- Entreprises

News on the taxation of corporate restructurings (2026)

Note: This language version is an automatically generated translation. The text may therefore contain linguistic and terminological errors.

view in original language (German)Note: This language version is an automatically generated translation. The text may therefore contain linguistic and terminological errors.

view in original language (German)In practice, corporate restructurings raise a variety of tax issues - in particular when shareholdings are spun off, real estate is converted, sister companies with loss carryforwards are merged or demergers are completed by selling at a lower price. Using practical case studies, Stefan Oesterhelt and Daniel Strahm show what tax consequences are associated with the spin-off of participations (including minority participations of less than 10%), when it is possible to invoke Art. 12 para. 4 lit. a StHG for real estate gains tax and under what conditions the conversion of an ordinary company into an AG can be tax-neutral. It also deals with mergers with loss carryforwards and cantonal differences in Basel, Berne and Zurich. The solutions provide you with the necessary tools to plan complex restructurings safely and to recognize tax obstacles at an early stage.

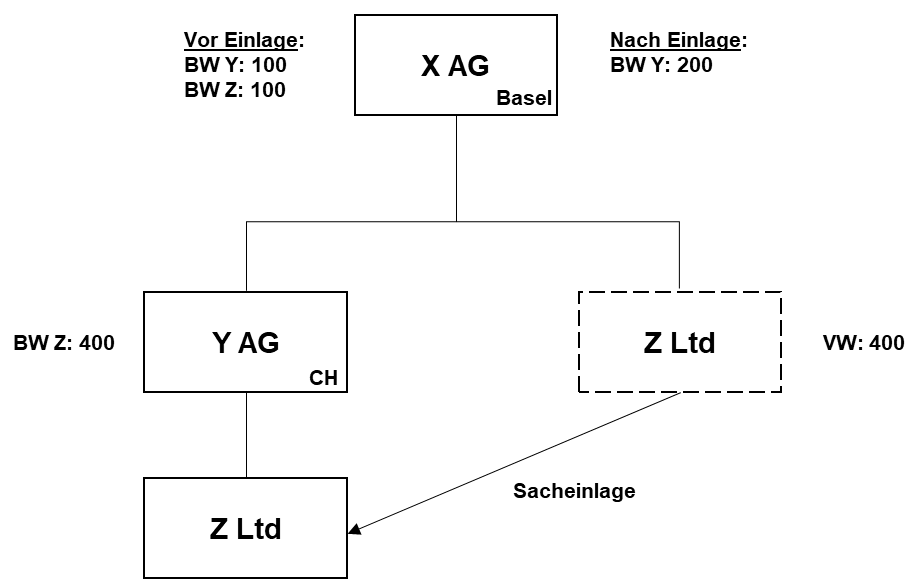

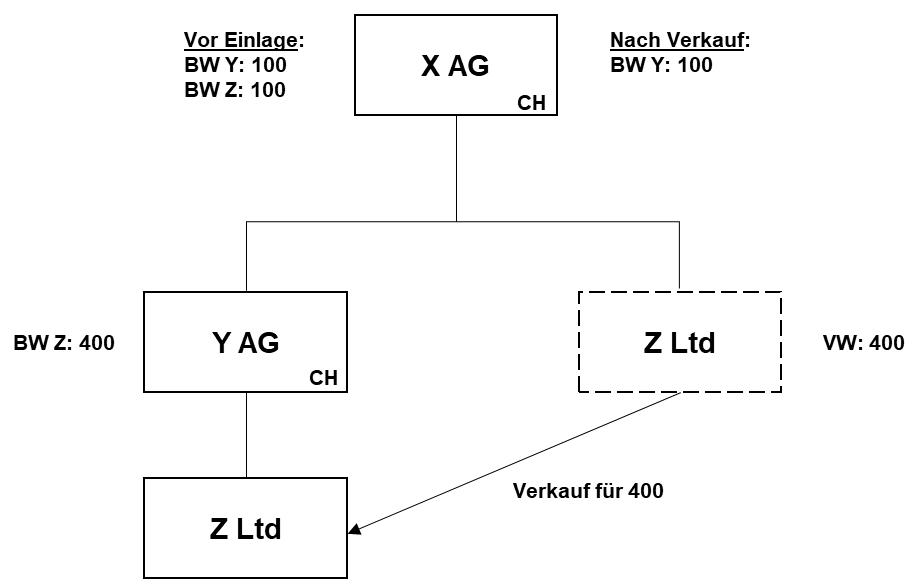

Basel-based X. AG owns two subsidiaries: the domestic Y. AG and the foreign Z. Ltd.

Y. AG has an income tax value (= cost basis) of CHF 100 million and a market value of CHF 150 million.

Z. Ltd. has a tax basis (cost basis) of CHF 100 million and a market value of CHF 400 million.

X. AG contributes Z. Ltd. to Y. AG at market value and records this as follows:

X. AG: Investment in Y 100 / Investment in Z 100

Y. AG: Investment Z 400 / Reserves 400

What are the tax consequences of this transaction?

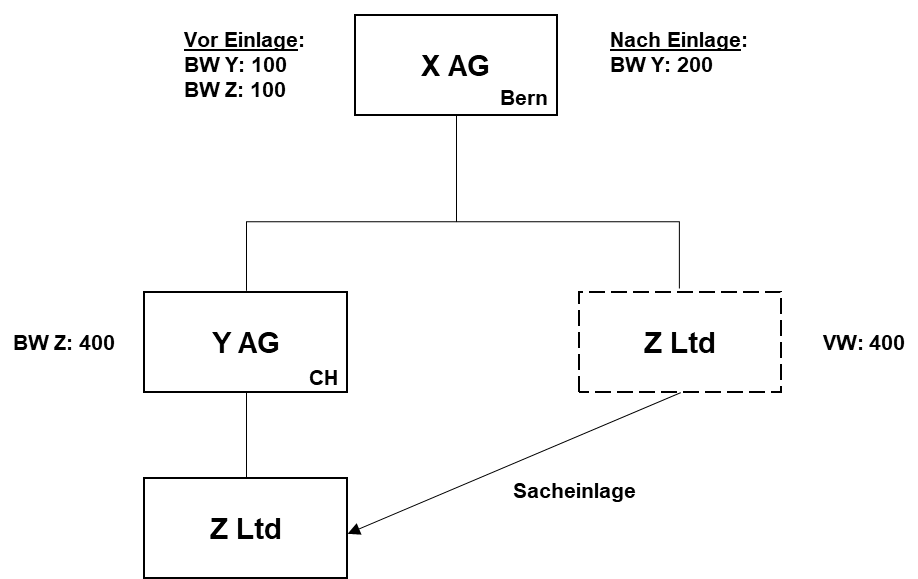

What would change if X. AG were domiciled in the Canton of Bern?

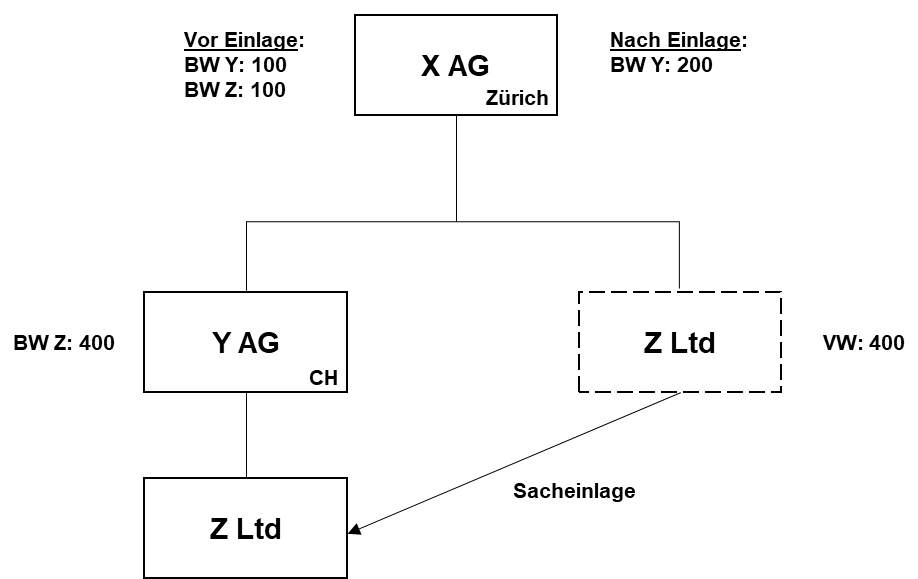

What would change if X. AG were based in the Canton of Zurich?

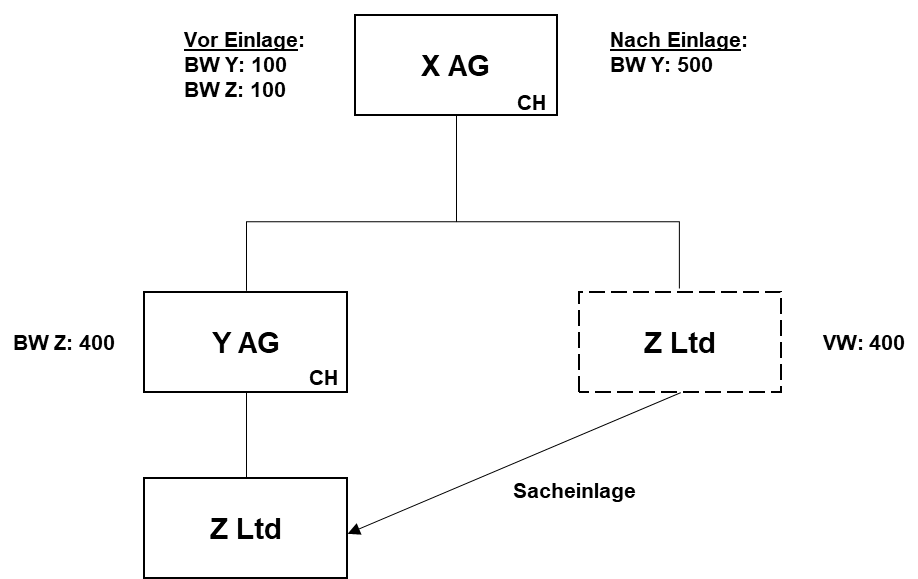

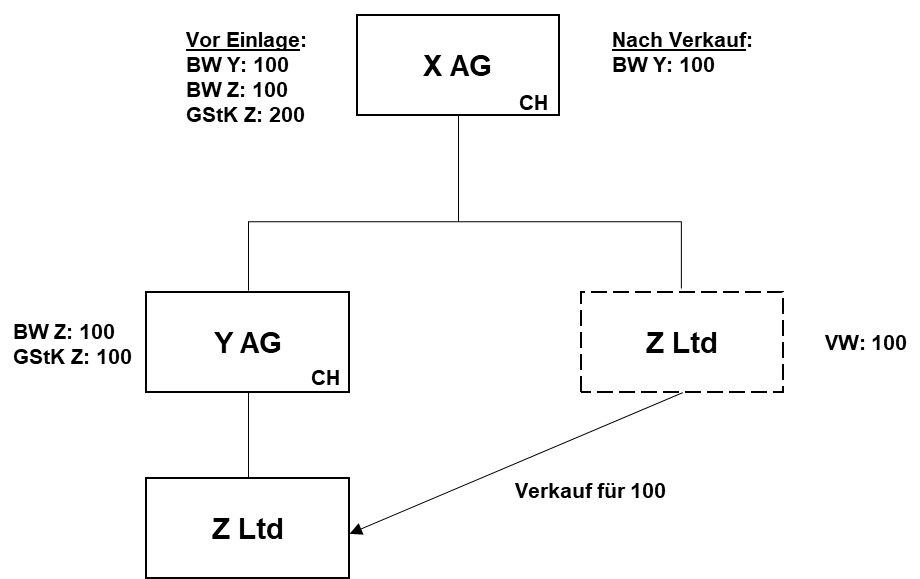

What would change if Z Ltd’s contribution to Y AG were recorded as follows:

X. AG: Investment in Y 400 / Investment in Z 100 / Income 300

Y. AG: Investment in Z 400 / Reserves 400

(Sub-variant

: Y. AG has a profit tax value of CHF 100 million, a cost basis of CHF 200 million, and a market value of CHF 100 million)

What would change if X. AG sold Z. Ltd. to Y. AG for cash at a market value of CHF 400 million?

From an accounting perspective, the sale would have the following effect:

X. AG Cash 400 / Investment in Z. Ltd 100 / Income 300

Y. AG Investment in Z. Ltd 400 / Cash 400

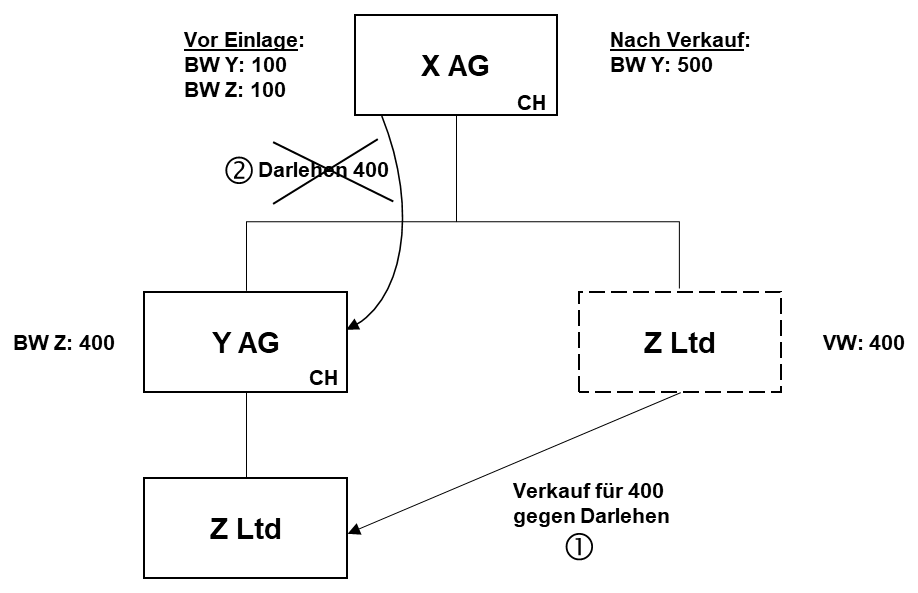

What would change if X. AG were to sell Z. Ltd. to Y. AG at a fair value of CHF 400 million in exchange for a loan (Step 1) and, on the same day, X. AG were to waive its loan receivable from Y. AG (Step 2), with the waiver being recorded by Y. AG as a non-income-affecting item?

Z. Ltd still has a profit tax value of CHF 100 million, but the cost basis is CHF 200 million and the fair market value is CHF 100 million.

X. AG sells Z. Ltd to Y. AG at the fair market value (= income tax value) of CHF 100 million.

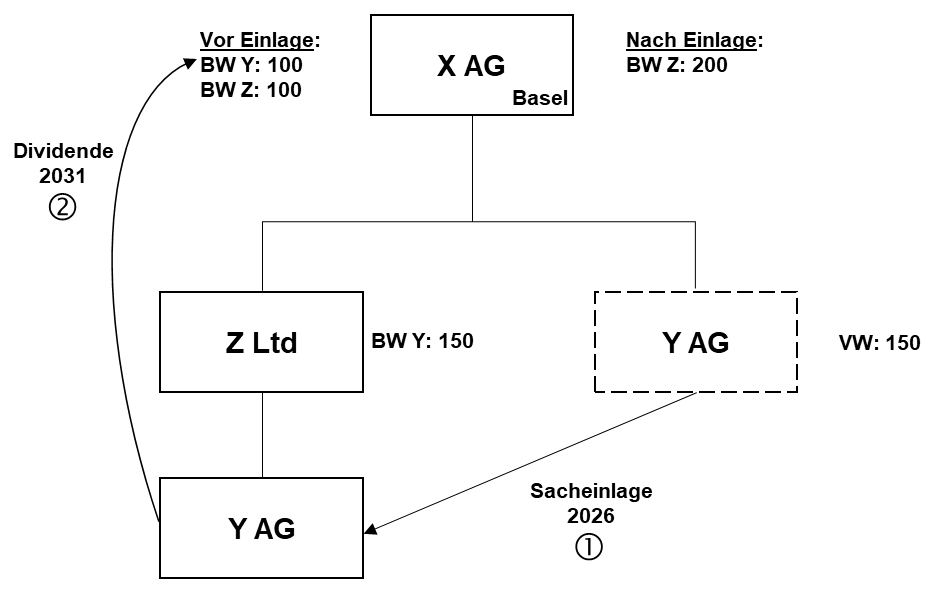

What would change if Y. AG were contributed to Z. Ltd. at fair market value in 2026 and recorded as follows:

X Inc.: Investment in Z 100 / Investment in Y 100

Z. Ltd: Investment in Y 150 / Reserves 150

In 2031, Z. Ltd distributes Y. AG to X. AG. At this point, Z. Ltd has a market value of CHF 300 million, at which it is recorded in X. AG’s books. (Alternative

: Sale for CHF 300 million)

For many years, X. has held several buildings with rental apartments in the Canton of Bern as part of his private assets, from which he generates annual rental income of CHF 2 million and incurs administrative expenses of CHF 80,000 per year. In the 2025 tax period, he declares these as business assets for the first time.

In 2026, he transfers the properties to X. AG.

Can X. invoke Art. 12(4)(a) of the Federal Act on Property Tax (StHG) with regard to real estate gains tax?

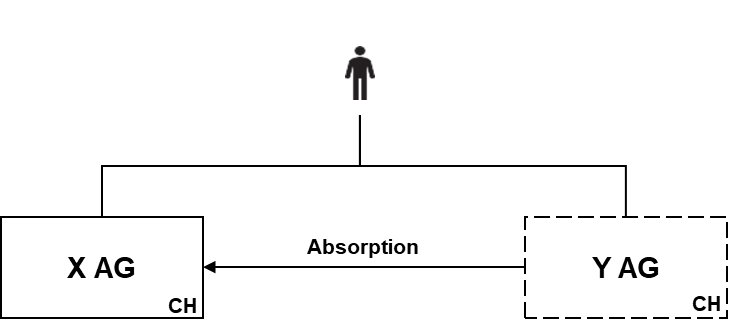

X. AG absorbs Y. AG. Both companies are active and are held by Mr. X.

The balance sheets are as follows (in TCHF, no hidden reserves):

X. AG Y. AG X. AG (after merger)

Share Capital 100 Share Capital 100 Share Capital 200

Ret. 100 Ret. 400 Ret. 300

Retained earnings: -200

What are the tax implications of the merger?

X Inc. absorbs Y Inc. Both companies are active and are held by Mr. X.

The balance sheets now appear as follows (in TCHF, no hidden reserves):

X. AG Y. AG X. AG (after merger)

Share Capital 100 Share Capital 100 Share Capital 200

Retained earnings 400 Retained earnings 400 Retained earnings 400

Retained earnings: -200 Retained earnings 200

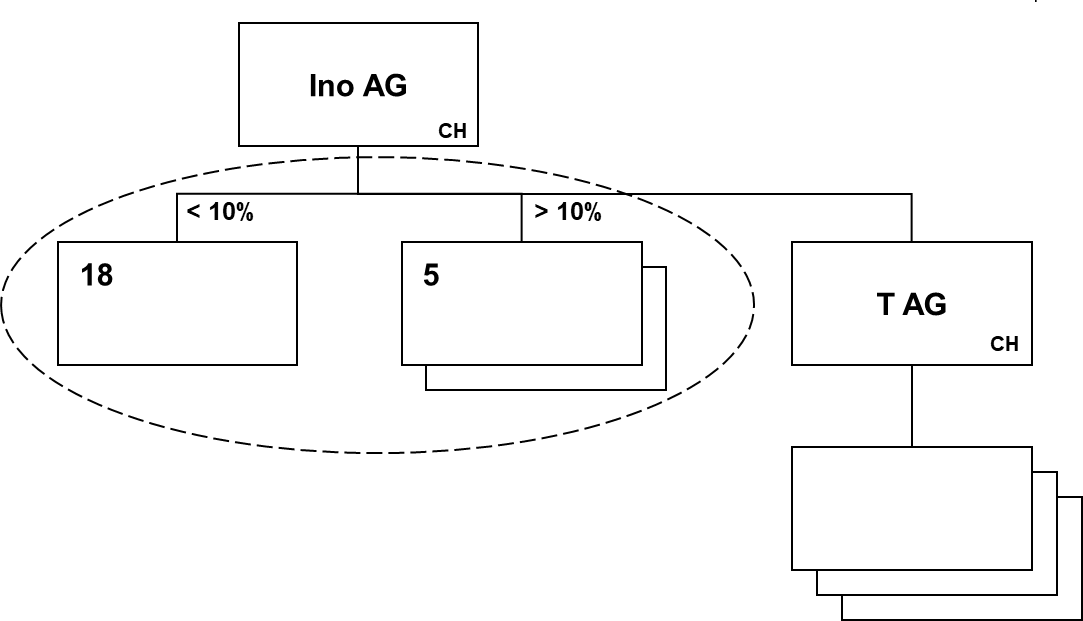

Innovation AG holds stakes in various startups and supports them by providing advice and access to an attractive network. Innovation AG intends to establish a competence center and create the necessary spatial, technical, and operational conditions for a wide range of companies.

Innovation AG can be divided into the areas of (1) support and services, and (2) financial support and equity investments (promotion of entrepreneurship through the provision of equity and/or debt capital). Both areas employ staff and generate revenue from, among others, sponsors who wish to strengthen these innovations.

Innovation AG intends to expand its shareholder base to generate more funds for promoting innovation. In doing so, area (2) of financial support and investments, along with its investment portfolio, is to be spun off into a subsidiary. The 23 investments in fixed assets are to be transferred to the subsidiary at book value.

| Balance Sheet Innovation AG (in TCHF) | | | | | ------------------------------ | ----- | ------------- | ----- | | Current assets | 1,000 | Liabilities | 200 | | 18 investments1 < 10% | 3,500 | Share capital | 3,600 | | 5 investments2 > 10% | 2,000 | Retained earnings | 2,700 | | | | | |

1 Total market value TCHF 4,500

2 Total market value: TCHF 3,000

Can the equity interests be transferred to a subsidiary on a tax-neutral basis?

Three years after the spin-off, the subsidiary sells one of the equity interests < 10% (book value CHF 200,000; fair market value at the time of the spin-off CHF 250,000) for a price of CHF 10 million. What are the tax consequences?

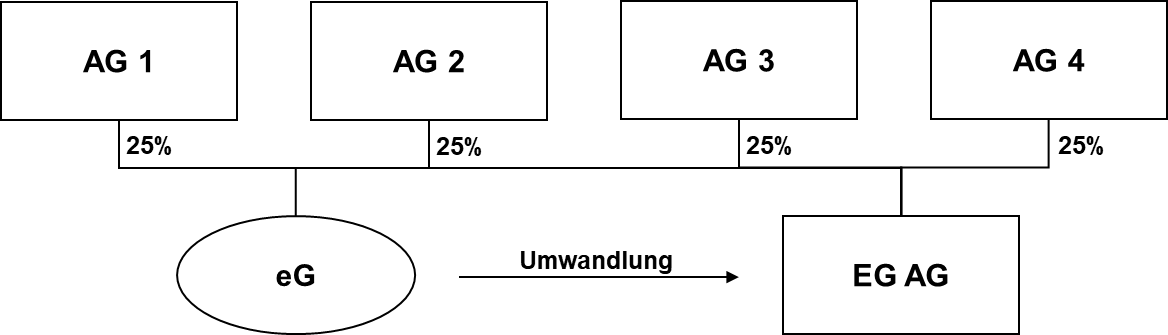

The general partnership eG was established to organize the use of specialized machinery in an economically optimal manner by pooling the costs of several companies. The use of the specialized machinery is now open not only to the partners, but the general partnership also offers its services to all interested parties on the market. The eG employs eight staff members.

Four stock corporations (AG 1 – AG 4) hold interests in the general partnership. Each stock corporation is a partner in eG with a one-quarter share.

There are plans to convert the simple partnership into the stock corporation “EG AG.” This will simplify legal, administrative, and accounting procedures. Following the conversion, the stock corporations AG 1–AG 4 will each hold a 25% stake in EG AG.

| eG Balance Sheet (in TCHF) | | | | | ------------------- | ----- | ---------------------- | ----- | | Current assets | 500 | Liabilities | 1,800 | | Fixed assets1 | 2,500 | Shareholders’ equity | 1,200 |

1 The eG reports hidden reserves of TCHF 2,400

| eG Income Statement (in TCHF) | | | | | ---------------------------- | ----- | -------------- | ----- | | Operating/Personnel Expenses | 1,000 | Operating Income | 1,800 | | Other Expenses | 200 | | | | Profit | 600 | | |

Can the eG’s hidden reserves be transferred on a tax-neutral basis as part of the conversion of the general partnership into a stock corporation?

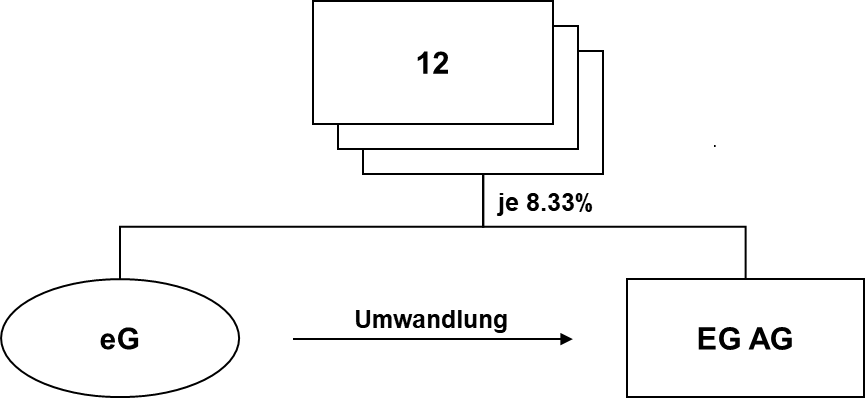

How should the conversion be assessed if twelve stock corporations (SC 1 – SC 12) hold interests in the general partnership? Each stock corporation is a partner in the general partnership with a one-twelfth share. After the conversion, the stock corporations SC 1 – SC 12 each hold an 8.33% interest in the general partnership.

How should the conversion be assessed if eight stock corporations (SC 1 – SC 8) hold interests in the general partnership? Each stock corporation is a partner in the general partnership with an eighth share. After the conversion, the stock corporations SC 1 – SC 8 each hold a 12.5% stake in the general partnership.

Initial situation as in Variant 1: AG 1 – AG 12 are all shareholders of the eG with a one-twelfth share. After the conversion, the stock corporations AG 1 – AG 12 each hold an 8.33% stake in EG AG. Two years after the conversion, AG 1 acquires AG 2’s 8.33% stake in EG AG from AG 2. What are the tax consequences for AG 1 and AG 2?

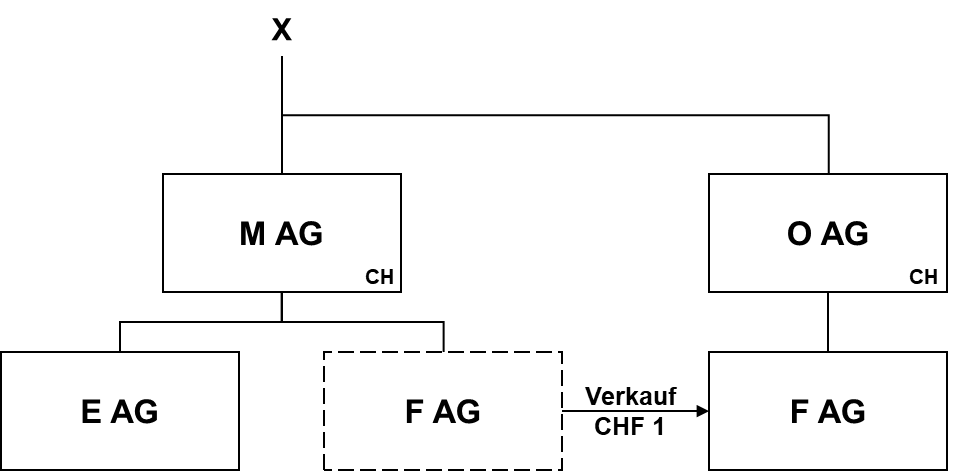

The holding company M. AG owns two subsidiaries, E. AG and F. AG, both of which engage in operational activities. M. AG holds a 100% stake in both companies.

The private owners of M. AG plan to spin off the stake in F. AG. A demerger or a transfer of assets under the Merger Act, as well as a two-stage demerger under the old law, are out of the question due to the cumbersome nature of implementation and the undesirable publicity effect. It is therefore planned to implement the spin-off by selling the stake to the holding company O. AG (incorporated with share capital of CHF 100,000), which was previously established by the private owners. Since a sales contract with a sales price of CHF 0 is not permissible under civil law, the stake in F. AG is to be sold to O. AG for CHF 1. The retained earnings of M. AG will be reduced by the book value of the equity interest, less the sale price of CHF 1. The corresponding amount will be recorded in the retained earnings of O. AG.

| Balance Sheet of M. AG before Demerger (in CHF) | | | | | ---------------------------------- | --------- | ------------- | ---------- | | Investment in E. AG | 9,500,000 | Liabilities | 900,000 | | Investment in F. AG | 7,500,000 | Share capital | 100,000 | | | | Retained earnings | 16,000,000 |

| Balance Sheet of M. AG after Split (in CHF) | | | | | ----------------------------------- | --------- | ------------- | --------- | | Investment in E. AG | 9,500,000 | Liabilities | 900,000 | | Receivable from O. AG | 1 | Share capital | 100,000 | | | | Retained earnings | 8,500,001 |

| Balance Sheet of O. AG after Split (in CHF) | | | | | ----------------------------------- | --------- | ------------------- | --------- | | Cash and cash equivalents | 100,000 | Liability to M. AG | 1 | | Investment in F. AG | 7,500,000 | Share capital | 100,000 | | | | Retained earnings | 7,499,999 |

Question