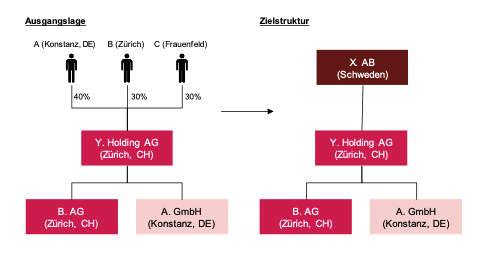

1. Facts

X. AB (Sweden) plans to acquire 100% of the shares in Y. Holding AG (Zurich). The current shareholder structure of Y. Holding AG is as follows1:

- 40% of the shares are held by A, a resident of Konstanz (Germany),

- 30% of the shares are held by B, a resident of Zurich, and

- 30% of the shares are held by C, a resident of Frauenfeld.

The Y. Group is an IT company, with its core activities carried out by B. AG (Zurich) (owner of the IP and customer contracts). A. GmbH is a service provider that develops software on behalf of B. AG. Y. Holding AG is a pure holding company.

The structure can be simplified as follows:

Y. Holding AG was founded in 2010 by A and B. C (Managing Director) acquired the shares in 2020 from A and B at their market value at the time (EBITDA x8 multiple minus net debt).

1 These findings are derived, among other sources, from the share register, old purchase agreements, and similar documents.

The purchase agreement is currently scheduled to be signed in Q2 2024. The parties have agreed in a letter of intent that the purchase price shall be determined based on the consolidated Swiss GAAP FER financial statements as of December 31, 2023 (locked-box mechanism). The EBITDA multiple method (multiple of 10) is to be used to calculate the *enterprise *value. The transaction is expected to close shortly after the purchase agreement is signed.

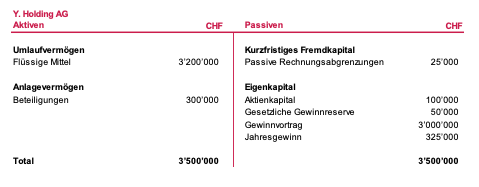

The statutory balance sheet of Y. Holding AG as of December 31, 2023, presented the following picture:

Questions

- What are the income tax consequences for the sellers resulting from the sale of the shares in Y. AG?

- What must X. AB, as the buyer, take into account, and how can it factor in the potential tax consequences/risks during negotiations?

- Would your recommendation change if a closing account mechanism had been agreed upon instead of a locked-box mechanism?

1. Facts

As part of the due diligence process, you requested the cost of acquisition overview1. It presents the following picture:

In the Swiss GAAP FER financial statements, the investments are carried at their historical cost (B. AG at CHF 3 million and A. GmbH at CHF 1 million).

1 Often an attachment to the tax return or a separate statement.

Question

What does X. AB, as the buyer, need to consider?

1. Facts

As part of the due diligence process, you have gained the following insights1:

- The sellers’ legal and consulting fees incurred to date in connection with the sale were billed to Y. Holding AG (CHF 250,000 in 2023).

- The Y. Group has not yet prepared a transfer pricing study. Your analysis of intra-group transactions has revealed that the compensation paid to A. GmbH by B. AG has been too high over the past two years (CHF 160,000 per year).

Question

What should X. AB, as the buyer, take into account?

1 These findings can be obtained through a discussion with management or, among other things, by reviewing the following documents: contracts, balance sheets, and, if applicable, bank statements, as well as a separate overview from the target company regarding intra-group transactions.

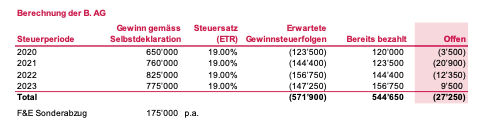

1. Facts

As of December 31, 2023, B. AG has recognized a provision for current taxes in the amount of CHF 35,608. Based on the tax documents received, you have gained the following insights:

- B. AG has filed its tax returns through 2022.

- The company has received final tax assessments through 2019.

- For the years 2020 through 2022, the company claimed a special R&D deduction of CHF 175,000 per year.

- In Q1 2024, the Zurich Tax Office raised several questions regarding B. AG’s activities and, in its assessment decision dated March 15, 2024, for the year 2020, determined that the underlying personnel costs do not qualify for the special R&D deduction. Accordingly, the special R&D deduction was corrected in the assessment decision for the year 2020.

- The assessment decision was not taken into account in the calculation of the tax provision as of December 31, 2023.

- The tax provision is calculated using a tax rate of 19%.

The tax provision calculation received showed the following:

Question

What does X. AB, as the buyer, need to consider?

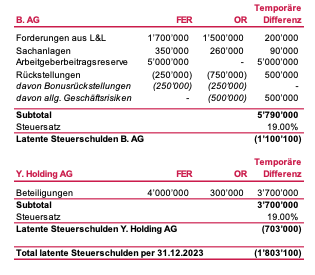

1. Facts

The consolidated Swiss GAAP FER financial statements as of December 31, 2023, show the following deferred tax items (assumption: A. GmbH has no deferred tax items):

Question

What does X. AB need to consider as the buyer?