TC Association (at book value). Is this merger possible on a tax-neutral basis under the DBG?

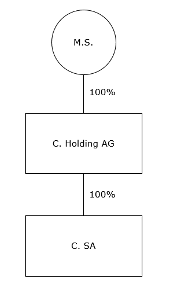

1. Facts

M.S. holds 100% of the shares of C. Holding AG in his private assets. C. Holding AG owns 100% of C. SA.

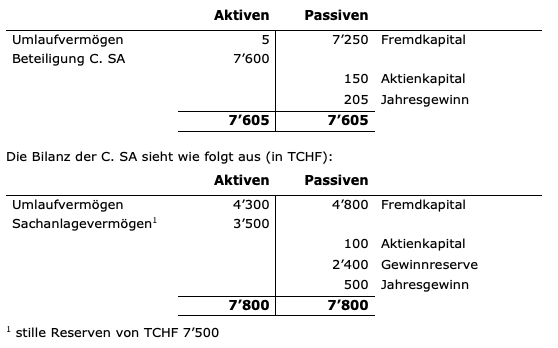

The balance sheet of C. Holding AG is as follows (in TCHF):

A parent company absorption is planned. To simplify the structure, C. Holding AG is to be merged into C. SA as of December 31, 2023, via a reverse merger, with the merger loss being capitalized.

Questions

- What are the tax consequences for shareholder M.S.?

- Scenario 1: On August 28, 2023, C. SA increased its share capital by TCHF 50 to TCHF 150, charged to retained earnings.

- Scenario 2: On February 23, 2024, C. SA increased its share capital by TCHF 50 to TCHF 150, charged to retained earnings.

- Scenario 3: Instead of retained earnings and net income, C. SA has retained earnings of TCHF 2,900. C. SA does not increase its share capital.

- Scenario 4: Unlike in the facts of the case, C. Holding AG has current assets of TCHF 1,000, debt of TCHF 100, and retained earnings of TCHF 8,145. The merger effective date is set as June 30, 2023, on which C. Holding AG prepared its financial statements. How is the taxable capital of C. SA calculated for the period of its fiscal year from January 1 to December 31, 2023?