1. Facts

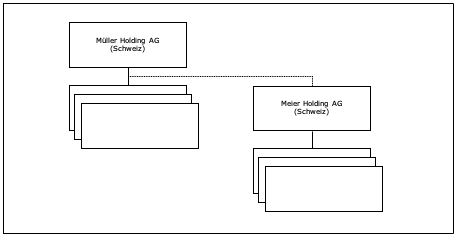

The Müller Group, consisting of Müller Holding AG, headquartered in Switzerland, and various subsidiaries in Switzerland and abroad, intends to acquire the Meier Group. The target group consists of Meier Holding AG, headquartered in Switzerland, and various subsidiaries in Switzerland and abroad. Legally, Müller Holding AG acts as the buyer, offering one newly created Müller Holding AG share and CHF 20 in cash for each share of Meier Holding AG.

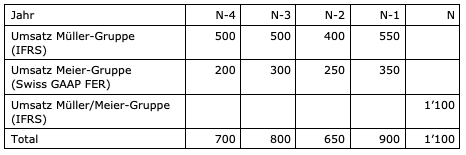

The revenues of the two groups are as follows (each converted to EUR), with the Müller Group using IFRS as its accounting standard and the Meier Group using Swiss GAAP FER.

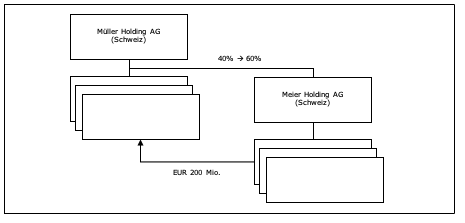

Same facts as in Option 1. The Müller Group already holds a stake of approximately 40% in the Meier Group (or its parent company, Meier Holding AG). There is already active mutual business activity between the Müller Group and the Meier Group. Of the Müller Group’s consolidated revenue, approximately EUR 200 million comes from transactions with the Meier Group. The Müller Group intends to increase its stake from the current 40% to 60%.

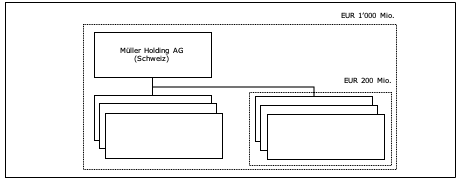

In recent years, the Müller Group has generated consolidated revenue equivalent to approximately EUR 1,000 billion. As part of a strategic realignment, it intends to completely spin off part of the business and list it on the stock exchange as the Meier Group. The Meier Group is expected to have consolidated revenue of approximately EUR 200 million in its first year.

Question

How is the revenue of EUR 750 million, which is relevant for determining subjective tax liability, calculated in each of the scenarios?

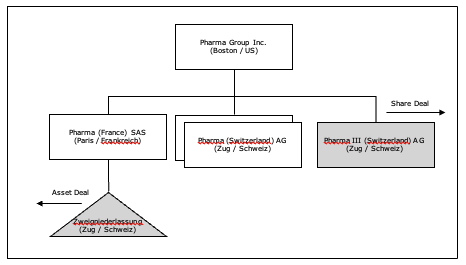

1. Facts

The U.S.-based Pharma Group Inc., headquartered in Boston, USA, has three subsidiaries in Switzerland as well as a permanent establishment of a French subsidiary. As part of a restructuring of its European business, the following transactions are planned:

- Transaction 1: Sale of the subsidiary Pharma III (Switzerland) AG to a Basel-based pharmaceutical group as part of a share deal;

- Transaction 2: Sale of the business operations of the branch office as part of an asset deal to the Swiss subsidiary of a French pharmaceutical group;

All groups involved are subject to the minimum tax due to their global revenue, and the subsidiaries as well as the permanent establishment of Pharma Group Inc. in Switzerland form a VAT group.

Questions

- How should these transactions be assessed under Art. 6 of the Minimum Tax Ordinance (joint liability)?

- How should these transactions be assessed under Art. 15(1)(c) of the VAT Act (joint liability)?

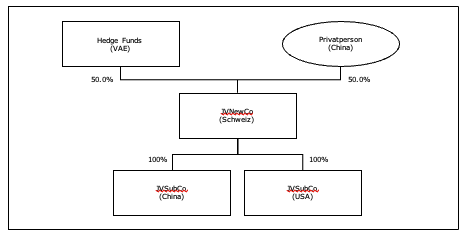

1. Facts

Year 1

A hedge fund from the United Arab Emirates (UAE), which is not yet subject to the global minimum tax due to a turnover of less than EUR 750 million and prepares its consolidated financial statements in accordance with IFRS, and a Chinese private individual wish to develop a drug for a rare disease. To this end, in Year 1 they establish a joint venture in the form of a stock corporation headquartered in Baar, Canton of Zug, with each investor holding 50% of the capital and voting rights (alternative: the Chinese private individual holds 50.1% of the capital and 50% of the voting rights).

Year 3

In the third year, the hedge fund based in the United Arab Emirates makes a major acquisition, which means it is now subject to the global minimum tax due to the additional revenue.

Year 6

The joint venture proves successful, and starting in the sixth year, the company generates recurring revenue of approximately EUR 1,000 million from the marketing of the drug. In the seventh year, the joint venture establishes a subsidiary in Shanghai, China, and another in Boston, USA, for the distribution of the drugs.

Question

How do you assess this situation from the perspective of Swiss supplementary tax?

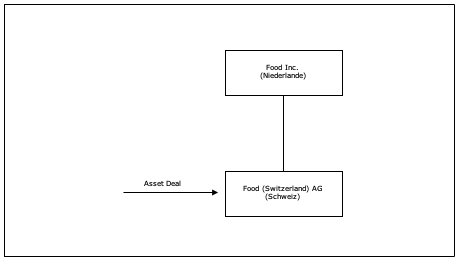

1. Facts

The Swiss subsidiary (pre-tax rate: 20%) of a Dutch food conglomerate acquires the dog food business from a Swiss competitor as part of an asset deal. Part of the acquired assets is the “Leckerli” brand, whose purchase price is set at CHF 1 billion in the contract. According to a ruling, the buyer may amortize the brand for tax purposes over 10 years. The Dutch group prepares its financial statements in accordance with IFRS.

Questions

- How do you assess this situation based on the GloBE model rules?

- How could this issue be resolved based on the Minimum Tax Regulation (MindStV)?

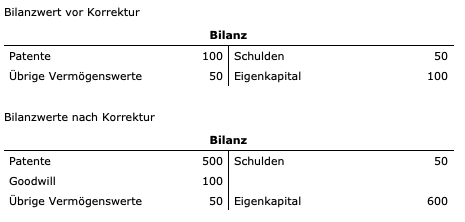

1. Facts

A pharmaceutical group subject to the global minimum tax and preparing its consolidated financial statements in accordance with IFRS acquires a Swiss stock corporation with IFRS equity of CHF 100 million for a price of CHF 600 million as part of a share deal. According to purchase price allocation (“PPA”), the premium of CHF 500 million is allocated as follows: CHF 400 million to the patents held by the company and CHF 100 million to goodwill. The transaction took place on December 15, 2021.

Question

How do you assess this share deal from the perspective of Swiss supplementary tax?

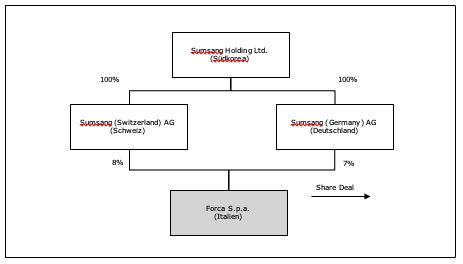

1. Facts

The South Korean Sumsang Group has grown significantly in the past due to numerous M&A transactions and therefore has a very complex corporate structure. Among other holdings, it owns a 15% stake in the Italian company Forca S.p.A., which it intends to sell at a significant capital gain. 8% of the shares are held by Sumsang (Switzerland) AG, based in Switzerland, and another 7% by the German company Sumsang (Germany) AG.

Questions

- How do you assess the sale of the 8% stake by Sumsang (Switzerland) AG from the perspective of Swiss supplementary tax?

- Does the assessment change if the group held only a 20% stake in Sumsang (Germany) AG?

- Does the assessment change if the 8% stake consists of voting shares and the 7% stake consists of common shares?