1. Facts

Disrupt AG, headquartered in the Canton of Zurich, is a startup in the field of artificial intelligence development. It was founded jointly by Anna, Ben, and Clara at the beginning of 2016 as an ETH spin-off. Anna, Ben, and Clara all reside in the Canton of Zurich. At the time of founding, each held a one-third stake. Anna is the CEO of Disrupt AG, Ben is the head of the development department (CTO), and Clara handles finances and the recruitment of investors (CFO).

To meet ongoing capital needs, private equity investors subscribed to additional shares in Disrupt AG as part of capital increases in 2020 and 2022, so that the three founders now each hold 20% and the investors hold 40%.

Disrupt AG operated at a loss until 2023 and was therefore continuously reliant on capital, which was provided in the form of equity and debt. A modest profit of CHF 50,000 is projected for 2024. Disrupt AG has 12 employees, including the founders.

Anna, Ben, and Clara, all of whom work at Disrupt AG, paid themselves a relatively low salary of CHF 60,000 per year through 2022. In 2023, the gross salary was increased to CHF 120,000 per founder (all working full-time).

The market-standard salary is CHF 220,000 for Anna and CHF 200,000 for Ben and Clara.

In 2024, a potential exit is on the horizon. A U.S. technology company wishes to acquire 100% of the shares in Disrupt AG. The U.S. technology company intends to leverage the emerging breakthroughs in development for its own office software.

The share purchase agreement stipulates a purchase price of CHF 20,000,000 for all shares of Disrupt AG. The purchase price is divided equally among the shareholders, meaning Anna, Ben, and Clara each receive a share of the purchase price of CHF 4,000,000 (a total of CHF 12,000,000 for the founders).

50% of the purchase price attributable to the founders (i.e., CHF 6,000,000) will be deposited in an escrow account for two years (“holdback”). During this period, the salary for the three founders will be CHF 150,000. In addition, a two-year non-compete clause is agreed upon and enforced with a contractual penalty.

In the event of early termination, the escrow amount is forfeited (100% if terminated in the first year and 50% if terminated in the second year) and is transferred back from the escrow account to the buyer. This holdback applies only individually; for example, if Anna terminates early, Ben and Clara do not lose their entitlement.

Questions

- As an advisor, what would you recommend to the founders when drafting the share purchase agreement?

- Outline the income tax consequences resulting from the sale of the shares for Anna, Ben, and Clara.

- Do you see any tax issues related to continued employment and the escrow in the event of early termination?

1. Facts

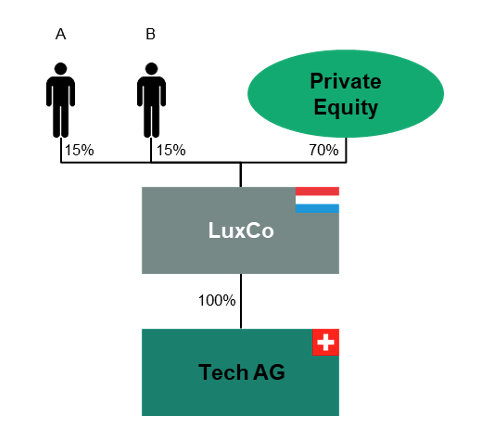

Tech AG is owned 50% each by its founders A and B (both founders are residents of Switzerland). As of July 1, 2024, A and B sell their shares to LuxCo, an acquisition vehicle for a private equity fund, for CHF 50 million. A and B receive 70% of the purchase price in cash (i.e., CHF 35 million), the remainder is settled with 30% of the shares in LuxCo, i.e., the founders each contribute 15% of their shares in Tech AG to LuxCo and receive LuxCo shares in return.

The founders remain employed by Tech AG, with salaries in line with market rates. There is a shareholders’ agreement among the LuxCo shareholders, which contains the usual clauses such as purchase rights and obligations (drag-along/tag-along), voting thresholds, etc. However, there are no continued employment obligations and no obligations to return the shares in LuxCo (i.e., no good leaver or bad leaver clauses). Furthermore, no non-compete clause is agreed upon.

LuxCo is financed with 30% equity and 70% debt (bank loans). There are no preferred shares.

Variant: Good-leaver and bad-leaver clauses are agreed upon in the shareholders’ agreement, pursuant to which A and B must sell 5% of their shares (i.e., a total of 10%) to the fund at a fixed formula price. There are no such repurchase obligations on the remaining shares.

As of** June 30, 2028** (exactly four years later), the shareholders sell all shares in LuxCo to a third party for CHF 100 million.

Questions

- What are the income tax consequences of the sale of Tech AG for A and B?

- How can A and B’s minority stakes in LuxCo be classified from a tax perspective? What should be taken into account?

- Explain the tax consequences of the sale of the minority interests in LuxCo for A and B.

1. Facts

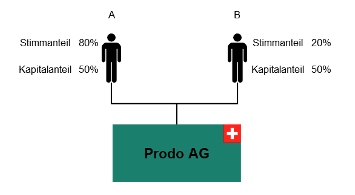

A and B are the founders of Prodo AG, a startup based in the Canton of Zurich that develops CAD software for the manufacture of hearing aids and dental implants. A and B are also residents of the Canton of Zurich. Both hold 50% of the capital shares; however, A holds an 80% voting majority through his voting shares (share capital of CHF 100,000, 400 voting shares with a par value of CHF 125 and 100 common shares with a par value of CHF 500, A holds all 400 voting shares and B holds all 100 common shares.):

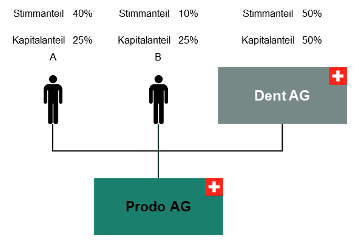

Both founders are employed by Prodo AG and receive a market-rate salary. Dent AG, a publicly traded manufacturer of dental implants, is one of Prodo AG’s most important customers and wishes to strengthen its ties with the company. It therefore acquires half of the voting rights and half of the capital shares from both A and B. Following this transaction, the ownership structure is as follows:

Dent AG pays the two founders a total purchase price of CHF 10 million, with A receiving CHF 6,000,000 and B receiving CHF 4,000,000. Under the share purchase agreement, A and B commit to continuing to work for Prodo AG for another two years and additionally agree to a non-compete clause.

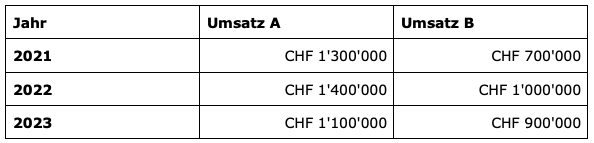

Variation: Prodo AG has no preferred shares, and A and B hold exactly 50% of the capital and voting shares; nevertheless, the same asymmetrical purchase price distribution applies as in the previous case. Prodo AG is an eye clinic, and A and B are ophthalmologists at Prodo AG. A and B receive a relatively low fixed salary of CHF 80,000 per year. The remainder of their compensation depends on the revenue they generate, with both doctors maintaining separate division-level accounting. Immediately prior to the sale, the revenue figures were as follows:

After the sale, A and B receive a market-rate salary and agree to a temporary non-compete clause.

Question

What are the income tax consequences for A and B resulting from the sale of the shares in Prodo AG?

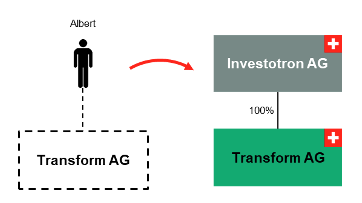

1. Facts

On May 15, 2024 (date of the binding agreement), Albert sells 100% of the shares in his startup "Transform AG" to the investment company "Investotron AG" for CHF 5,000,000. Prior to the sale, Albert held the shares in his private assets and was the company’s founder. The financial statements as of December 31, 2023, had not yet been prepared at the time of sale; the profit for 2023 is expected to be CHF 800,000. As of May 15, 2024, non-operating assets amount to CHF 1,400,000.

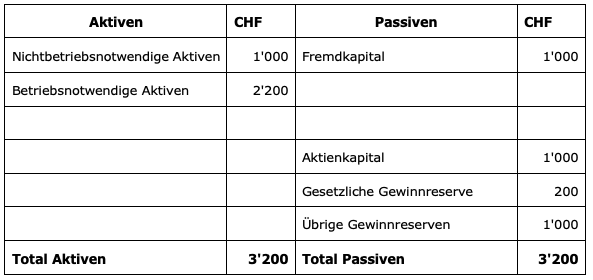

The balance sheet of Transform AG as of December 31, 2022, prior to the sale, can be presented as follows:

Following the sale, Transform AG distributes a dividend of CHF 1,300,000 to Investotron AG on July 15, 2024, based on the now available 2023 financial statements.

Questions

- Assess the tax consequences of the dividend distribution on June 15, 2024.

- Variation: The sale takes place on July 1, 2024. The 2023 financial statements have not yet been approved by the general meeting.

1. Facts

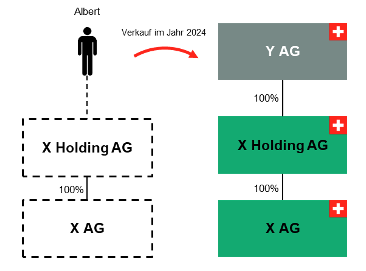

Albert holds 100% of the shares in X Holding AG. X Holding AG is a holding company and, in turn, holds 100% of the shares in X AG. Albert founded X AG as a startup in 2016 and has been its CEO since its founding. In 2018, he contributed X AG to X Holding AG as part of a contribution-in-kind formation (alternative: in March 2024). To avoid income tax consequences under the principle of transposition, the contribution was made solely against X AG’s share capital of CHF 100,000 existing at the time of the contribution.

On July 15, 2024 (transaction date), Albert sells 100% of the shares in X Holding AG to Y AG for CHF 5,000,000.

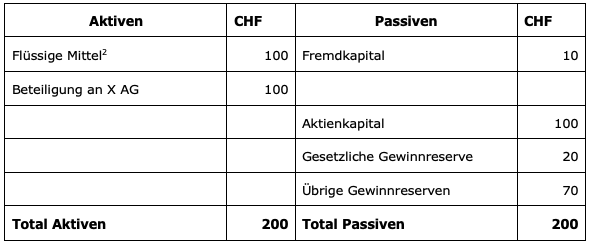

The approved 2023 financial statements of X Holding AG are available as of the date of sale. The balance sheet of X Holding AG as of December 31, 2023, can be presented as follows:

2For simplicity’s sake, it is assumed that this item has neither increased nor decreased between the balance sheet date (December 31, 2023) and the date of sale (July 15, 2024).

The approved 2023 financial statements of X AG are available as of the date of sale. The balance sheet of X AG as of December 31, 2023, can be presented as follows:

3For simplicity’s sake, it is assumed that this item has neither increased nor decreased between the balance sheet date (December 31, 2023) and the date of sale (July 15, 2024).

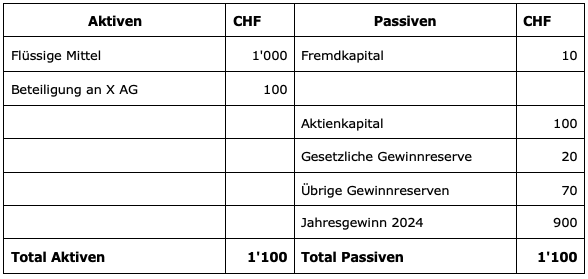

On July 20, 2024 (i.e., after the sale), X AG pays a dividend of CHF 900 to X Holding AG. The balance sheet of X Holding AG as of December 31, 2024, can be presented as follows:

Based on the balance sheet as of December 31, 2024, X Holding AG pays a dividend of CHF 900,000 to Y AG on July 15, 2025.

Question

Assess the income tax consequences for Albert of the CHF 900,000 dividend paid by X Holding AG to Y AG.

1. Facts

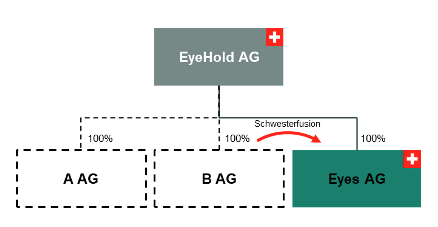

The Eye Group, consolidated under EyeHold AG, operates various eye clinics in Switzerland. In the past, it acquired various eye clinics that were operated as corporations, including A AG and B AG. The sellers were always natural persons residing in Switzerland. At the time of sale, A AG and B AG each had non-operating assets eligible for distribution under commercial law amounting to CHF 500,000 and hidden reserves of CHF 300,000 each.

EyeHold AG wishes to simplify the structure. To this end, the target companies are to be absorbed into the main operating company, Eye AG. Eye AG is also a subsidiary of EyeHold AG.

Variant: Eyes AG is the parent company of the absorbed A AG and B AG (subsidiary absorption).

Variant 2: Eyes AG (sister company) reports a (qualified) capital loss under Art. 725a of the Swiss Code of Obligations (restructuring merger).

Variant 3: A AG was established in 2022 (two years prior to the sale) via a tax-neutral conversion retroactive to January 1, 2022. On May 14, 2024, A AG is sold by its founder to Eyes AG for a price of CHF 1,000,000.

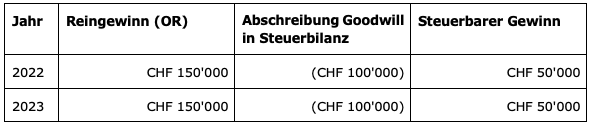

The sale triggers income tax consequences for the founder on the hidden reserves existing at the time of the conversion (Art. 19 para. 2 DBG). The amount of hidden reserves at the time of conversion is decisive. The sale triggers income tax consequences for the founder based on CHF 500,000.

This refers to the goodwill existing and contributed at the time of sale (no hidden reserves on assets/debt), which must now be taxed due to the violation of the lock-up period. A AG generates a profit of CHF 150,000 in each of the years 2022 and 2023; however, due to the amortization of the CHF 500,000 goodwill (straight-line over 5 years at 20% per year), it is taxed “only” CHF 50,000 in each year on the tax balance sheet:

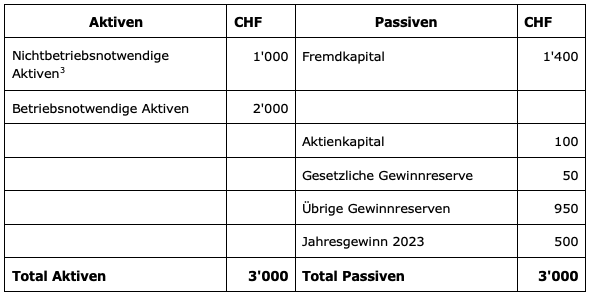

The net assets available at the time of sale and distributable under commercial law (as of the balance sheet date of December 31, 2023) amount to CHF 250,000 (total annual profits of CHF 300,000 minus the statutory reserve of 50% of the share capital of CHF 100,000). The remaining amount of goodwill capitalized in the tax balance sheet amounts to CHF 300,000 at the time of sale. In June 2024, A AG distributes a dividend of CHF 250,000 to EyeHold AG (Variant 4: A AG is liquidated).

Questions

- Do the sister company mergers result in tax consequences for the sellers? If so, to what extent?

- Variant: Does the subsidiary merger result in tax consequences for the seller? If so, to what extent?

- Variant 2: Are there any tax consequences resulting from the sister merger (restructuring merger)? If so, to what extent?

- Variants 3 and 4: Do the distribution or liquidation of A AG result in tax consequences for the sellers? If so, to what extent?

Case 7: Integration of the Target

(Based on VGer ZH SB.2022.00060 of October 4, 2023.)

1. Facts

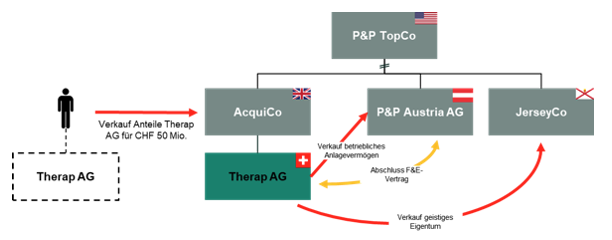

Therap AG, headquartered in Zurich, is a biotech company specializing in the development of innovative therapeutic agents. The company was founded in 2013.

On June 16, 2024, it was acquired by the publicly traded U.S. pharmaceutical group Peters & Peters through a specially established acquisition company based in the UK for a price of CHF 50,000,000.

On the same day, Therap AG entered into an agreement with the newly founded P&P Austria AG, an Austria-based group company of Peters & Peters, under which it agreed to provide

- general and administrative services related to the distribution of P&P Austria AG’s products, and

- to conduct research and development, with the research results belonging to P&P Austria AG.

Therap AG will be compensated for these services on a cost-plus-10% basis. An annual profit after taxes of CHF 100,000 is expected. Based on the contracts entered into, the newly established P&P Austria AG is expected to generate a profit of CHF 800,000 per annum.

On June 16, 2024, Therap AG also sold all "Intellectual Property Rights" (IPR) and "Non-Viral Contracts" to P&P Jersey Ltd., a group company of the corporate group based in Jersey, for a price of CHF 25 million. The book value of the intellectual property is CHF 10,000,000 and corresponds to the capitalized research costs.

Finally, Therap AG also sold all remaining operating assets to P&P Austria AG. Since the remaining operating assets showed a net liability at book value, Therap AG additionally compensated P&P Schweiz AG for this transfer with CHF 1 million.

In the consolidated annual report, Peters & Peters allocated the purchase price for the stake in Therap AG as part of the so-called Purchase Price Allocation (PPA) as follows:

- CHF 40 million for intellectual property and non-viral contracts

- CHF 500,000 for operating fixed assets

- CHF 9.5 million cannot be allocated to specific assets (i.e., goodwill)

Questions

Identify the potential income tax consequences for Therap AG arising from the following transactions:

- a. Sale of intellectual property

- b. Sale of fixed assets

- c. Conclusion of an agreement regarding general/administrative services and contract research (R&D).