- Entreprises

Pre-deal carve-outs and carve-ins incl. Pillar 2

Note: This language version is an automatically generated translation. The text may therefore contain linguistic and terminological errors.

view in original language (German)Note: This language version is an automatically generated translation. The text may therefore contain linguistic and terminological errors.

view in original language (German)How can complex pre-deal structures be optimally structured from a tax perspective - and where are the biggest pitfalls lurking? These case studies will guide you through key issues relating to carve-outs, carve-ins and the effects of BEPS Pillar 2 in M&A transactions. From demergers and share distributions to withholding tax and DTA issues, practical scenarios are systematically prepared. The solutions provide you with concrete approaches and valuable insights for the tax structuring of complex transactions.

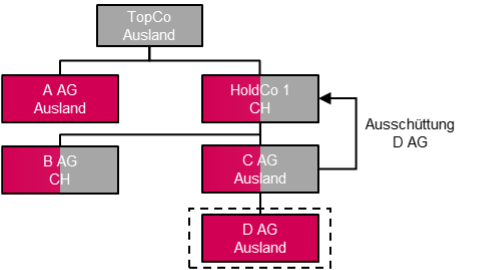

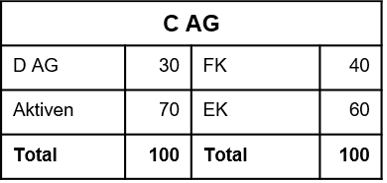

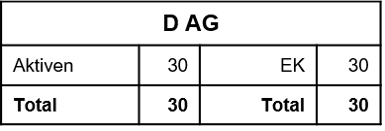

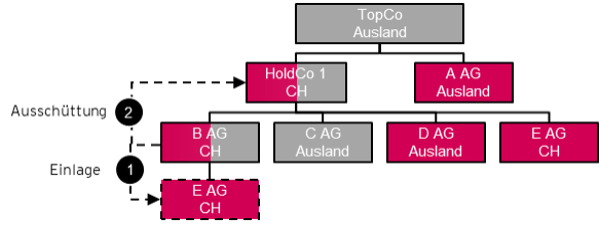

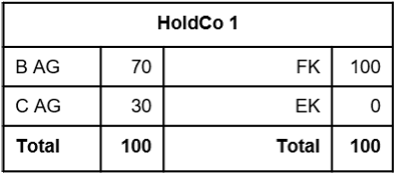

In view of the planned demerger, C AG distributes its equity interest in D AG to HoldCo 1 at fair value.

The income is recognized as investment income at the HoldCo 1 level.

The companies do not report any hidden reserves.

The TopCo group of companies is considered a taxpayer for the purposes of the OECD minimum tax. The taxable business entity for the purposes of the IIR (Income Inclusion Rule) pursuant to Articles 2.1 through 2.3 of the GloBE Model Rules is TopCo. In Switzerland, the Swiss supplementary tax applies.

The income is recognized as a substantive dividend at the HoldCo 1 level.

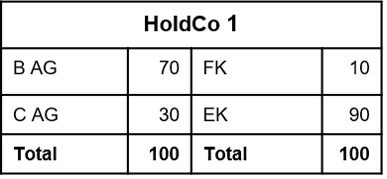

What are the implications for income tax and BEPS Pillar 2 at the HoldCo 1 level?

Prior to the planned distribution by D AG, C AG’s prior-year profit of 10 is distributed to HoldCo 1 as an ordinary dividend.

The ordinary dividend is recorded as dividend income at the HoldCo 1 level.

C AG’s cost basis is 50. The book value remained unchanged from the previous period and, like the income tax value, remains at 30.

The reported equity of C AG is 30.

The companies do not have any hidden reserves.

What are the consequences for income tax and BEPS Pillar 2 at the HoldCo 1 level, assuming that the group had previously exercised the Equity Investment Inclusion Election?

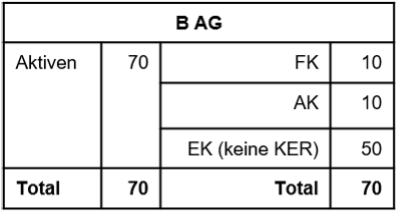

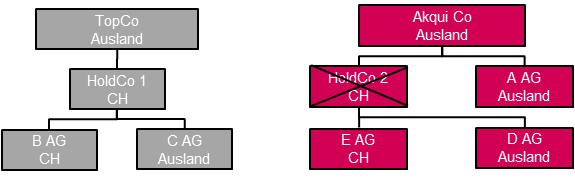

A division of B AG is spun off under an old-law spin-off. E AG is newly established for this purpose (tax neutrality is assumed).

In the past, B AG was written down by 10 at the HoldCo 1 level. This write-down is partly related to the business unit to be spun off (however, a precise allocation to the spun-off or remaining business is no longer possible).

Due to poor business performance in recent years, tax loss carryforwards of 30 have accrued (however, a precise allocation to the spun-off or remaining business is no longer possible).

The tax loss carryforwards could not be capitalized under IFRS due to various uncertainties regarding the future profitability of B AG. However, as a result of the spin-off, it is expected that approximately 50% of the tax loss carryforwards can be utilized within the group in the future. Accordingly, a deferred tax asset was recognized.

The TopCo group is considered a taxable entity for the purposes of the OECD minimum tax. The taxable business entity for the purposes of the IIR (primary supplementary tax regime) pursuant to Articles 2.1 through 2.3 of the GloBE Model Rules is TopCo. In Switzerland, the Swiss supplementary tax applies.

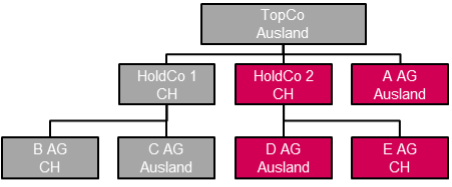

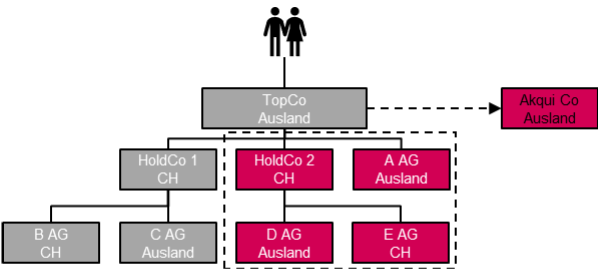

A detailed discussion of the split of HoldCo 1 CH has been omitted, as tax neutrality is generally assumed. HoldCo 1 and HoldCo 2 now exist.

Prior to the restructuring, HoldCo 1 qualified as a securities dealer because the book value of its equity investments as of December 31, 2025 (as well as in previous years) exceeded CHF 10 million.

As part of the restructuring (holding split retroactive to January 1, 2026), HoldCo 1 now holds only investments with a total book value of less than CHF 10 million.

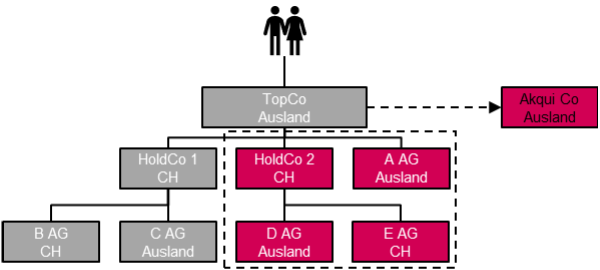

Prior to the sale, the spun-off business unit is restructured as shown below. Control over the business unit has not yet been relinquished.

The spun-off Akqui Co, along with its investments, continues to be listed within the TopCo Group but is no longer consolidated line by line. The discontinued business segment is classified as “Discontinued Operations” or “held for sale” in accordance with IFRS 5 and is reported separately.

The discontinued business unit generates consolidated revenue of well over EUR 1 billion. The remaining business unit generates revenue of approximately EUR 3 billion.

The planned sale is to take place as a share deal.

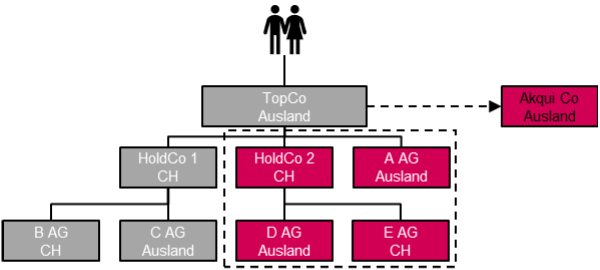

TopCo is resident in a country with which Switzerland has concluded a double taxation treaty.

For the past five years, TopCo has met three key substance criteria that, according to FTA practice, are relevant for assessing treaty eligibility:

However, the shareholders of TopCo are not resident in a DTA country.

Does the sale of TopCo to AkquiCo affect TopCo’s treaty entitlement with respect to withholding tax?

TopCo meets only two of the relevant substance tests (functional and balance sheet substance). It can be assumed that it is eligible for treaty benefits prior to the sale.

Prior to the sale (when treaty eligibility still existed), HoldCo 1 had distributable funds under commercial law that were not clearly necessary for operations in the amount of 100.

After the sale (until the planned dividend distribution), an additional 300 in funds distributable under commercial law were generated.

Following this sequence of events, HoldCo1 distributes a dividend of 400 to TopCo.

TopCo established HoldCo 1 in 2021 to acquire B AG.

This purchase was financed through an intra-group loan.

Assumption: In the absence of treaty eligibility, this constitutes a case of extended international transposition.

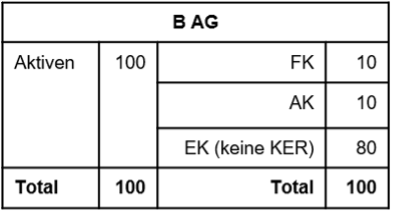

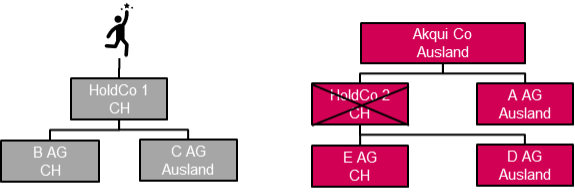

Following the sale of HoldCo 2 and A AG, a dividend of 80 is to be distributed by B AG to HoldCo 1.

Balance Sheet (Acquisition of C AG)

Balance sheet (after the sale)

After the sale, TopCo only meets the balance sheet substance criterion (30% equity).

Assumption: At least two substance tests must be met to establish treaty eligibility.

One year later, during which no dividends were distributed, TopCo takes measures to build up its workforce.

TopCo is not resident in any DTA country.

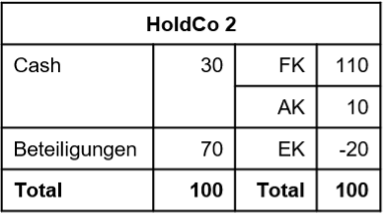

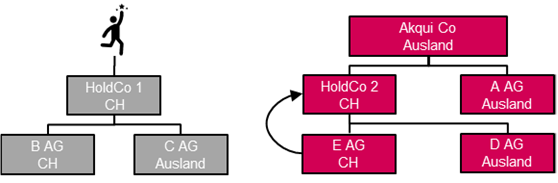

The buyer (AkquiCo; treaty-eligible) acquired HoldCo 2 in 2025 for 90, solely because of the two equity interests.

The buyer therefore intends to liquidate HoldCo 2 (a liquidation plan was already in place at the time of purchase).

There are hidden reserves amounting to 100 on the equity interests in E AG and D AG.

Balance Sheet 2024 (prior to sale)

What are the tax consequences from the perspective of income and withholding taxes?

HoldCo 2 is not to be liquidated; instead, E AG is to merge with HoldCo 2 (upstream merger).

The seller is now a natural person resident in Switzerland who holds the equity interests in their private assets.

The buyer intends to liquidate HoldCo 2 (a liquidation plan was already in place at the time of purchase).

What are the tax consequences from the perspective of income and withholding taxes?

HoldCo 2 is not to be liquidated; instead, E AG is to merge with HoldCo 2 (upstream merger).

What are the tax implications from an income tax perspective?