1. Facts

BergGipfel Asset Management AG (BGAM AG) was founded on March 1, 2007, with the primary purpose of providing consulting and services in the field of asset management, and is headquartered in Horgen. Its share capital, divided into 1,000 shares with a par value of CHF 100 each, is 99% owned by BI (999 shares with a par value of CHF 100 each) and 1% by his wife NI (1 share with a par value of CHF 100). Both reside in Wädenswil and serve on the company’s board of directors. Unlike NI, BI is also actively involved in the company’s operations as the managing director of BGAM AG.

BI wishes to transfer BGAM AG to younger hands as part of a business succession plan. To this end, he wishes to transfer all shares to SU, a long-time employee of BGAM AG with joint signing authority. SU resides in Landquart (Canton of Graubünden).

The plan is for NI to first transfer her 1% stake to BI at a price of CHF 30. Subsequently, BI intends to transfer his 100% stake to SU at the same price, i.e., for a total of CHF 30,000 (CHF 30 per share: total 1,000 shares at CHF 30 each = CHF 30,000). SU is to continue operating BGAM AG in accordance with BI’s intentions and provide asset management services to its long-standing clients in the customary manner.

The parties are aware that the price per share of CHF 30 is not only below par value but also below the formula value (according to the Praktiker Method I pursuant to KS SSK 28 as of December 31, 2023: CHF 280) or a market value.

Question

How should a share acquisition by SU as of July 1, 2024, be classified for tax purposes?

Same facts as in the basic scenario, but BI sells its shares to SU in two tranches: The plan is for BI

- will sell a 40% stake in BGAM AG as of July 1, 2024, at a price of CHF 30 per share, and

- on January 1, 2027, purchase the remaining 60% at the same price of CHF 30 per share.

BI and SU enter into a shareholders’ agreement. This agreement stipulates that, in the event SU unexpectedly leaves the company (for whatever reason), he is obligated to return his shares to BI at the formula value applicable at that time (practical method, Model 1 KS SSK 28).

Question

Does this change the tax treatment of SU’s share purchase?

Same facts as in Variant 1; the shareholder agreement provides for a right of SU to return the shares, but not an obligation to do so.

Question

Does the tax treatment of SU’s share acquisition differ from that in Variant 1?

1. Facts

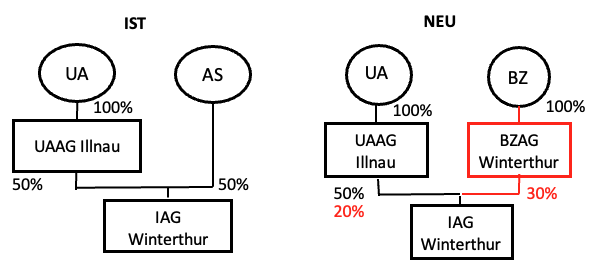

UA, a resident of Illnau-Effretikon, is the managing director and chairman of the board of directors of IAG. BZ, a resident of Kollbrunn, is a long-standing employee and has been a member of the board of directors since 2020. Another member of the board of directors is AS (retired since October 2019), a resident of Bülach.

In 2010, as part of a management buyout, UA and AS acquired IAG from SG through Ing Holding AG (IHAG), a company established for this purpose, in which they each hold a 50% stake. The purchase price for 100% of the shares was CHF 4 million. In a shareholders’ agreement (ABV), UA and AS agreed on a right of first refusal for share capital increases as well as a right of first refusal for share sales in favor of the other shareholder. According to the ABV, the share price is to be agreed upon by the shareholders or determined by the auditors if the shareholders cannot reach an agreement.

Finally, in 2016, UA contributed his 50% stake in IHAG to his personal holding company, UA Holding AG (UAAG), which he owns 100%. In 2018, IHAG merged with IAG (reverse merger) and was subsequently dissolved. Since then, AS and UAAG have each held a 50% stake in IAG. A shareholders’ agreement remains in place between the shareholders, with unchanged provisions regarding preemptive and first-refusal rights as well as the determination of the sale price.

Since the acquisition in 2010, IAG has distributed the majority of its current profits to its shareholders annually as dividends.

Upon retirement, AS wishes to withdraw completely from the company and sell his 50% stake in IAG retroactively as of January 1, 2024, to UA (20%) and BZ (30%), both of whom hold executive positions at IAG. The enterprise value of IAG, determined using the practitioner’s method, amounts to CHF 7 million at this time (→ 50% = CHF 3.5 million).

UA wishes to acquire the 20% stake through UAAG, as he already holds the previously acquired 50% through that entity.

BZ wishes to acquire the 30% stake through his yet-to-be-established personal holding company, BZ Holding AG (BZAG), which he will own 100%. The purchase price for the 30% stake is to be financed partly through a bank loan in favor of BZAG and partly through a loan from BZ to BZAG. BZ refinances the loan through an additional mortgage on his owner-occupied primary residence.

BZ will charge BZAG the same interest rate that he must pay on the additional mortgage.

BZAG and UAAG each acquire their shares at the enterprise value calculated using the practitioner method, i.e., BZAG 30% for CHF 2,100,000, UAAG 20% for CHF 1,400,000. The ABV is maintained.

Questions

How should the share acquisition by UA and BZ via the employee holding companies (UAAG and BZAG) be classified?

-

What are the tax consequences if UAAG or BZAG sells IAG shares three years after acquisition?

-

Three years after acquiring the IAG shares, BZ sells its 100% stake in BZAG- What are the tax consequences for BZ?

- What are the tax consequences for UA?

-

Three years after acquiring the IAG shares, BZ sells a 25% stake in BZAG- What are the tax consequences for BZ?

- What are the tax consequences for UA?

-

Can the acquisition via a personnel holding company be viewed as tax avoidance?

Same facts as in the base scenario, but BZAG and UAAG acquire shares for CHF 1,200,000 (BZAG 30%) and CHF 800,000 (UAAG 20%) respectively, i.e., at the value used in the earlier transaction and thus below the formula value.

Same facts as in Variant 1, but BZ is the son of AS and has been working in a management position at IAG for several years.

Question

- How should BZ’s share acquisition via BZAG be classified?

1. Facts

Gründer-IT AG (GITAG), headquartered in Dietlikon, ZH, was founded on May 20, 2019, by Gründer Holding AG (GHAG), headquartered in Zurich, with a share capital of CHF 200,000 divided into 2,000 registered shares of CHF 100 each. According to the Commercial Register entry, GITAG’s purpose is to provide IT services, trade in IT products, advise natural and legal persons on strategic and operational matters, and provide related services. To this end, GITAG leased office and retail space in Dietlikon in June 2019. GHAG, for its part, was founded by IT specialists and possesses expertise in this industry. It has already applied the following procedure on various occasions for the establishment of IT companies or in connection with company acquisitions.

To finance the interior fit-out, the warehouse, marketing, and other costs during the start-up and development phase, GHAG contributed a capital injection of CHF 600,000 to GITAG’s equity and also granted it a loan of CHF 100,000.

RS is a computer scientist and assumed his position as managing director of GITAG on June 1, 2019.

Immediately after GITAG was founded (on the same day), RS acquired a 10% stake in GITAG pursuant to a purchase agreement dated May 20, 2019. The purchase price for the 10% stake was CHF 80,000 (share capital of CHF 200,000 and contribution to equity of CHF 600,000 = CHF 800,000 → 10% thereof).

In the purchase agreement dated May 20, 2019, GHAG granted RS a two-part purchase right, namely that RS

- may acquire an additional 80% of GITAG’s shares at any time over the following ten years (from January 1, 2020, to December 31, 2029), in one or more tranches at RS’s discretion. The purchase price per share was fixed at CHF 400, subject to capital increases or repayments, which would be taken into account as price adjustments;

- as of January 1, 2030, RS may also acquire the remaining 10% at the then-current market value, but at a minimum of CHF 400 per share. In the event of a disagreement, the market value shall be determined by the opinions of two experts; the purchase price would be the arithmetic mean of the values in both expert opinions.

As of March 1, 2023, RS and GHAG agreed in an addendum to the original purchase agreement to acquire an additional 10% stake in GITAG. The purchase price was CHF 80,000 (CHF 400 x 200). According to the Practitioner Method Model 2, GITAG’s enterprise value as of December 31, 2022, was CHF 380,000. The formula value for the 10% stake calculated in this manner amounted to CHF 38,000 at that time.

RS plans to acquire an additional 70% stake in GITAG as of June 1, 2024. The purchase price is CHF 560,000 (CHF 400 per share x 1,400 shares).

According to the Practitioner Method Model 2, the enterprise value of GITAG as of December 31, 2023, is CHF 1,560,000. The formula value thus determined for the 70% stake is CHF 1,092,000 (CHF 780 per share). The 70% stake is subject to a 8-year lock-up period, corresponding to a discount of 37.259%. The resulting reduced formula value for the 70% stake is, rounded, CHF 685,132 (= CHF 1,092,000 x 62.741%).

There is a shareholders’ agreement in place stipulating that the enterprise value must continue to be determined in the future using the Practitioner Method Model 2. Pursuant to the shareholders’ agreement, GHAG has a right of first refusal on RS’s shares until December 31, 2029

- if RS dies or becomes permanently incapacitated,

- if RS ceases active service as a board member or IT specialist due to resignation by RS or termination by GITAG for good cause. Good cause includes a decline in revenue under RS’s management for five consecutive years or a permanent reduction in his working hours exceeding 50% of his normal working hours.

RS (or his legal successor) has a right of sale to GHAG until December 31, 2029

-

if RS dies or becomes permanently incapacitated;

-

if RS ceases active employment as a board member or IT specialist.

RS will finance the planned purchase of the 70% stake with private funds. He will also acquire and hold the 70% stake directly.

Questions

- How should the first share purchase of 10% on the date of incorporation (immediately after incorporation) be classified?

- How should the second share purchase of a 10% stake on March 1, 2023, be classified?

- How should RS’s third share purchase of a 70% stake as of June 1, 2024, be classified?

- Does RS have to take into account any restrictions from the initial share purchases regarding the acquisition of the final 10% after January 1, 2030?

The first and second share purchases are the same as in the basic scenario. However, RS’s third share purchase of 70% takes place on June 1, 2026.

According to the Practitioner Method Model 2, the enterprise value of GITAG as of December 31, 2025, is CHF 1,560,000. The formula value thus determined for the 70% stake is CHF 1,092,000 (CHF 780 per share). The 70% stake is subject to a lock-up period of 8 years (through May 31, 2034), which corresponds to a discount of 37.259%. The resulting reduced formula value for the 70% stake remains unchanged at approximately CHF 685,132 (= CHF 1,092,000 x 62.741%).

Questions

1. Alternative:

On June 2, 2031, an independent third party, RS (90% shareholder) and GHAG (10% shareholder), makes a takeover offer to acquire 100% of GITAG and offers CHF 1,200 per share.

- What are the tax consequences for RS?

2. Alternative:

On June 2, 2031, GHAG acquires 90% of RS based on a third-party appraisal at a price of CHF 1,200 per share.

- What are the tax consequences for RS?

1. Facts

In 1998, AN and BS founded ABS GmbH, headquartered in Aarau, with a capital contribution of CHF 10,000 each. The purpose of ABS GmbH is the planning, installation, and commissioning of solar power systems. BS serves as managing director with sole signing authority. Internally, the business partners managed ABS GmbH on an equal footing from the outset. BS contributed his expertise in the installation and commissioning of the systems, and AN, as an engineer, was responsible for the planning of the systems.

In 2000, BS founded another company with other business partners, and BS’s activities subsequently shifted increasingly to that company. In 2010, BS retired. At that time, AN was the sole employee and wage earner (at market-rate wages) of ABS GmbH. He continued to expand the planning division. ABS GmbH now employs 8 people in the planning department.

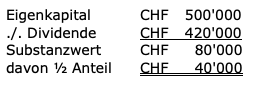

In 2021, BS passed away. AN acquired the share from BS’s estate for a price of CHF 60,000. Prior to the purchase of the share, the non-operating reserves of CHF 420,000 were distributed in full to the shareholders. The company’s enterprise value at that time, calculated using the so-called practitioner method, was CHF 800,000. The purchase price was calculated based on the net asset value according to the interim financial statements as of June 30, 2021 (rounded figures):

Purchase price: The net asset value was rounded up to CHF 60,000.

The competent tax office classified the purchase of the additional ordinary share as a genuine employee shareholding and assessed the difference between the purchase price and the formula value as income from employment.

Following an appeal, the tax office waived taxation for the 2021 tax year on the condition that the employee agreed to the following reverse arrangement (referred to as a “perpetual formula commitment”):

- In the event of a future sale of the equity interest in ABS GmbH acquired in the 2021 tax year, the difference between the equity then available plus CHF 20,000 and the actual proceeds from the sale shall be classified as income from employment for AN.

- The Employee waives the right to claim, in the event of a sale of the ABS GmbH share acquired in 2021, that the tax realization date is attributable to the 2021 tax period.

- The “first in, first out” principle applies. Accordingly, upon the sale of a share, the share acquired in 2021 is considered sold only if the second share is no longer owned by AN or is sold at the same time. Should the number of shares and their par value change due to an amendment to the articles of association, the foregoing applies mutatis mutandis. If the share acquired in 2021 is transferred by gift, mixed gift, or inheritance, the “perpetual formula commitment” also applies to the new owners. The ordinary share acquired in 2021 shall be deemed to have been transferred by gift, mixed gift, or inheritance, provided that the second ordinary share is no longer owned by AN or is transferred at the same time. Should the number of ordinary shares and their par value change due to an amendment to the Articles of Association, the foregoing shall apply mutatis mutandis.

- AN expressly declares that this agreement remains in full force and effect even if tax jurisdiction changes due to a change of residence (whether intermunicipal or intercantonal).

Question

How should AN’s acquisition of shares in 2021 be classified under Zurich tax practice?