1. Background

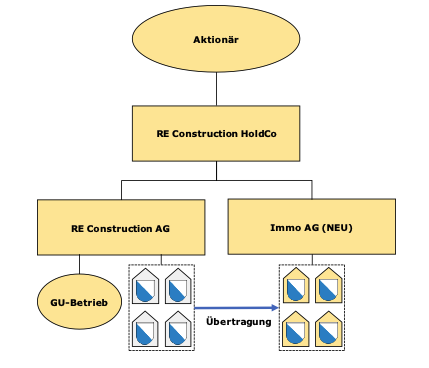

The RE Construction Group is engaged in the development of construction projects. Some of the completed buildings are not sold after construction (though this applies to only a minority of the developed properties), but are retained by the company as part of its investment strategy. The properties are managed by a third-party provider. Mr. B is the owner of the RE Construction Group. For strategic reasons, it is planned to separate the four investment properties in the Canton of Zurich from the general contractor and transfer them to Immo AG. The structure is as follows:

The investment properties consist of developed plots with 80 apartments. The annual rental income amounts to CHF 2.2 million (net), and the annual administrative expenses amount to CHF 80,000.

Questions

- Can the developed properties be transferred to Immo AG in a tax-neutral manner?

- Does your assessment change if two of the four buildings are not yet completed or do not yet have tenants at the time of the transfer? Assume that the other two properties are also only partially leased, meaning the figures in the facts section are merely estimates. In reality, only CHF 0.3 million in annual rental income is generated. Management has so far been handled on an interim basis by RE Construction AG itself and remains within manageable limits.

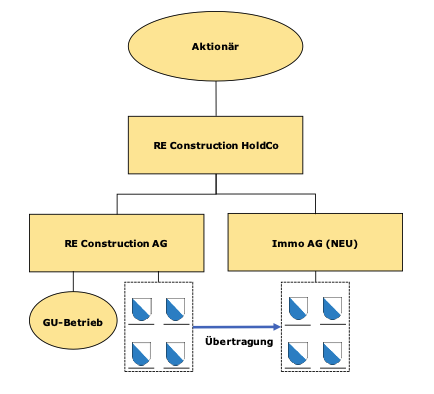

The RE Construction Group is dedicated to the development of construction projects. Due to favorable market conditions, RE Construction AG was recently able to acquire four building plots in the canton of Zurich. It has been decided not to develop the properties and to hold them as an investment. For estate planning purposes, the properties are not to remain within RE Construction AG but are to be transferred to a new real estate company (Immo AG).

The properties generate annual rental income of CHF 200,000 through partial use as parking spaces. Annual administrative expenses amount to CHF 20,000.

Questions

- Can the building plots be transferred to Immo AG in a tax-neutral manner?

- Does your assessment change if there is already an approved construction project for the development of the properties, which assumes rental income of CHF 18 million upon completion?

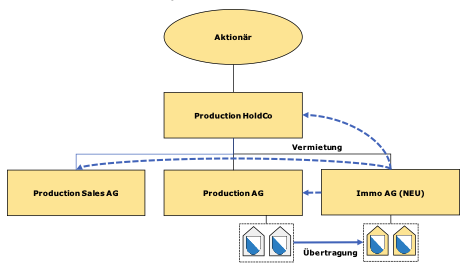

The Production Group is an operating group active in the development and marketing of medical technology. The Production Group’s headquarters are located in Wädenswil (headquarters of Production HoldCo and Production Sales AG). The office building is owned by Production AG. Production takes place in Dübendorf in Production AG’s own manufacturing facility. The shareholder of the Production Group is Mr. P, the father of a daughter and a son. The daughter is already heavily involved in the operational management of the Production Group. The son is a winemaker and does not wish to be involved in the Production Group in the future. As part of estate planning, the buildings owned by the Production Group are to be transferred to Immo AG. The structure is as follows.

Following the transfer, the commercial buildings will be leased by Immo AG to Production HoldCo, Production Sales, and Production AG (not a classic sale-and-lease-back arrangement). Long-term lease agreements will be entered into. Rent is payable on June 30 of each year. Immo AG’s expenses remain within a very manageable range.

There are two lease agreements. The annual rental income amounts to CHF 2.1 million (net), and the annual administrative expenses amount to CHF 20,000.

Questions

- Can the Production Group’s buildings be transferred to Immo AG in a tax-neutral manner?

- Are there any restrictions on a tax-neutral holding split (assuming the operational requirement is also met upon transfer to Immo AG)? What must be considered regarding real estate gains tax, and what should be included in the share purchase agreement in the event of a sale of Immo HoldCo?

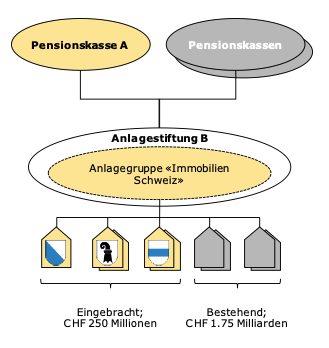

1. Background

Pension Fund A owns five properties (all residential properties in Switzerland).

Pension Fund A wishes to transfer all properties to Investment Foundation B. This is driven by economic considerations such as diversification, deeper knowledge of regional markets, more professional real estate management, cost reduction through exploitable synergies, and improved performance.

The consideration owed for the transfer is settled by the acquiring Investment Foundation B through the issuance of no-par-value, irrevocable claims (book claims) in the “Swiss Real Estate” investment group.

Investment Foundation B already holds properties with a market value of CHF 1.75 billion. All are located in the “Swiss Real Estate” investment group.

Investment Foundation B is not leveraged.

Following the transfer of the properties to Investment Foundation B, the structure is as follows:

Question

What are the tax consequences of Pension Fund A’s transfer of the properties to Investment Foundation B?

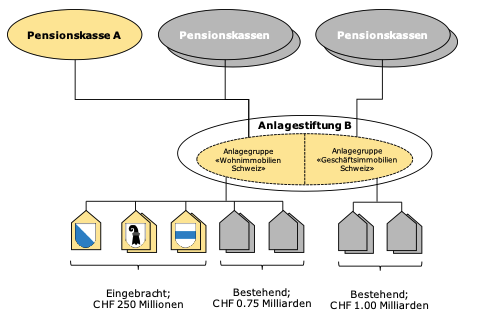

Compared to the basic scenario, Investment Foundation B maintains two different investment groups. The “Residential Real Estate Switzerland” investment group currently comprises properties with a market value of CHF 0.75 billion. The “Commercial Real Estate Switzerland” investment group currently comprises properties with a market value of CHF 1.00 billion. Pension Fund A’s properties are settled in exchange for the issuance of no-par, irrevocable claims (book claims) in the “Residential Real Estate Switzerland” investment group.

Question

What are the tax consequences of Pension Fund A’s contribution of the properties to the “Residential Real Estate Switzerland” investment group of Investment Foundation B?

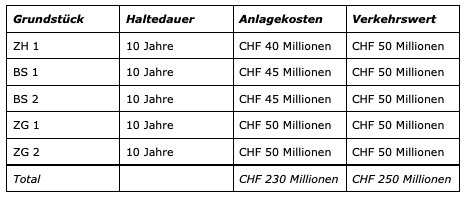

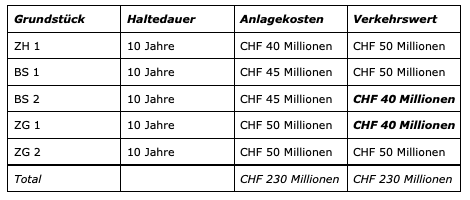

Facts as per Alternative 1. However, the market values of properties BS 2 and ZG 1 have decreased.

Question

Is there potential for optimization compared to Alternative 1?

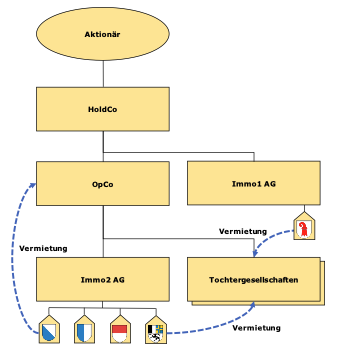

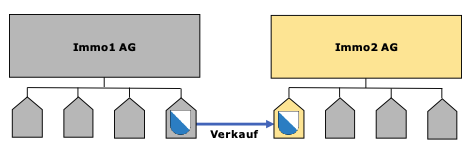

1. Facts

Group A is an operating group. The real estate necessary for operations (in the cantons of ZH, LU, SO, GR, and BL) is owned by group real estate companies (Immo1 AG and Immo2 AG). All companies are headquartered in the canton of Solothurn. The structure is as follows:

Questions

- To raise liquidity, HoldCo sells all shares in Immo1 AG and OpCo sells all shares in Immo2 AG. The lease agreements remain in effect. What are the tax consequences (real estate gains tax, transfer tax, and income tax) regarding the properties?

- The shares in Immo1 AG and Immo2 AG are not sold. Instead, the shareholder sells all shares in HoldCo and thereby indirectly also Immo1 AG and Immo2 AG, respectively the properties. Are there different tax consequences regarding the properties compared to the direct sale of the shares in Immo1 AG or Immo2 AG?

1. Background

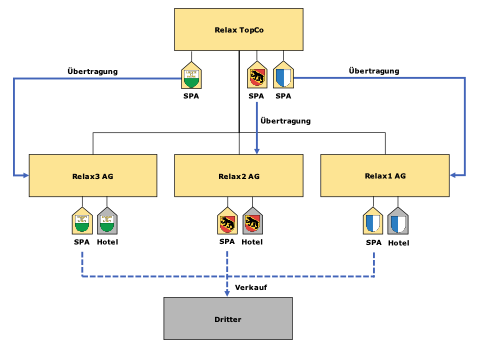

The Relax Group is currently active in the wellness and hospitality sectors. Originally, the Relax Group intended to invest in hotels located as close as possible to thermal baths and other wellness facilities (hereinafter “SPAs”). When the SPAs were put up for sale, the Relax Group decided to acquire them. The acquiring company was Relax TopCo. Due to increased demand, the Relax Group decided to expand hotel capacity and close the SPAs to the public, making them accessible only to hotel guests. To this end, the SPAs (buildings and operations) were transferred to the respective hotel companies (Relax1 AG, Relax2 AG, and Relax3 AG). The transfer was tax-neutral. Three years later, the spa buildings were sold to an investor (a third party) to raise liquidity (no replacement purchase was made). This can be illustrated graphically as follows:

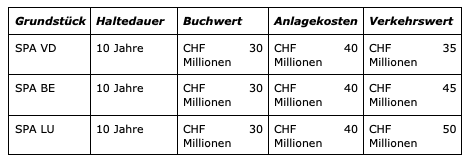

The property values of the SPA plots at the time of the transfer to the hotel companies are as follows:

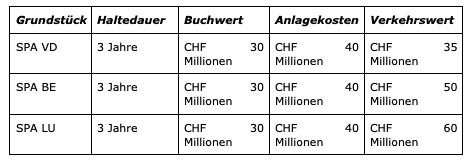

The property values of the SPA plots at the time of sale to the third party are as follows (taking into account the tax-neutral transfer to the hotel companies):

Questions

- What are the tax consequences for Relax TopCo?

- What are the real estate transfer tax consequences for Relax1 AG in the Canton of Lucerne?

- What are the property gains tax and transfer tax implications for Relax2 AG in the Canton of Bern?

- What are the transfer tax implications for Relax3 AG in the Canton of Vaud?

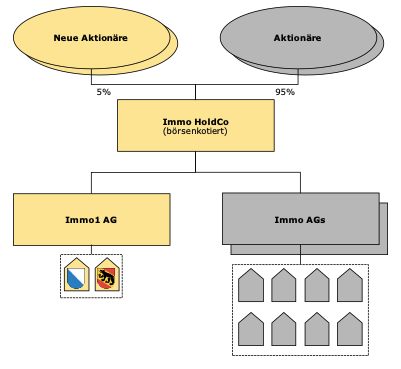

Immo1 AG owns two large parcels of land, each developed with several apartment buildings. Their returns are no longer sufficient, and property and administrative expenses have risen significantly in recent years. The shareholders decide to sell their equity interests in Immo1 AG from their private assets.

Immo HoldCo, listed on the over-the-counter market, expresses interest and proposes a quasi-merger. The sale price is set at CHF 100 million, with CHF 50 million paid in cash to the shareholders and CHF 50 million paid in newly issued shares. The newly created share capital amounts to approximately 5% of Immo HoldCo’s total share capital. The requirements for the quasi-merger (KS ESTV 5a, Section 4.1.7.1) are met. The structure is as follows:

Shortly after the quasi-merger, 80% of the new shareholders sell their shares in Immo HoldCo on the stock exchange.

Questions

- Is this also a tax-neutral quasi-merger for property tax purposes?

- Do the transactions described have any property tax implications?

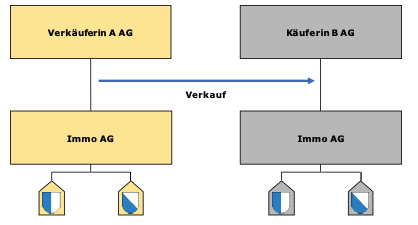

1. Facts

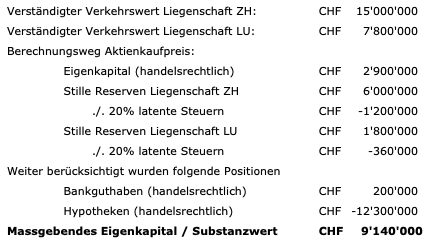

Seller A AG, based in Zurich, holds 100% of the shares in Immo AG (also based in Zurich). Immo AG owns one property in the canton of Lucerne and one property in the canton of Zurich. All shares of Immo AG are sold to buyer B AG. This can be illustrated as follows:

The purchase price of the shares in Immo AG is CHF 9,140,000. The following values were taken into account when determining the purchase price.

Questions

- How is the transfer value of the Zurich property, which is decisive for Zurich property gains tax, determined?

- How is the transfer value of the Lucerne property, which is relevant for Lucerne transfer tax, determined?

1. Facts

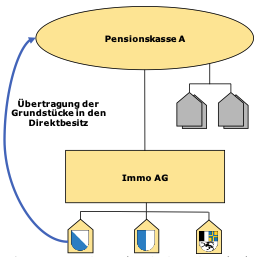

Pension Fund A, organized as a foundation, has acquired 100% of the shares in Immo AG (both headquartered in Zurich). At the time of the acquisition of the shares by Pension Fund A, Immo AG’s financial statements show real estate with a book value of CHF 400 million (market value CHF 700 million; no other hidden reserves). Equity consists of share capital and capital contribution reserves, each amounting to CHF 100 million. Immo AG is affected by the cash trap issue, which is why there are no retained earnings but cash and cash equivalents of CHF 100 million. Unlike Immo AG, Pension Fund A, as an occupational pension institution, is exempt from income tax. To avoid unnecessary tax expenses, the real estate is now to be transferred from the taxable portion of Immo AG to the tax-exempt portion of Pension Fund A.

The potential tax savings were already known at the time of acquisition. Therefore, it was already intended at that time to transfer the properties from Immo AG to Pension Fund A as soon as possible.

Questions

- What tax consequences will result from the transfer if the shares in Immo AG were acquired at that time by a legal entity domiciled in the Canton of Zurich?

- What tax consequences will result from the transfer if the shares in Immo AG were acquired at that time by a natural person residing in Copenhagen (Denmark)?

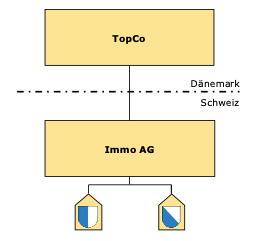

1. Facts

TopCo, based in Denmark, holds all shares in Immo AG, Zurich. Immo AG owns a property located in the city of Zurich. The property was acquired by Immo AG in a taxable transaction in 2010. The acquisition cost is CHF 50 million, and the current market value of the property is CHF 100 million. The shares in Immo AG are now being sold to a third party.

TopCo is an operating company with sufficient substance in Denmark for the purposes of Swiss real estate gains tax.

Question

Is real estate gains tax levied in the Canton of Zurich, and on what capital gain?

1. Facts

Immo1 AG owns a property (multi-family house) in the Canton of Zurich. Immo2 AG intends to acquire the property.

Questions

- What must the acquiring Immo AG secure based on the statutory lien, and how should this be done? How does the lien procedure work?

- What special considerations must be taken into account if Immo1 AG wishes to make use of § 224a StG-ZH (offset of business losses against property gains tax) due to an operating loss?

- How should the situation be assessed in comparison to the initial scenario if the property is located in the Canton of Lucerne rather than in the Canton of Zurich?