1. Background

In the case of extensive real estate portfolios that have previously been held privately, the question may arise—particularly in the context of estate planning—as to whether these should be transferred to business assets and, if so, subsequently converted into a corporation.

The transfer of investment real estate into a real estate company is therefore a key issue in estate planning. Indirect real estate ownership is not always more tax-advantageous than direct investments in every scenario. Furthermore, the transfer may give rise to tax consequences.

The following statutory provisions must be observed regarding the taxability of real estate gains:

- Art. 16(3) DBG: Capital gains from the sale of private assets are tax-exempt.

- Art. 18(2) DBG: Income from self-employment also includes all capital gains from the sale, realization, or book revaluation of business assets.

- Art. 58(1)(a) DBG: Taxable net income consists of the balance of the income statement.

Question

Only the sale of real estate held as part of private assets is tax-exempt (excluding real estate gains tax). What are the advantages of transferring such assets to business assets or contributing them to a legal entity?

Mr. L (residing in Meggen/LU; single, two adult children) and Mr. B (residing in Saanen/BE; single, one adult son) have been friends since school and are successful entrepreneurs (resulting in an annual income of CHF 2 million, received as salary). They meet for dinner on the eve of their class reunion and discuss the real estate portfolios they have built up over the years (their entire net worth is currently tied up in real estate). At present, they hold the properties directly in their personal estates (the requirements for commercial real estate trading are clearly not met).

Mr. L’s Real Estate Portfolio

Mr. B’s Real Estate Portfolio

Question

Mr. L and Mr. B are wondering whether the current income tax burden could be reduced if the properties were transferred to a real estate company (“Immobilien L AG” and “Immobilien B AG,” respectively) (the costs of the transfer will not be addressed here).

2.1 Background

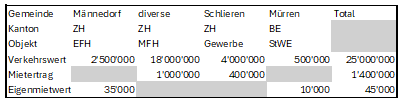

Ms. H is 68 years old. In 1995, she inherited three apartment buildings, among other assets, from her father. Thanks to her successful career as a self-employed attorney specializing in divorce law, she had the necessary resources to build up a substantial real estate portfolio over the years. In addition to a spacious single-family home in Männedorf (her residence) and a vacation apartment in Mürren, the portfolio includes six multi-family homes and a commercial property in several municipalities in the Canton of Zurich. Market value: CHF 25 million. Rental income: CHF 1.4 million; imputed rental value: CHF 45,000. Ms. H has consistently declared the properties in the real estate schedule of her tax return.

Ms. H’s Real Estate Portfolio

Ms. H has three children who get along well with one another. Her daughter Petra is a self-employed property manager. In light of her advancing age, Ms. H wishes to settle her estate and intends to sell her properties to a real estate company (Immo AG) that she has founded. Some of the properties are in dire need of renovation. Costly renovation work is scheduled for the coming years.

Questions: Basic Facts

- What considerations and decisions need to be made prior to the transfer?

- What tax consequences should Ms. H expect?

- Can it be assumed that the properties constitute personal assets, or is there a risk that the tax authorities will treat them as business assets?

- Would the situation change if the properties were classified as business assets?

- What options become available after the properties are transferred to a legal entity?

The facts are analogous to those in the basic scenario. Alternatively, the apartment buildings and the commercial property to be transferred to Immobilien H AG are located in the canton of Lucerne (market value of CHF 22 million and property tax assessed value of CHF 17 million). Ms. H is still unsure what should happen to the properties after they are transferred to Immobilien H AG. A possible sale in three years cannot be ruled out. In the event of a transfer, Immobilien H AG would capitalize the acquisition costs as the book value under commercial law.

Questions

- Can the properties be transferred to Immobilien H AG, which is held by Ms. H, without triggering capital gains tax consequences?

- What considerations and decisions must be made prior to the transfer?

3.1 Facts

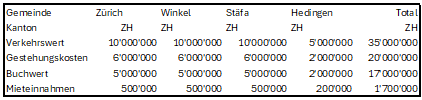

Ms. M. (divorced) resides in the Canton of Zurich and owns several properties in the Canton of St. Gallen (see below). Ms. M. has two children (K1 and K2) who also reside in the Canton of Zurich. She is not dependent on the income from the properties.

- Multi-family home in Rohrschach (SG): Market value CHF 10 million; unencumbered

- Multi-family home in St. Gallen (SG): Market value CHF 20 million; encumbered by a mortgage of CHF 10 million.

- Multi-family home in Wil (SG): Market value CHF 20 million; recently underwent a comprehensive renovation (investment volume CHF 5 million), although the majority of the outstanding contractor invoices have not yet been paid (the contractors are becoming increasingly concerned about the outstanding payments)

Ms. M. heard from an acquaintance that it is now possible to transfer real estate to a real estate company without tax consequences. The properties are to be transferred to her children, K1 and K2, after her death.

Questions

- Can the properties be transferred to Immobilien M AG without triggering real estate gains tax? What steps should be taken, and what should be kept in mind?

- Should the deferred taxes be considered as consideration?

- Is the capital gains tax deferred in full, or is the deferral limited to the hidden reserves attributable to K1 and K2?

- Can the properties be recorded on the balance sheet of Immobilien M AG at fair market value? What would be the tax consequences regarding the deferred capital gains tax?

- Do the transferred hidden reserves constitute capital contribution reserves?

4.1 Facts

X. (born in 1960) purchased six multi-family residential properties in the canton of Zurich between 2000 and 2020 as a long-term capital investment. In 2020, the projected net rents amounted to CHF 1.5 million, which X. reported as part of her personal assets.

In 2022, X. received an inheritance, after which she promptly acquired four additional properties in the canton of Zurich with projected net rents of CHF 1.0 million. She commissioned Z. AG to manage her entire real estate portfolio (leasing, rent and utility billing, collections, administration, property maintenance, and cleaning, etc.) for a fee of CHF 100,000 per year.

In 2025, X. declared the properties as business assets for the first time, with projected net rental income of CHF 2.5 million.

X. intends to transfer the real estate portfolio (at its tax value) retroactively as of January 1, 2026, to the newly to-be-established X. AG.

Questions

- Can X. claim a tax deferral due to restructuring for the Zurich real estate gains tax in connection with the transfer of the real estate portfolio to X. AG?

- For purposes of federal direct tax, is X. engaged in self-employment?

- Are the rental income subject to social security contributions, and what should X. consider in this regard with a view to the intended transfer?

- What would be the tax consequences at the cantonal level if the properties were located in the canton of Aargau?

5.1 Facts

Mr. K. (widowed), 72 years old, owns an extensive real estate portfolio in the canton of Zurich (a monistic canton). The properties clearly constitute business assets derived from commercial real estate trading. They are recorded in the accounting records. Mr. K. does not wish to bequeath business assets to his children due to the tax and social security implications and therefore intends to transfer the properties to his personal assets.

The following key details are known:

Questions

- What tax consequences can Mr. K. expect?

- Would the tax consequences change if the properties were located in a canton with a dualistic tax system?

- Can Mr. K. apply for liquidation taxation?

- What alternatives are there to a private withdrawal?