- VAT/Customs

- Entreprises

VAT issues in M&A transactions

Note: This language version is an automatically generated translation. The text may therefore contain linguistic and terminological errors.

view in original language (German)Note: This language version is an automatically generated translation. The text may therefore contain linguistic and terminological errors.

view in original language (German)VAT is often underestimated in M&A transactions - but can have a significant financial impact. These case studies use practical constellations to show how issues such as reporting procedures, tax succession, input tax deduction and company sales should be assessed from a VAT perspective. Among other things, complex restructurings, asset deals and special features of investment and finance companies are dealt with. The solutions provide you with clear guidelines for recognizing VAT risks and handling transactions correctly.

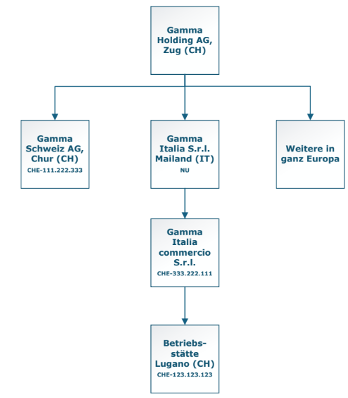

The Gamma Group is an international company with subsidiaries in numerous countries that support the trade in building materials. Previously, the building materials were produced within the group itself. Following a restructuring in 2000, the production companies were spun off or sold, so that activities now focus on distribution and trade.

The group structure in Europe currently looks as follows:

In light of the strategic realignment and the current cost structure, Group management has decided to restructure the trading activities in Europe to increase efficiency and leverage synergies. To this end, various subsidiaries are to be merged. As part of these measures, the Swiss trading company Gamma Schweiz AG, Chur (CH), is to be integrated into the existing Italian subsidiary Gamma Italia S.r.l., Milan (IT) (merger in accordance with the Swiss International Private Law Act).

Gamma Schweiz AG owns a factory site in Chur (CH) with a market value of CHF 150 million. Ten years ago, the factory was renovated for CHF 50 million and adapted for commercial use. Subsequently, the company leased the site—with an option (Art. 22 MWSTG)—to external third parties. The input tax incurred and claimed in connection with this renovation totaled CHF 11 million.

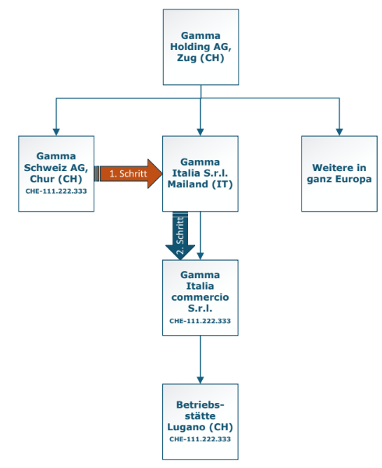

The following steps are planned as part of the restructuring:

Step 1

Gamma Schweiz AG will merge with Gamma Italia S.r.l. (Italy). This merger is planned to be effective retroactively as of January 1, 2025, for tax purposes. Registration in the Italian Commercial Register is scheduled for mid-June 2025. The registered office of Gamma Italia S.r.l. is located in Milan (Italy). Following the merger, Gamma Schweiz AG will be removed from the Swiss Commercial Register. Deregistration from the VAT register will take place as of September 30, 2025.

Step 2

Gamma Italia S.r.l. (It) will then merge as of November 30, 2025, with Gamma Italia commercio S.r.l., Milan (It), which is also domiciled in Italy. Gamma Italia commercio S.r.l. (It) also operates a permanent establishment in Lugano (CH). Gamma Italia commercio S.r.l. (It) has been registered in the Swiss VAT register since January 1, 2020; the permanent establishment in Switzerland has also been registered in the Swiss VAT register since January 1, 2021. The cantonal tax authorities of Graubünden have confirmed a tax-neutral transfer of the factory premises to the permanent establishment of Gamma Italia commercio S.r.l.

The following steps are illustrated graphically:

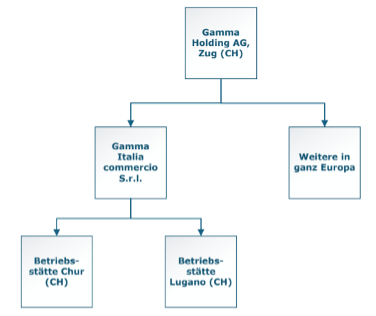

The final structure is as follows:

The lease agreements for the factory premises will be amended as of January 1, 2026; Gamma Italia commercio S.r.l., Italy, will now act as the lessor. VAT will continue to be shown separately in the lease agreements (exercise of the option pursuant to Art. 22 of the Swiss VAT Act).

Müller AG operates two self-contained business divisions: a carpentry shop and a furniture store. As part of a strategic realignment, Müller AG transfers the carpentry shop, including inventory and staff, to Odermatt AG, an independent third party, for a purchase price of CHF 3 million. One year after closing, the Federal Tax Administration (FTA) discovers during an audit that Müller AG had not reported VAT on the carpentry shop’s sales prior to the sale. Two years after the sale, Müller AG goes bankrupt.

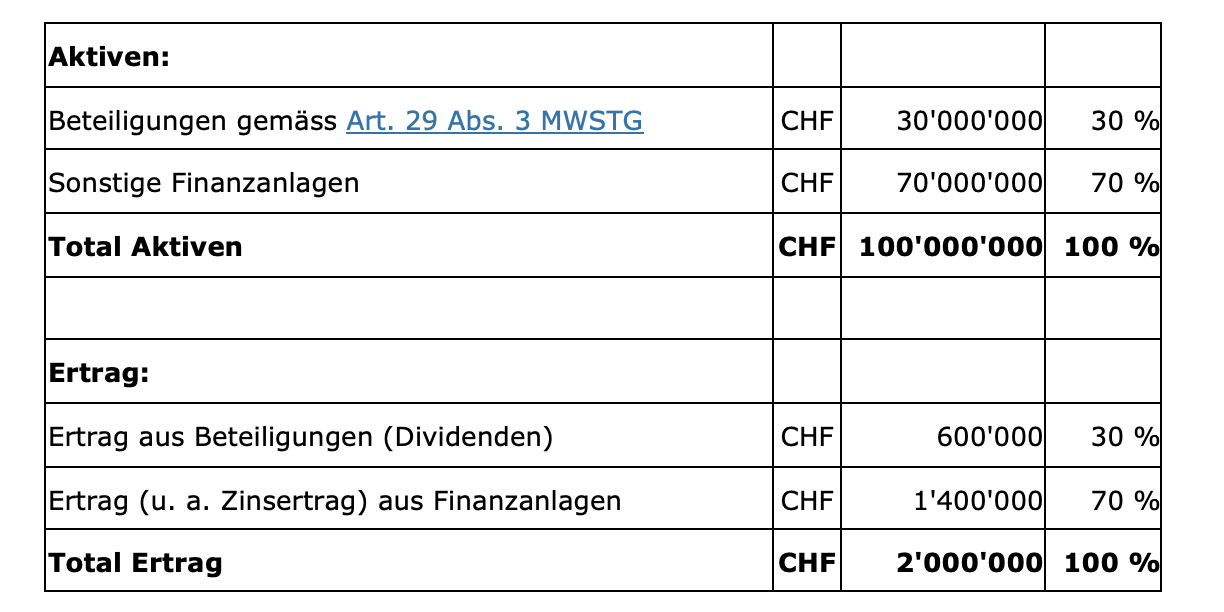

Finanz AG holds various financial investments; it does not engage in any other activities. The assets and income of Finanz AG are composed as follows:

This case is based on Example 3 of VAT Info 09, Section 2.2.4.4.

During the relevant fiscal year, Finanz AG incurred input tax-bearing expenses on which a** total of CHF 200,000 in input tax** is levied. This input tax breaks down as follows:

CHF 30,000 in input tax can be directly allocated to the acquisition, holding, and disposal of equity investments (e.g., M&A advisory, due diligence).

CHF 70,000 in input tax can be directly allocated to the management of financial investments (e.g., custody fees, specific financial advisory services).

CHF 100,000 in input tax relates to general overhead costs (infrastructure, IT, general administration, audit) that are used for both areas.

Hans Müller is the owner of Müller Schreinerei AG, based in Bern, and intends to retire from business life. Against this backdrop, the operational business is to be sold. The company’s current assets also include several properties that are leased to third parties.

Reto Schwarz, who works as a foreman at Müller Schreinerei AG, has expressed interest in taking over the business. Since he lacks the financial means to purchase shares, the parties agree on a sale of the business (asset deal) directly from the corporation. The agreed purchase price consists of a fixed portion of CHF 100,000 and a variable portion amounting to 25% of the pre-tax profit generated over the next two years (earn-out). Over the past five years, the average pre-tax profit has been CHF 200,000. The properties leased to third parties remain the property of Müller Schreinerei AG and are not included in the transferred business. The commercial property where the carpentry business is operated will be leased to the purchaser following the transfer. The business transfer takes place on May 1, 2026. Subsequently, Mr. Schwarz establishes a limited liability company (Schwarz Schreinerei GmbH) and contributes the acquired assets to it. The limited liability company is entered in the Commercial Register on May 25, 2026, and is also listed in the VAT Register from that date onward.

In the two years following the transfer of operations, the GmbH generates a pre-tax profit of CHF 150,000 each year. After that, revenue declines significantly and falls below the relevant threshold of CHF 100,000 in the third year. For this reason, the GmbH is removed from the VAT register at the beginning of the fourth year.

Hans Müller’s wife, Dr. Silvia Müller, is a general practitioner and runs her own practice. She also wishes to retire and is selling her practice to her successor. Dr. Silvia Müller is registered in the VAT register due to the dispensing of medications. Her successor, Dr. Xaver Imstepf, will not continue selling medications and therefore will not register in the VAT register. The sale price is agreed upon as CHF 1 million.

This is broken down as follows:

Business fixed assets CHF 650,000

(X-ray machine, ultrasound, etc.)

Medications CHF 50,000

Acquisition of customers (goodwill) CHF 300,000

How should this sale be classified for VAT purposes? Does Dr. Müller have to account for the payment with VAT?