1. Background

A-AG was founded in 20x1 with its headquarters in ZH by the two founders, A and B, and develops software products for insurance solutions.

In 20x2, the publicly traded Investor-AG acquired a stake in A-AG as part of a strategic partnership. It holds 75% of the shares in A-AG. At the same time, the management team was expanded to include a new CEO (Manager Y) and a CTO (Manager Z), who were also given the opportunity to acquire shares in A-AG (5% each), these being employee shares.

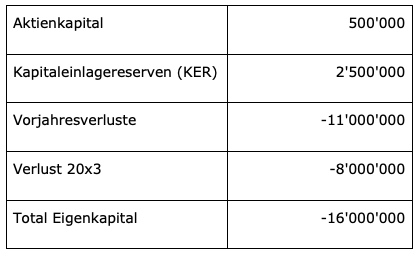

However, A-AG’s software did not develop as hoped. Sales and growth were also sluggish compared to the original forecasts. To cover A-AG’s funding needs, Investor-AG granted A-AG subordinated loans totaling CHF 17 million. As of the end of 20x3, A-AG’s equity is negative (CHF -16 million) and is composed as follows:

In 20x4, Investor AG concludes that an improvement in the overall situation regarding A-AG is unlikely. It seeks to sell its stake in A-AG. Founder B and managers Y and Z express interest in acquiring the shares.

Managers Y and Z are both employed by A-AG. Founder B is not employed by A-AG. He is employed by B-AG, which is wholly owned by him (a one-person company whose sole customer is A-AG).

The transaction is to be structured as follows:

- Investor AG waives repayment of the CHF 17 million loan and grants A-AG an additional interest-free loan of CHF 3 million to ensure liquidity.

- Investor AG sells its shares in A-AG for CHF 1 to founder B and managers Y and Z (25% each).

The transaction is to take place as soon as possible, especially since Investor AG fears that A-AG may go bankrupt, which would damage Investor AG’s reputation as a majority shareholder that invests in many startups and could also result in liability claims against the board members it has appointed.

Questions

- How should the debt waiver be treated at the A-AG level?

- Does the acquisition of A-AG shares result in tax consequences for managers Y and Z?

- Does the acquisition of A-AG shares result in tax consequences for founder B?

Investor AG holds a put option with an exercise price of CHF 1 on the shares of A-AG. How should the exercise of this put option be treated for tax purposes?

1. Facts

Unlike in Case 1, Investor AG retains its shares for the time being, and managers Y and Z have never acquired a stake in A-AG. However, the restructuring of A-AG is unsuccessful. Despite restructuring measures, the company remains on the brink of bankruptcy.

Founders A and B realize that their original idea is not working. Founder A subsequently exits A-AG and transfers his shares to Founder B for CHF 1. Founder B changes the company’s purpose in an attempt to expand into a new business field (while abandoning the old one) and continues to operate A-AG on this new basis.

Questions

- How should the sale of the founder shares from Founder A to Founder B be classified?

- Variation: A-AG is liquidated at the instigation of Investor-AG, and subsequently a new company is founded by B.

1. Facts

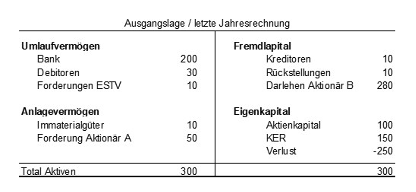

The restructuring of A-AG was unsuccessful. After numerous discussions, the two founders decide to liquidate A-AG. Founder B has a new idea (new business area) and is convinced that he can utilize the developed intellectual property. The final balance sheet prior to the liquidation resolution by the general meeting of A-AG is as follows:

A-AG recorded a 10% allowance for doubtful accounts on its receivables. The receivables from the FTA consist of VAT credits.

Furthermore, there is an estimate of the fair value of the held intellectual property in the amount of 160. The receivable from Shareholder A accrued interest at a rate of 4%.

Questions

- What does the opening balance sheet for liquidation look like?

- Which items do you think require further discussion?

1. Facts

B-AG is founded by shareholders residing abroad and in Switzerland and, in the initial phase, is also “managed” by the shareholders residing in Switzerland.

Going forward, management will be handled solely by a shareholder residing abroad, and the shareholder residing in Switzerland will step back (retaining only their supervisory role as a member of the board of directors).

Questions

- How do you assess the facts from the perspective of income tax and withholding tax?